PLEASE NOTE: Changes to the registration threshold and rate of payroll tax occurred from 1 January 2019.

From 1 January 2019, businesses with annual Australian wide wages:

- $1.5 million or less are no longer liable for payroll tax.

- between $1.5 million and $1.7 million benefit from a reduced payroll tax rate.

For businesses grouped for payroll tax the $1.5 million threshold relates to the total taxable wages of all group members.

There are no changes for business with wages above $1.7 million.

Please note, business with wages below $1.5 million are still required to lodge a 2018-19 Annual Reconciliation.

From 1 January 2019, the threshold increased from $600,000 to $1.5 million.

This means if your Australia wide annual wages are $1.5 million or less, you are no longer liable for payroll tax, from 1 January 2019.

However, you may still be liable for payroll tax up to 31 December 2018.

Employers with Australia wide annual wages of $1.5 million or less will pay different rates of payroll tax during 2018-19.

1 July 2018 to 31 December 2018 | Variable from 2.5% to 4.95%* |

1 January 2019 to 30 June 2019 | 0% |

* Reduced rate provided by ex gratia.

Your rate is calculated on your Australia wide annual wages (or group wages), this means, your wages before the deduction entitlement is subtracted.

RevenueSA Online will calculate the correct rate and payroll tax payable for each period for each period.

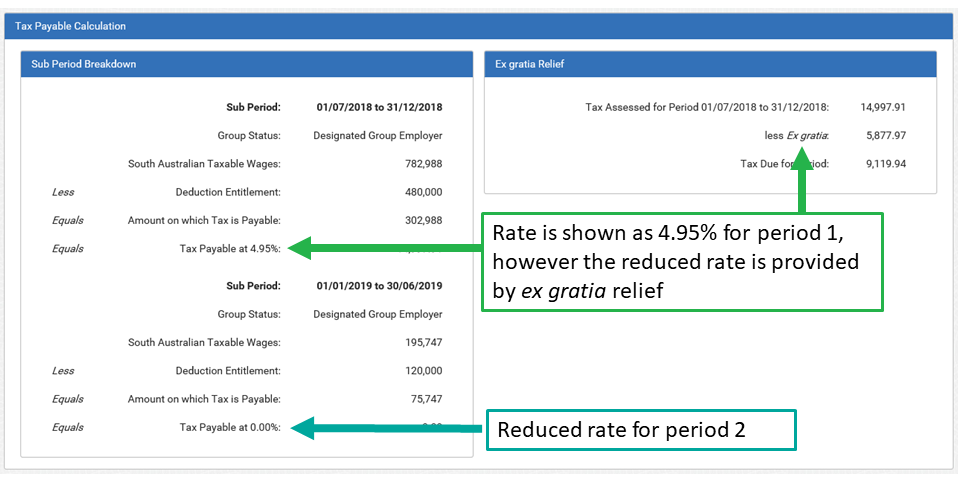

The Tax Payable Calculation screen of your Annual Reconciliation will reflect 4.95% as your payroll tax rate for period 1, however the reduced rate is reflected by the ex gratia relief (see image below). The ex gratia amount is deducted from your payroll tax liability.

Yes, you will still need to lodge your 2018-19 Annual Reconciliation, and provide your wages for the full financial year.

RevenueSA Online will calculate your payroll tax liability for 1 July 2018 to 31 December 2018. (see below).

For the 2018-19 Annual Reconciliation, after entering your South Australian wage components, you will need to provide your total South Australian wages split into 2 periods:

- 1 July 2018 to 31 December 2018 (period 1)

- 1 January 2019 to 30 June 2019 (period 2)

RevenueSA Online will calculate the payroll tax payable for period 1. If your Australia wide annual wages are $1.5 million or less in 2018-19 there will be no payroll tax payable for period 2.

See the SA Wage Details help (PDF 166KB) help for assistance.

If you estimate that your Australia wide wages for 2019-20 will be $1.5 million or less you will be prompted towards the end of your Annual Reconciliation (at the wage estimates screen) to cancel your registration. You have the option to cancel your registration or remain registered:

- To cancel select cancel registration.

- To remain registered select continue with registration.

It’s your choice if you remain registered or cancel. If your wages are close to the threshold (currently $1.5 million), or they fluctuate year to year, you may prefer to retain your registration in case you exceed the threshold in 2019-20.

If you remain registered and would like to change your return cycle to annual or monthly please email your request to payrolltax@sa.gov.au.

If you cancel your registration, and your relevant wages remain below the registration threshold, you will no longer be required to lodge monthly returns or an annual reconciliation in future years.

If you retain your registration you will need to lodge returns, either monthly or annually depending on your return cycle.

You must lodge your Annual Reconciliation online at www.revenuesaonline.sa.gov.au between Monday, 1 July 2019 and Monday, 22 July 2019.

RevenueSA Online has replaced RevNet, but uses the same username and password credentials.

See the RevenueSA Online page for more details on this online portal.

You can also use our AR checklist to prepare the information you need for your annual reconciliation.

You can reset your password in RevenueSA Online.

See the Reset Password help (PDF 130KB) help for assistance.

Help guides are available to assist you in using RevenueSA Online to complete your 2018-19 Annual Reconciliation.

Start (PDF 132KB)

Status (PDF 187KB)

SA Wages (PDF 165KB)

SA Wage Details (PDF 144KB) (2018-19 financial year only)

Interstate Wages (PDF 92KB)

Group Wages (PDF 254KB)

Reconciliation Calculation (PDF 131KB)

Tax Payable Calculation (PDF 176KB) (2018-19 financial year only)

Deduction Allocation (PDF 122KB)

Estimates (PDF 188KB)

Declaration (PDF 857KB)

Modify an Annual Reconciliation (PDF 119KB)

Pay by Electronic Payment Authority (EPA) (PDF 164KB)

Generate a Payment Advice to pay by EFT, BPAY or Cheque (PDF 115KB)

View/Download Annual Reconciliation Report (PDF 116KB)

Void Payment – Electronic Payment Authority (EPA) (PDF 108KB)

You can also access these from within RevenueSA Online. The help icon on each screen will take you directly to the relevant Help.

For the 2018-19 year, the maximum payroll tax deduction entitlement is $600,000. However this may vary based on group status and Australia wide wages.

You may have heard that the threshold increased to $1.5 million from 1 January 2019, however there was no change to the deduction entitlement. The threshold relates only to when an employer must register for payroll tax. That is, if an employer’s Australia wide wages exceed $1.5 million they must register.

For 2018-19, the deduction will be split over the 2 periods:

- 1 July 2018 to 31 December 2018 (period 1)

- 1 January 2019 to 30 June 2019 (period 2)

The amount of deduction for each period will be determined based on the wages paid in each period.

RevenueSA Online will calculate the applicable payroll tax deduction for each period.

| Example |

|---|

An employer pays 75% of their wages during period 1 (1 July 2018 to 31 December 2018) and 25% of their wages during period 2 (1 January 2019 to 30 June 2019). Assuming the employers receives the maximum deduction entitlement of $600,000, their deduction for 2018-19 would be split as follows: Period 1 $450,000 Period 2 $150,000 Total $600,000 |

Employers sometimes make lump sum payments. This can include superannuation top ups, fringe benefits and bonuses.

If these payments relate to the full financial year you can split them across the 2 periods.

For example, an employer pays an employee a $5,000 bonus in recognition of their work through the financial year. The payment is made in June.

As the payment relates to the whole financial year, they can declare $2,500 in period 1 (1 July 2018 to 31 December 2018) and $2,500 in period 2 (1 January 2019 to 30 June 2019).

While completing your Annual Reconciliation, it’s a good time to check that the contact details and organisation name on RevenueSA Online are correct.

If they are not, please update the information to ensure any correspondence is sent to the correct address.

See the Update Details help (PDF 108KB) help for assistance.

If your organisation is part of a group the Designated Group Employer (DGE) is required to lodge first before other group members. This allows the DGE to distribute any unused deduction entitlement to group member/s. When the group member subsequently lodges, the remaining deduction will be allocated resulting in the correct tax being calculated.

Each employer is allocated a status which indicates if they are part of a group or a single employer. Statuses are:

| Non Group Employer (NGE) | An organisation that is not grouped with any other organisation. |

| Designated Group Employer (DGE) | The nominated member of a payroll tax group entitled to claim the group’s payroll tax deduction entitlement. |

| Grouped Employer (GE) | Member of a payroll tax group. Not entitled to claim a payroll tax deduction. |

As part of your Annual Reconciliation, you will be asked to confirm if your status code is correct. Please select:

- YES if your status code is correct.

- NO if your status code is not correct.

If it is not correct you will be able to amend your status code.

See the Status help (PDF 187KB) help for assistance.

If you are a Nominated Single Lodger (NSL) you cannot change your status as part of the Annual Reconciliation lodgement. Please contact RevenueSA before you commence your Annual Reconciliation to change your status.

If your organisation ceased employing in South Australia during 2018-19, you will submit your final return in the Annual Reconciliation. When prompted select YES to the question ‘Did you cease paying wages in South Australia during 2018-19?’.

You will be asked if you want to cancel your registration and you will be required to enter a date of cancellation (the date you ceased paying wages in South Australia) and a reason for the cancellation (from a drop down list).

If you have overpaid your 2018-19 payroll tax, you will be prompted to enter your bank account details during the Annual Reconciliation. A refund will be paid to you via Direct Credit.

If you cannot finalise your Annual Reconciliation by 22 July 2019 please contact RevenueSA at payrolltax@sa.gov.au or on (08) 8226 3750 (select option 5) for advice.

Late lodgement of the Annual Reconciliation may result in interest and/or penalty tax being applied.

Details of any outstanding tax from previous year(s) and/or interest and penalty tax applied from monthly default assessments issued during 2018-19 will be summarised in the Annual Reconciliation.

All requests for remissions of default interest and penalty tax must be emailed to payrolltax@sa.gov.au.

Remission can only be considered after your Annual Reconciliation has been submitted on RevenueSA Online.

You can modify your 2018-19 Annual Reconciliation after it has been submitted by logging into RevenueSA Online and selecting the modify button in the ‘action’ section against the Annual Reconciliation. This will allow you to modify the required data and resubmit.

See the Modify an Annual Reconciliation (PDF 119KB) help for assistance.

Changes to the registration threshold and rate of payroll tax occurred from 1 January 2019.

For the 2018-19 Annual Reconciliation, after entering your South Australian wage components, you will need to provide your total South Australian wages split into 2 periods:

- 1 July 2018 to 31 December 2018 (period 1)

- 1 January 2019 to 30 June 2019 (period 2)

RevenueSA Online will calculate your payroll tax payable for each period.

See the SA Wage Details (PDF 144KB) help for assistance.

In your 2017-18 Annual Reconciliation, and for your monthly returns, you were only required to provide an estimate of your wages.

As there has been a change in the payroll tax during the financial year, you need to declare the wages paid in each period so that payroll tax can be calculated at the correct rate for the period the wages were paid.

The July 2019 monthly return will be open on RevenueSA Online from 23 July 2019 and must be lodged by 7 August 2019.

[Music]

Welcome to RevenueSA’s educational video series. This video is designed for employers with Australia wide wages of $1.5 million or less and will provide you with information to assist you in completing your 2018-19 annual reconciliation.

Payroll tax changes were introduced from 1 January 2019. which will have an impact on your 2018-19 annual reconciliation.

Some things you should take note of for your 2018-19 annual reconciliation include:

- your annual reconciliation is completed in RevenueSA Online

- the registration threshold has increased

- there has been no change to the maximum deduction entitlement

- you will need to provide your total South Australian wages for two periods; and

- a different rate of payroll tax may apply in each period.

Your annual reconciliation is completed in RevenueSA Online. If you are an annual lodger and have not yet logged into RevenueSA Online you can use your existing RevNet credentials to login.

From 1 January 2019, the annual payroll tax registration threshold increased to $1.5 million, however employers with wages of $600,000 or more must be registered and lodge an annual reconciliation in the 2018-19 financial year.

The maximum annual deduction entitlement has not changed and remains at $600,000.

The annual deduction entitlement will be reduced if the employer:

- is part of a group

- employs (or the group employs) in South Australia for part of the financial year; or

- employs (or the group employs) in South Australia and another state and/or territory.

For more information see our SA Deduction Entitlement educational video.

Payroll tax is based on a full financial year so what does that mean for the 2018-19 financial year?

Your liability will be based on your full 12 months Australia wide taxable wages.

But the year will be split into 2 periods – period 1 and period 2.

If your Australia wide taxable wages for the full financial are between $600,000 and $1.5 million you will be liable for payroll tax from 1 July 2018 to 31 December 2018.

However, you will not be liable for payroll tax from 1 January 2019 to 30 June 2019.

Please note: If your Australia wide taxable wages for the full financial year exceed $1.5 million you will be liable in both Period 1 and Period 2. Please refer to one of our other educational videos which explains this further.

For employers with annual Australia wide wages of $1.5 million or less this table shows your tax rate for the 2018-19 financial year.

From 1 July 2018 to 31 December 2018 the payroll tax rate will be between 2.5% and 4.95%.

The reduced rate is provided by way of ex gratia.

From 1 January 2019 to 30 June 2019 you are not liable so the rate will be zero.

RevenueSA Online will automatically calculate the correct rate and payroll tax payable for each period in the 2018-19 financial year when you complete your annual reconciliation.

Your monthly payroll tax rate during the financial year has been based on estimates, which were provided:

- in your 2017-18 annual reconciliation; or

- if this is your first annual reconciliation, the estimates provided when you registered; or

- if applicable, your amended estimates provided to RevenueSA.

The annual reconciliation is calculated on the actual wages paid during the 2018-19 financial year.

This means you may see a variance of the estimated rate of payroll tax applied to your monthly returns and the actual rate of payroll tax applied on your annual reconciliation.

Because of the changes to payroll tax from 1 January 2019, this financial year will have 2 separate periods.

During your annual reconciliation you are required to provide your South Australian wages for each period

- Period 1 which is from 1 July to 31 December 2018; and

- Period 2 which is from 1 January to 30 June 2019.

This will enable for the correct rate of payroll tax to be applied in each period.

Just a reminder, it is only your South Australian wages that need to be provided for each period.

Employers sometimes make lump sum payments. This can include superannuation tops ups, fringe benefits and bonuses.

If these payments relate to the full financial year you can split them across the 2 periods.

Let’s look at an example.

An employer pays employees a $5,000 bonus in recognition of their work through the financial year. The payment is made in June.

As the payment relates to the whole financial year, they can declare

- $2,500 in period 1 (1 July to 31 December 2018); and

- $2,500 in period 2 (1 January to 30 June 2019).

RevenueSA Online will automatically calculate the correct rate and payroll tax payable for each period in the 2018-19 financial year when you complete your annual reconciliation. This will be displayed on the Tax Payable Calculation screen.

Your Australia wide wages will determine your deduction entitlement and the rate of payroll tax that will be applied. It is not based on South Australian wages alone.

If you are grouped with other businesses that employ it is the Total Australia wide wages paid by all group members that is relevant.

Please note that if you are entitled to a reduced rate of payroll tax in period 1, this is provided by way of ex gratia.

As part of your annual reconciliation you provide wage estimates for the next financial year.

If you estimate that your Australia wide wages for 2019-20 will be $1.5 million or less you will be prompted towards the end of your Annual Reconciliation (at the wage estimates screen) to decide if you would like to cancel your payroll tax registration in South Australia.

It’s your choice if you remain registered or cancel.

To cancel you South Australian payroll tax registration, select Cancel Registration.

If your wages are close to the $1.5 million threshold or they fluctuate year to year, you may prefer to retain your registration in case you exceed the threshold in 2019-20.

To remain registered for payroll tax in South Australia for the 2019-20 financial year, select the continue with registration radio button.

If you remain registered and would like to change your return cycle please email your request to payrolltax@sa.gov.au.

If you remain registered you are still required to lodge returns,

If your estimated annual Australia wide wages are above $1.5 million, you will not be prompted with this question.

Please remember if you need help when completing the annual reconciliation you can click on the help link and a separate page will open detailing the steps required to complete the specific screen you are on.

That brings us to the end of this educational video.

If you require any additional assistance please contact us.

[Music]