General

Where can I find information on the changes to land tax?

Please see the land tax changes page to see what changes apply to you.

What rates are used to calculate land tax?

You can find the land tax rates on our Rates and Thresholds page.

The rates and thresholds are different for land held on trust. More information about trust rates can be found on the Rates and Thresholds page. Information about trusts can be found on the Land held on trust page.

Why have I received a Land Tax Assessment?

The use, site value and ownership of land each year at midnight 30 June determines your land tax payable.

If the combined site value of your taxable land is over the $482,000 threshold (or $25,000 for land held on trust), you will receive a Land Tax Assessment.

Changes to the way land held in different ownerships is grouped for assessment, started in the 2020-21 financial year, may mean you receive a Land Tax Assessment where you might not have received one before.

Why is this the first time I have received a Land Tax Assessment?

You could have received a Land Tax Assessment for the first time for any of the reasons listed below:

- The total taxable site value of land owned by you (and not held on trust) at midnight 30 June now exceeds $482,000.

- The total taxable site value of land held on trust, owned by you at midnight 30 June now exceeds $25,000.

- You have bought additional land in the last financial year.

- Land previously exempt from land tax no longer meets the exemption criteria.

- Your land is held across more than one ownership. An ownership consists of all the properties owned by the same owner or the identical group of owners.

- You are recorded as a beneficiary or unitholder for taxable land held on trust.

Why is my home included on my Land Tax Assessment? Shouldn’t this be exempt?

If your home was already exempt from land tax, as your ‘principal place of residence’, your exemption continues and the land will not be liable for land tax.

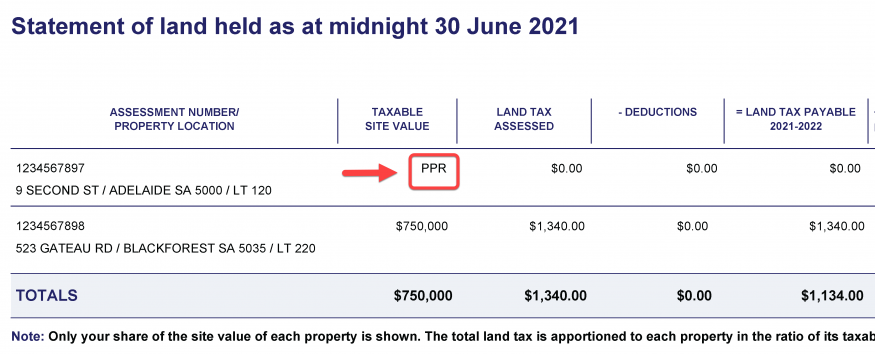

The Land Tax Assessment (PDF 948KB) lists all South Australian property that you own, or partly own, including land that is exempt from land tax. Previous Land Tax Notices of Assessment only listed taxable land.

On your Statement of land held (which is the last page of your Assessment), you will see a code next to your home’s details in the ‘Site Value’ column showing if it is exempt from land tax. If we have recorded it as your home (‘principal place of residence’), you will see the code ‘PPR’.

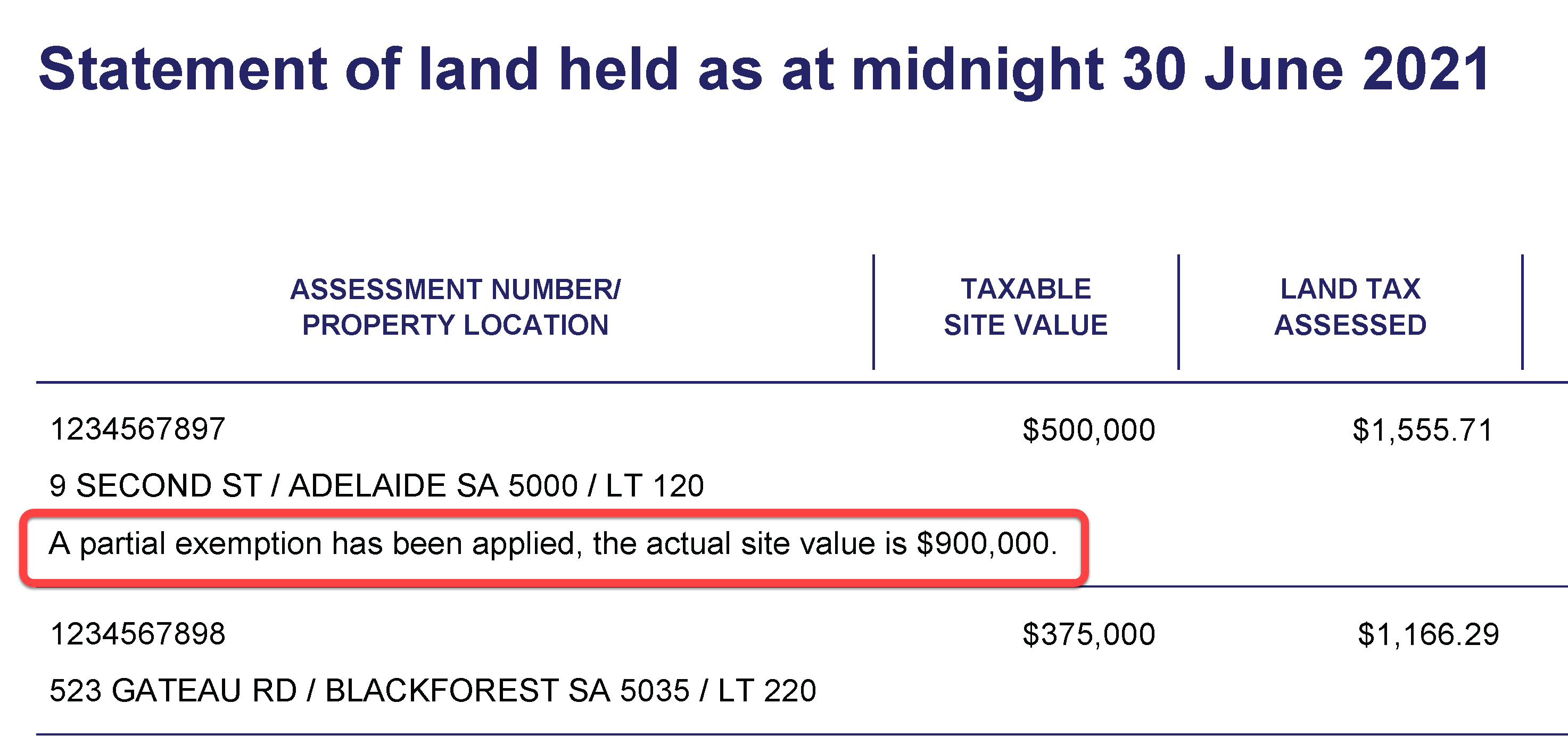

If a site value is displayed, an exemption has not been applied or partial exemption may have been applied. This means that land tax has been assessed against the land.

If you only receive a partial exemption, the value shown in the ‘Site Value’ column will reflect the proportion of the site value that attracts land tax. The partial exemption will be noted below the property description.

If your home does not currently have a principal place of residence exemption in place, please see our land tax exemption page for details on the principal place of residence exemption and how to apply.

Why is my home on my land tax assessment?

[music plays]

Why is my home on my Land Tax Assessment?

This video is intended as a guide only. We recommend you seek independent advice on state revenue matters and how they impact you and your circumstances.

[music fades]

Statement of land held shows all of the land you own or partly own in South Australia even if it’s not taxable land.

This could include your home or other exempt land. If the land is exempt, you’ll see a code instead of a dollar value in the site value column. You’ll also see an explanation of the codes at the bottom of your Statement of land held.

If you see a code, it means we have an exemption for your home and land tax isn’t charged on that property. If you see a value against the property it means that the land does not have an exemption or it only receives a partial exemption. Land that only receives a partial exemption will be indicated on your assessment.

If your exemption does not appear on your Land Tax Assessment you can apply online using the Apply for land tax exemption or relief form. Details about eligibility criteria and what you need to apply are available on our website.

Your land tax will need to be reassessed if your home was taxed and shouldn’t have been. Contact us for information.

[music plays]

If your land tax needs to be reassessed because your home was included in your original Land Tax Assessment and should have been exempt from land tax, call us on (08) 8372 7534.

More information can be found on the RevenueSA website.

[on screen no audio] www.revenuesa.sa.gov.au/landtax

[music fades]

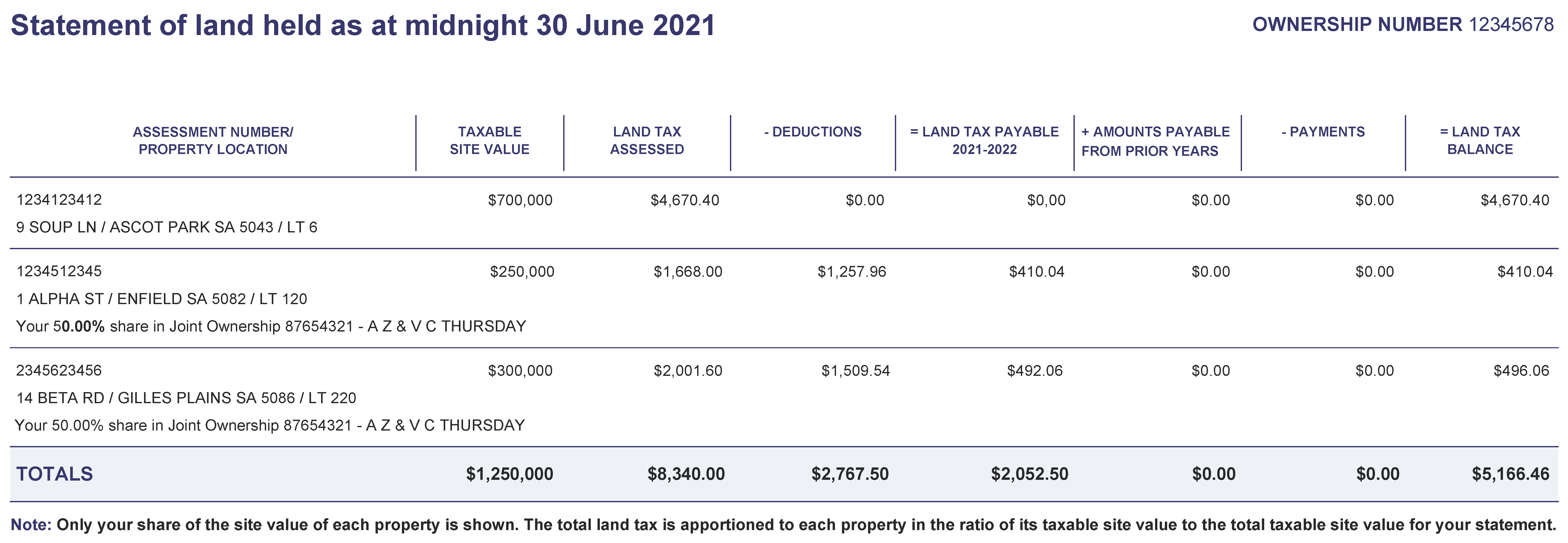

I have a deduction on my Land Tax Assessment. What is that and how is it calculated?

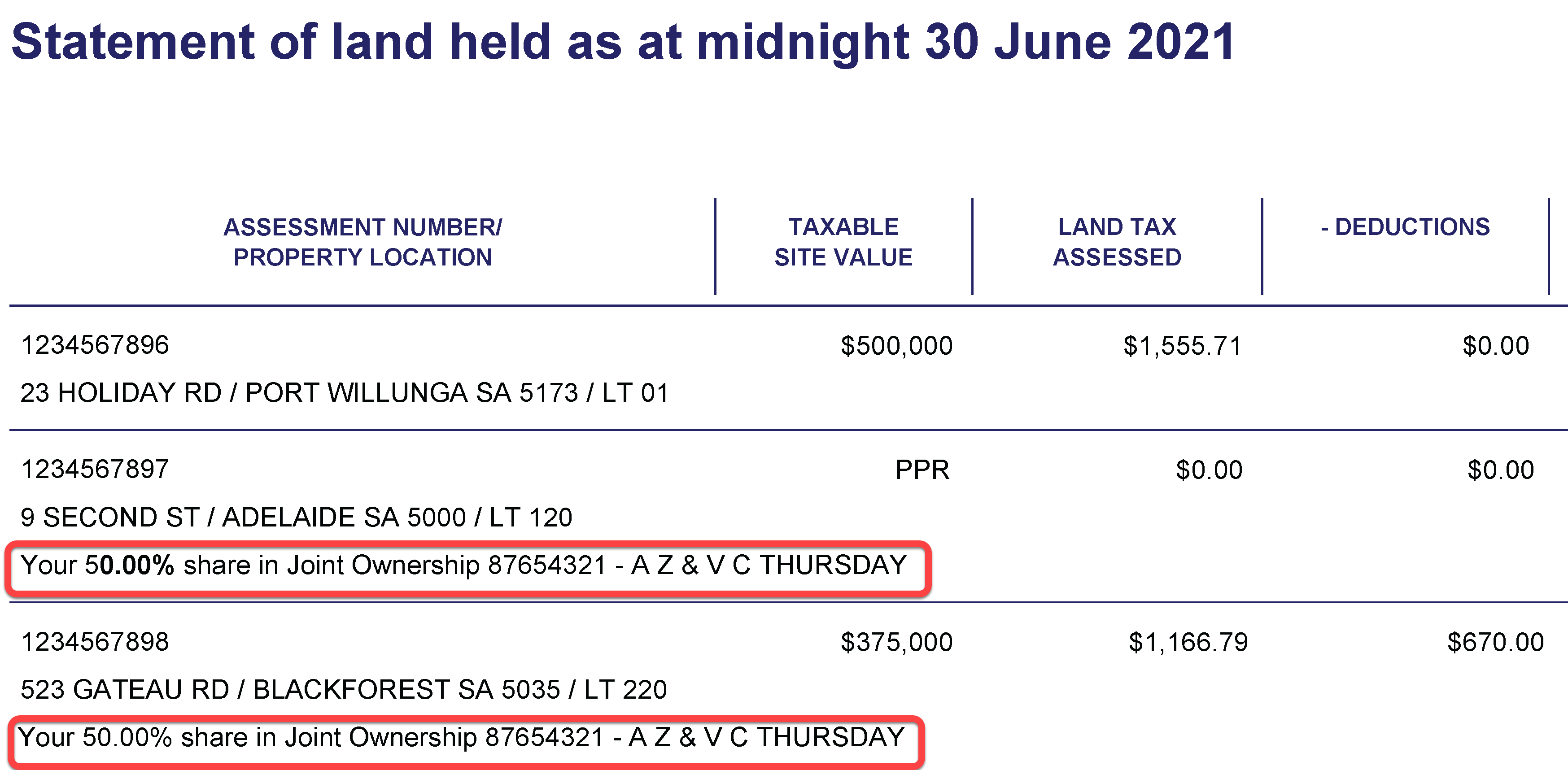

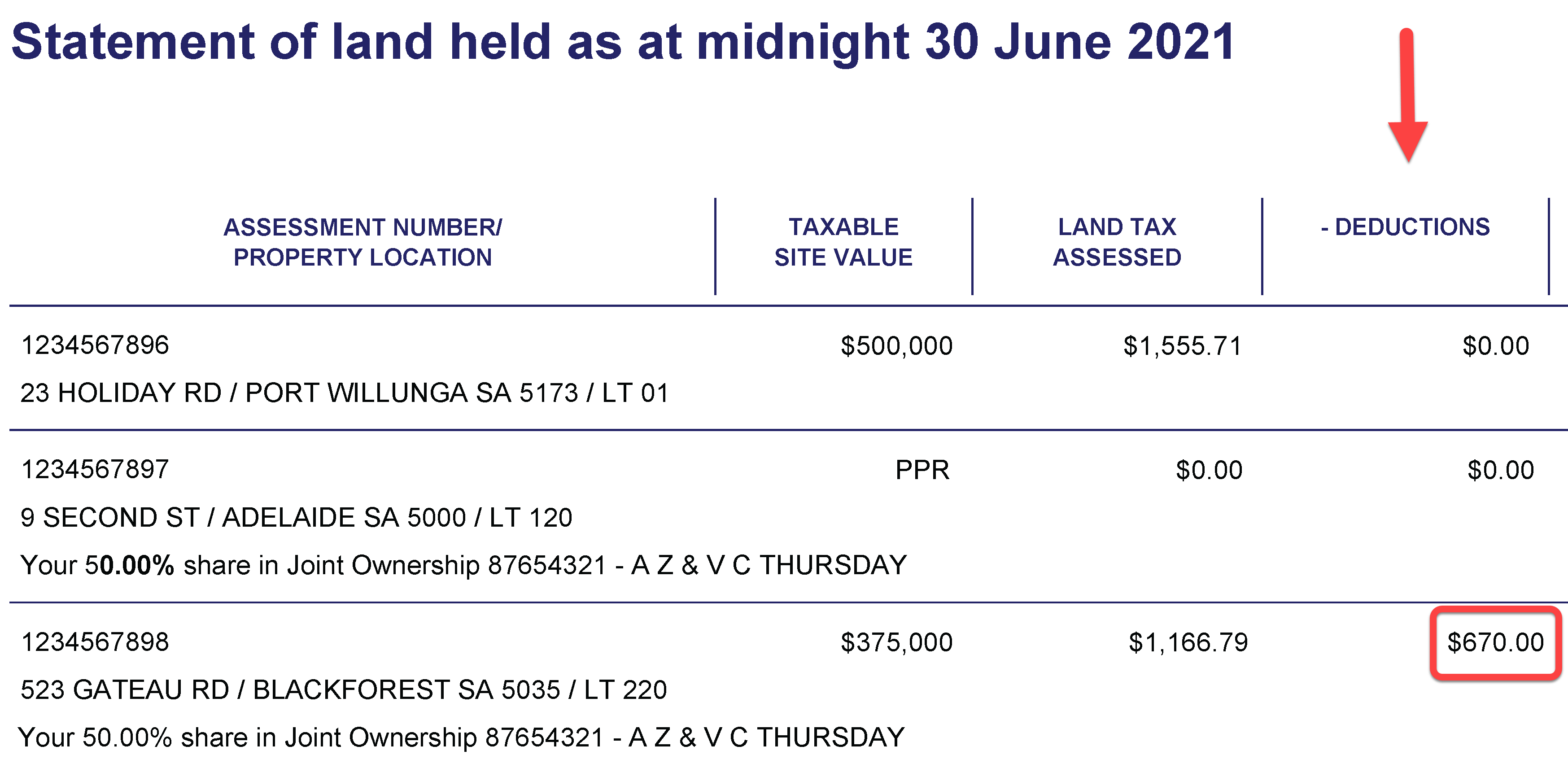

Where you own land jointly with another or others, the jointly owned land will be assessed firstly in the joint ownership.

You will then also be assessed individually on your share of the jointly owned land, along with any other land you own, or partly own.

To stop you being taxed again on land that attracts land tax in the joint ownership, you will receive a deduction to offset your individual land tax. The deduction is taken off the total of your individual land tax.

The deduction is equal to your share of the land tax charged to land in the joint ownership. If land tax is not applied in the joint ownership (for example, total site value is under the threshold), a deduction will not be available.

Where your total deduction is greater than your individual land tax liability, your land tax is reduced to zero and you will not receive a Land Tax Assessment on your individual holding.

I’m still paying my instalments for 2020-21. Can I still pay according to that assessment?

Your remaining instalments for your 2020-21 land tax assessment are now payable in instalment 1 of your 2021-22 Land Tax Assessment. You can view the balance outstanding in the ‘amount payable from prior years’ column on your 2021-22 Land Tax Assessment.

If you have concerns about paying by the due date, please see the payment options below.

Why is my INSTALMENT 1 more than my other instalments?

RevenueSA has experienced delays in the billing of some complex ownerships for the 2020-21 financial year.

As a result your first instalment may include:

- remaining instalments for your 2020-21 land tax assessment, and this is reflected in the ‘amount payable from prior years’ column on your 2021-22 Land Tax Assessment; and/or

- the full amount of your land tax if you have not yet received a Land Tax Assessment for the 2020-21 financial year for this ownership, and this is reflected in the ‘amount payable from prior years’ column on your 2021-22 Land Tax Assessment; and/or

- any unpaid land tax for previous financial years.

If you have concerns about paying by the due dates, we are here to help

Please contact us before the due date of your first instalment, you can:

The higher instalment 1 reflects your instalment payment for your 2021-22 land tax plus any amount payable from prior years (further explanation on reason is below).

You can choose to pay your land tax amount equally over the 4 instalments. The first instalment on your 2021-22 Land Tax Assessment includes one-quarter of your 2021-22 land tax plus any amount payable from prior years. Instalments 2, 3 and 4 are for the balance of your 2021-22 land tax.

For example, if your 2021-22 Land Tax Assessment includes land tax of $1,000 for 2021-22 plus $800 from prior years. Your existing instalments are as follows:

- Instalment 1 = $1,050

- Instalment 2 = $250

- Instalment 3 = $250

- Instalment 4 = $250

You can request to pay equally over your 2021-22 instalments:

- Instalment 1 = $450

- Instalment 2 = $450

- Instalment 3 = $450

- Instalment 4 = $450

To request this option, please complete the online request form and select ‘Pay over 4 instalments’. To complete this form you will need your ownership number and due date (located on the top right on the front page of your Land Tax Assessment).

Your request will be processed and a confirmation will be provided via email including details of your revised instalment amounts and due dates*.

* If you do not pay the full amount of an instalment by the due date, your total unpaid land tax balance will become payable and interest and penalty tax may apply. If you are unable to make payment before the due date, please contact RevenueSA to make alternative payment arrangements.

Refer to the back of your Land Tax Assessment for payment details.

If you require a longer payment plan, our Debt Management Services Team can assist you. Please complete the online request form and select ‘request a longer payment plan’.

To complete this form you will need your ownership number and due date (located on the top right on the front page of your Land Tax Assessment). You will also need to provide information on how much and how often you can make a payment.

We may ask for additional supporting information and if approved, confirmation will be provided via email including details of your revised payment plan and due dates*. Depending on the terms of the payment plan – some conditions may apply.

* If you do not pay the full amount of an instalment by the due date, your total unpaid land tax balance will become payable and interest and penalty tax may apply. If you are unable to make payment before the due date, please contact RevenueSA to make alternative payment arrangements.

Refer to the back of your Land Tax Assessment for payment details.

Can I make more frequent payments?

You can make more frequent payments (for example: monthly, fortnightly or weekly) using the payment reference. If you choose to make smaller payments, you must ensure the full amount of the instalment is paid by the instalment due date or contact us for an extension*.

For example instead of paying an instalment payment of $1,000 in one payment, you can make smaller payments over a number of weeks, as long as you ensure the $1,000 has been paid by the due date*.

* If you do not pay the full amount of an instalment by the due date, your total unpaid land tax balance will become payable and interest and penalty tax may apply. If you are unable to make payment before the due date, please contact RevenueSA to make alternative payment arrangements.

Refer to the back of your Land Tax Assessment for payment details.

I’m having difficulty paying. What should I do?

Payment by quarterly instalments is provided for land tax. If you wish to organise a payment arrangement, please contact RevenueSA on 8226 3750 (option 2) before the due date on your Land Tax Assessment.

Why is the same property showing on more than one Land Tax Assessment?

Where you own land jointly with another, or others, it may appear on more than one Land Tax Assessment.

Where land is own by joint owners, it will be firstly assessed in the joint ownership, and a Land Tax Assessment will be issued if land tax is applicable.

Individual owners will also be assessed on their share of jointly owned land, along with any other land that they own, or partly own, and a Land Tax Assessment will be issued if land tax is applicable. Partly owned land is identified under the property location details on your individual assessment.

If land tax is payable in the joint ownership, a deduction will be offset against your individual liability. This will be reflected in the ‘Deduction' column on your Statement of land held.

Where your total deduction is greater than your individual land tax liability, your land tax is reduced to zero and you will not receive a Land Tax Assessment on your individual holding.

[music plays]

Why is my property on more than one Land Tax Assessment?

This video is intended as a guide only. We recommend you seek independent advice on state revenue matters and how they impact you and your circumstances.

[music fades]

From 2020-21 changes were introduced to the way land tax in South Australia is assessed and charged.

One of the changes is how land owned by joint owners is taxed.

If land is owned by 2 or more people, it is assessed in the joint ownership and land tax is charged to the joint ownership.

Then, and this is new from 2020-21, each individual owner is separately assessed on their share of the jointly owned land along with any other land they own.

It means property can show on a joint Land Tax Assessment and then also on the individual Land Tax Assessment of each individual owner.

There are measures in place to stop people being double taxed on the same property that shows on more than one Land Tax Assessment.

See our website for more videos and more information.

[music plays]

More information can be found at www.revenuesa.sa.gov.au/landtax.

[music fades]

My Land Tax Assessment shows land I own with others – have I been taxed twice?

No, you may see the property appear on 2 Land Tax Assessments (the joint ownership and your individual ownership), but you have not been taxed twice.

Taxable land you own with others will be assessed in the joint ownership and an Assessment may be issued to the joint owners.

Your share in the land will also be assessed along with any taxable land you own or partly own and a deduction of your share of the land tax paid in the joint ownership will apply. An Assessment may be issued to your individual ownership which will show all land that you own or partly own.

[music plays]

Am I being charged land tax twice? Or, what happens when a property is on more than one Land Tax Assessment?

This video is intended as a guide only. We recommend you seek independent advice on state revenue matters and how they impact you and your circumstances.

[music fades]

In 2020-21 changes were introduced to the way land tax in South Australia is assessed and charged.

The changes mean that a parcel of land may appear on more than one Land Tax Assessment where it has more than one owner.

The same property could show on the joint ownership’s assessment and a share of the property could show on the individual owners’ assessments.

To stop people being taxed again on land already fully taxed in the joint ownership, individuals may receive a deduction which offsets their individual land tax.

A deduction is equal to an individual’s share of the land tax applied to the joint ownership.

In many cases the deduction will completely wipe out the individual’s land tax and where this happens, no Land Tax Assessment will be sent to that individual.

However, where the deduction doesn’t cancel out the individual’s land tax they will still receive an assessment which will be reduced by the amount of their deduction.

[music plays]

More information can be found at www.revenuesa.sa.gov.au/landtax

[music fades]

I own a property jointly with someone. We received a joint Land Tax Assessment and I received an individual Land Tax Assessment, but they didn’t receive anything. Why is that?

There are 2 main reasons that one owner could receive an individual Land Tax Assessment, while another owner does not.

One owner may not receive a Land Tax Assessment for either of these reasons:

- The deduction they receive offsets their individual land tax liability in full.

- The combined site value of taxable land they own, or partly own is below the land tax threshold.

I own land jointly, but don’t have a deduction showing on my individual Land Tax Assessment. Why is that?

A deduction will only apply when land tax is applicable in the joint ownership. If a deduction does not appear on your individual Land Tax Assessment, this means that no land tax has been applied in the joint ownership, most likely as the combined taxable site value is below the minimum land tax threshold.

How is land tax assessed for owners who own land jointly with another?

Land owned by joint owners, will be firstly assessed in the joint ownership, and a Land Tax Assessment will be issued if land tax is applicable.

Individual owners will also be assessed on their share of jointly owned land, along with any other land that they own, or partly own, and a Land Tax Assessment will be issued if land tax is applicable. Partly owned land is identified under the property location details on your individual assessment.

If land tax is payable in the joint ownership, a deduction will be offset against your individual liability. This will be reflected in the ‘- Deduction' column on your Statement of land held.

Where your total deduction is greater than your individual land tax liability, your land tax is reduced to zero and you will not receive a Land Tax Assessment on your individual holding.

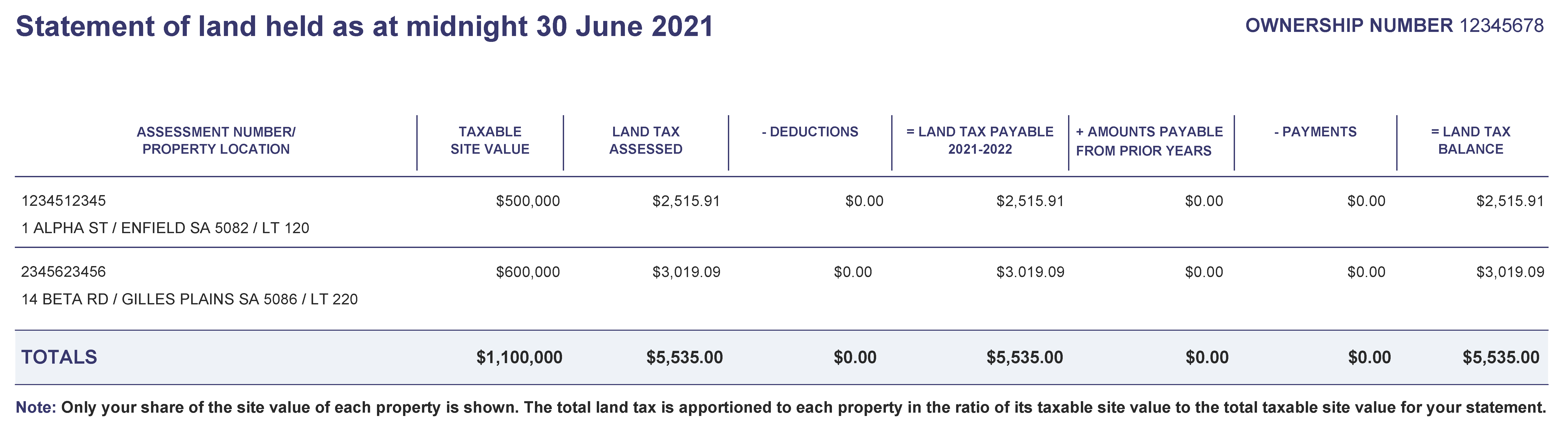

Example

Chau and Dai Nguyen own land together. They each have an equal share. Their joint Land Tax Assessment shows their jointly owned land:

- 1 Alpha Street, site value of $500,000

- 14 Bett Road, site value $600,000

Chau’s individual Land Tax Assessment shows her half of the jointly owned land, plus the other land she owns in her own right:

- 1 Alpha Street - 50% share of ownership #123456 Chau and Dai Nguyen, site value of $250,000 (half of the total site value of the property)

- 14 Bett Road, 50% share of ownership #123456 Chau and Dai Nguyen, site value of $300,000 (half of the total site value of the property)

- 9 Soup Lane, site value of $700,000

Chau receives a deduction for her share of the land tax applied to the joint ownership, but it doesn’t completely wipe out her individual land tax.

She will receive a Land Tax Assessment on her site value of $250,000 + $300,000 + $700,000 (with a deduction for her share of the land tax applied to the joint ownership on the jointly owned properties).

Dai does not own any land in his own right. His properties would show as:

- 1 Alpha Street, 50% share of ownership #123456 Chau and Dai Nguyen, site value of $250,000 (half of the total site value of the property)

- 14 Bett Road, 50% share of ownership #123456 Chau and Dai Nguyen, site value of $300,000 (half of the total site value of the property)

Dai receives a deduction for his share of the land tax applied to the joint ownership. In his case, it completely offsets his individual land tax.

Dai does not receive an individual Land Tax Assessment.

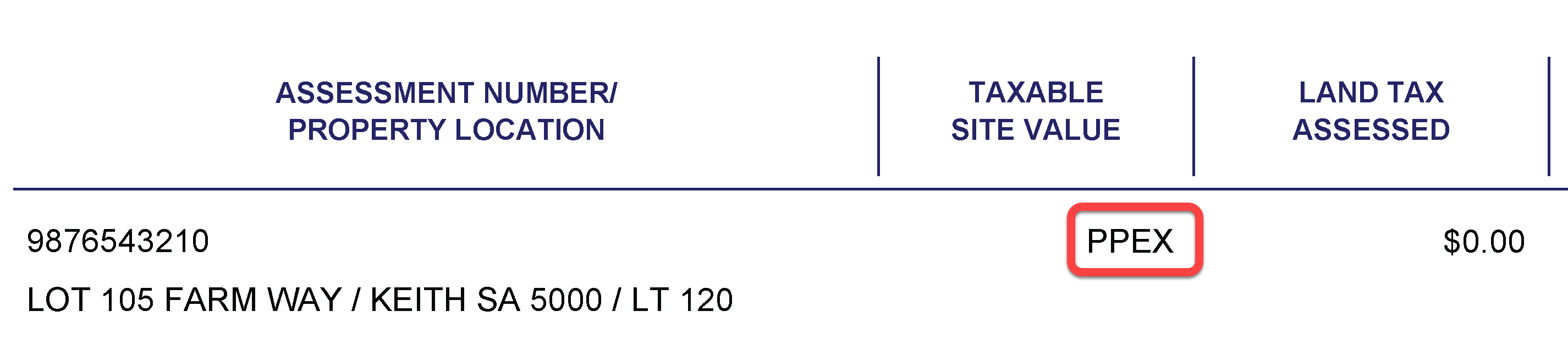

Why is my exempt primary production land showing on my Land Tax Assessment?

If your land was already exempt from land tax, as it is used for primary production, your exemption continues and the land will not be liable for land tax.

The Land Tax Assessment (PDF 948KB) lists all South Australian property that you own, or partly own, including land that is exempt from land tax. Previous Land Tax Notice of Assessments only listed taxable land.

On your Statement of land held (which is the last page of your Assessment), you will see a code next to the land used for primary production in the ‘Site Value’ column if it is exempt from land tax. If we have recorded it as used for the business of primary production, you will see the code ‘PPEX’ beside your property.

[music plays]

Why is my exempt land on my Land Tax Assessment?

This video is intended as a guide only. We recommend you seek independent advice on state revenue matters and how they impact you and your circumstances.

[music fades]

Statement of land held shows all of the land you own or partly own in South Australia, even if it’s not taxable land.

This could include property that is exempt from land tax, such as land used for primary production.

If the land is exempt, you’ll see a code instead of a dollar value in the site value column.

You’ll also see an explanation of the codes at the bottom of your Statement of land held.

If you see a code, it means we have an exemption for your land and that property’s value doesn’t count towards your total taxable site value.

No tax is charged on that property.

If your exempt land shows on your Statement, but it has a dollar value it means that we don’t have an exemption recorded for that property.

You can apply for an exemption using the online Apply for land tax exemption or relief form.

Details about the eligibility criteria and what you need to apply are available on our website.

If your application is approved, your land tax will be reassessed and a new Land Tax Assessment will be issued, showing the exemption.

Contact us for information.

[music plays]

If your land tax needs to be reassessed because your exempt land was included in your original Land Tax Assessment and should have been exempt from land tax, call us on (08) 8372 7534.

More information can be found on the RevenueSA website.

[on screen no audio] www.revenuesa.sa.gov.au/landtax

[music fades]

Has my exemption been removed?

No. No existing exemptions were removed as part of the land tax changes.

The Land Tax Assessment (PDF 948KB) lists all South Australian property that you own, or partly own, including land that is exempt from land tax. Previous Land Tax Notice of Assessments only listed taxable land.

If your land was already exempt from land tax, maybe as it is your home (known as your principal place of residence) or it is used for primary production, your exemption continues and the land is not liable for land tax. However it will still appear in your Land Tax Assessment with an exemption code beside the property details on your Statement of land held (the last page of your Assessment).

If the land listed on your Statement of land held does not currently have an exemption in place and you believe you are eligible, please see our land tax exemption page for details on exemptions and how to apply.

What relief is available if my land tax has increased?

If your 2021-22 land tax has increased by between $2,500 and $102,500 compared to your 2019-20 land tax and that increase is due to the new method of aggregation, you may be eligible for land tax relief.

The increase must be due to the new method of aggregation, and not due to the introduction of new rates for trusts, purchasing additional land, an exemption from land tax no longer applying, an increase in site value or unpaid land tax from previous years.

The value of relief will be calculated on 70% of the difference between land tax payable, compared to the land tax that would have been payable on the relevant land under the aggregation approach, tax rates and thresholds that applied in 2019-20.

You can apply online for relief.

Visit the Transitional Land Tax Relief page for more information and eligibility for the 2020-21, 2021-22 and 2022-23 financial years.

How do I apply for relief if my land tax is higher this year?

You can apply online for relief .

Visit the Transitional Land Tax Relief page for more information and eligibility, including how to apply.

Why is the land tax different in on our Individual Assessments when we own equal share in the land?

Your Individual Assessment is calculated on the total site value of your land holdings, which includes land you own individually and your share in land owned with others. Your total land tax is then apportioned back to each parcel of land you have an interest in.

This means, whilst you may own an equal share in a parcel of land (for example, 2 owners own 50% each), the land tax that is assessed in your individual ownership can differ. An example best explains this.

Brian and Poppy equally own land with a site value of $500,000 which is assessed with land tax of $90.00. The joint ownership will be issued a Land Tax Assessment for $90.00.

Both Brian and Poppy will receive a deduction against their Individual Assessment of $45.00 (based on 50% share).

Brian also owns a parcel of land with a site value of $300,000. His Individual Assessment would be as follows:

Land A

$250,000 (being 50% share of $500,000)

Land B

$300,000 (100%)

Land tax of $340.00 is assessed on the total site value of $550,000.

His Individual Assessment will show the following:

| Land tax assessed | Less deduction from joint ownership | Land tax payable | |

|---|---|---|---|

| Land A | $154.55 | $45.00 | $109.55 |

| Land B | $185.45 | n/a | $185.45 |

| TOTALS | $340.00 | $45.00 | $295.00 |

Poppy also owns 2 parcels of land with site values of $300,000 and $150,000 respectively. Her Individual Assessment would be as follows:

Land A

$250,000 (being 50% share of $500,000)

Land B

$300,000 (100%)

Land C

$150,000 (100%)

Land tax of $1,090.00 is assessed on the total site value of $700,000

Her Individual Assessment will show the following:

| Land tax assessed | Less deduction from joint ownership | Land tax payable | |

|---|---|---|---|

| Land A | $389.29 | $45.00 | $344.29 |

| Land B | $467.14 | n/a | $467.14 |

| Land C | $233.57 | n/a | $233.57 |

| TOTALS | $1,090.00 | $45.00 | $1,045.00 |

Why have I not received my land tax assessment yet?

Due to the land tax reforms we are implementing a wide range of changes and billing for your ownership may not have occurred as of yet. Your land tax assessment will be issued in due course and this will not affect the length of time that you have in order to pay.

What do I do if I think my Land Tax Assessment is wrong?

The main reasons your Land Tax Assessment could be different to what you estimated or expected:

- Your site value is different to what you expected.

- The land listed on your Land Tax Assessment is not a complete list of all the land you own, or partly own.

- You do not own some or all of the land listed on your Land Tax Assessment.

If your site value is different to what you expected, see What if I disagree with the site value on my Land Tax Assessment?

If you think your Assessment is wrong for any other reason, we have an online form where you can lodge queries or concerns about your Land Tax Assessment.

Please have your ownership number or assessment number with you when you complete the form.

What if I disagree with the site value on my Land Tax Assessment?

We use values provided to us by the Valuer-General when calculating land tax.

If you disagree with the valuation, you may lodge an objection with the Valuer-General.

What to do

Site values are determined on an annual basis by the Valuer-General as part of a general valuation and each new valuation comes into force from 1 July to 30 June of a financial year, then it is superseded by a new valuation coming into force for the following 1 July.

Section 24(1) of the Valuation of Land Act 1971 provides that an Objection to the Valuer-General cannot be lodged against a site value that is no longer in force. You cannot lodge an objection to a valuation for a previous financial year.

If you received your Land Tax Assessment for the 2020-21, 2021-22, 2022-23, 2023-24 and/or 2024-25 financial year(s) after 1 July 2025, you may send a request to RevenueSA for a review the site value no longer in force.

If you do not agree with the statutory valuation referred to in the Land Tax Assessment (site value) for the current financial year, you may lodge an objection with the Valuer-General.

You must lodge an objection within 60 days of receiving the first rate notice from any rating authority for the financial year. An objection is a formal process and there are specific legislative requirements under the Valuation of Land Act 1971 for both you and the Valuer-General.

If you wish to lodge an objection for multiple properties or you also want to object to your capital value (Emergency Services Levy), you need to complete and lodge a separate form for each value and property.

Prior to lodging a formal objection, you can seek further information or clarification by contacting the Office of the Valuer-General via Land Services SA on the below contact number.

Your objections to the statutory valuation can be directed to the Office of the Valuer-General.

Online:

Complete the on-line objection form at www.valuergeneral.sa.gov.au/valuation/objecting-to-a-valuation

Email:

Mail:

Office of the Valuer-General

GPO Box 1354

ADELAIDE SA 5001

Phone:

1300 653 346

If you lodge an objection, you are still required to pay your land tax by the due date. If your objection results in an amendment to the value, then a refund may be issued.

If you received your Land Tax Assessment for the 2020-21, 2021-22 and/or 2022-23 financial year(s) after 1 July 2023, you may send a request to RevenueSA for a review of the site value no longer in force.

Site values are determined on an annual basis by the Valuer-General as part of a general valuation and each new valuation comes into force from 1 July to 30 June of a financial year, then it is superseded by a new valuation coming into force for the following 1 July.

Section 24(1) of the Valuation of Land Act 1971 provides that an Objection to the Valuer-General cannot be lodged against a site value that is no longer in force.

Due to delays in issuing some land tax assessments following the changes required to implement land tax reform, the Commissioner of State Taxation and the Valuer-General have agreed to a temporary administrative arrangement to allow landowners to have site values reviewed that are not in force pursuant to the Valuation of Land Act 1971.

If a landowner receives a Land Tax Assessment for the 2020-21, 2021-22, 2022-23, 2023-24 and/or 2024-25 financial years after 1 July 2025, where the site value on the notice is no longer in force, and does not agree with the statutory site valuation referred to in the Land Tax Assessment, they may lodge a request for a review with RevenueSA. Your request must be within 60 days of receiving the first Land Tax Assessment from RevenueSA for the respective financial year.

Where the land owner receives a Land Tax Assessment for the current 2025-26 financial year, then you can lodge an objection with the Valuer-General within 60 days of the first notice and in accordance with the provisions of the Valuation of Land Act 1971. View more information on objecting to a value.

The approach for each financial year is summarised below:

Financial Year of Land Tax Liability

Land Tax Assessment issued after 1 July 2025

2025-26

Lodge a site value Objection with the Office of the Valuer-General within 60 days of receiving the Land Tax Assessment.

2024-25

Lodge a site value review via email with RevenueSA at RevData@sa.gov.au within 60 days of receiving the Land Tax Assessment.

2023-24

Lodge a site value review via email with RevenueSA at RevData@sa.gov.au within 60 days of receiving the Land Tax Assessment.

2022-23

Lodge a site value review via email with RevenueSA at RevData@sa.gov.au within 60 days of receiving the Land Tax Assessment.

2021-22

Lodge a site value review via email with RevenueSA at RevData@sa.gov.au within 60 days of receiving the Land Tax Assessment.

2020-21

Lodge a site value review via email with RevenueSA at RevData@sa.gov.au within 60 days of receiving the Land Tax Assessment.

A review of your Land Tax Assessment, including taking into consideration advice from the Valuer-General on the site value, is at the Commissioner of State Taxation’s discretion and will be on a case-by-case basis. The Commissioner of State Taxation’s decision to undertake a review will take into consideration, amongst other things, whether or not the delay in issuing a Land Tax Assessment resulted in you not being able to lodge the Objection with the Valuer-General prior to the end of the relevant financial year.

If, as a result of a site value review, the Valuer-General advises RevenueSA of an updated site value, the updated site value will be recorded in RevenueSA’s system and the updated site value will be used by RevenueSA for land tax purposes only. The site value on the valuation roll, which has been adopted by other rating agencies that use the value, will not be updated.

Further, as the site valuation review process is an administrative arrangement, should you disagree with the outcome of the site value review you do not have the ability to object, or seek a further review of the decision under the Valuation of Land Act 1971.

If you lodge a review you are still required to pay your land tax by the due date. If the review results in an amendment to the site value, then a refund or a new Land Tax Assessment may be issued.

Why has my apartment been taxed? I don't have any land.

While you may not have any physical land, your apartment is built on land and a site value is determined for each apartment by the Valuer-General. This site value may still attract land tax.

Why have I received a Land Tax Assessment for my unit/townhouse etc.?

As the owner of the unit/townhouse etc., you are seen as the owner for land tax purposes.

A site value is determined by the Valuer-General for each unit/townhouse etc., which is used to assess land tax.

If your unit/townhouse is owned under a strata title or a community title, your site value will not include common property (for example shared driveways). The relevant community or strata corporation will be liable for any common land that attracts land tax.

Why have I received a Land Tax Assessment for my shack site?

As the holder of a shack site lease, you are seen as the owner for land tax purposes.

The lessee (holder of the lease) has been recognised as the owner for land tax purposes since 1989. This means your shack site may be assessed along with any other land you own for land tax.

My question isn’t answered above. Where can I go for information?

If you have any questions which aren’t answered here, we have an online form where you can lodge queries about your Land Tax Assessment

Land held on trust

I hold land on trust, what does this mean for the Land Tax Assessment?

Land you hold on trust may be taxed at the Trust land tax rates, which includes a surcharge of up to 0.5% on the general land tax rates and a lower threshold of $25,000.

Please see our land held on trust page for more information.

Who is the owner of land held on trust?

For land tax, the trustee is generally treated as the owner of land held on trust. The land is assessed in a separate ownership from any other land the trustee owns outside of the trust.

Where beneficiaries or unitholders are nominated, they will also be treated as owners for the purposes of land tax.

I own land on trust, why does it appear on my individual Land Tax Assessment?

Where RevenueSA has not been notified of the trust ownership of land, the land will appear in the trustee’s ownership (as per the registered ownership details on the Title for the land)

Trustees are obligated to tell RevenueSA where they hold land on behalf of a trust within 30 days of acquiring the land.

See land held on trust page for more information.

Is all land held on trust subject to the trust land tax rates?

Only discretionary trusts, fixed trusts and unit trusts are liable for the trust land tax rates. Other types of trusts are excluded from the trust rates and will be taxed at general land tax rates.

In certain circumstances, if the trust’s beneficiary(ies) or unitholder(s) have been nominated, the land will be assessed at general land tax rates, not trust land tax rates. It will also be assessed in the individual ownerships of all of the beneficiaries or unitholders.

See land held on trust page for more information.

Why does my ownership number start with a T?

Trust held properties are now recognised in Ownership Numbers beginning with ‘T’.

Please ensure that you use the correct payment reference number as it appears on your Land Tax Assessment as this may be different from payment reference numbers provided to you in the past.

Why is my land tax higher than previous years?

Land held in trust is assessed at higher trust surcharge rates.

For more information on the assessment of land tax for land held trust see our land held on trust page.

Do all trusts attract the surcharge?

Some trusts are excluded from the surcharge, for example a superannuation trust.

To find out which types of trusts are excluded from the trust surcharge see our land held on trust page.

Some trusts may also nominate a designated beneficiary, unitholders or beneficiaries to have their land tax assessed at the general rates. If the trust chooses to nominate:

- Discretionary trusts can nominate a designated beneficiary (for land held as at midnight 16 October 2019) up until 31 December 2021

- Unit trusts must nominate all their unitholders

- Fixed trusts must nominate all their beneficiaries

Please note: by nominating a designated beneficiary, unitholders or beneficiaries, they may also be liable for land tax for the land held on trust. The land (or share in the land) may be assessed along with any other land they own and they may receive an individual land tax assessment. You should seek independent advice before nominating.

For more information on nominating a designated beneficiary, unitholders or beneficiaries and how land tax is assessed see our land held on trust page.

I nominated a designated beneficiary, why have you not assessed the land at the general rates?

Where all required information has been lodged, the designated beneficiary will be acknowledged and land tax assessed at the general rates.

You may have been charged at the trust rates because the:

- Statutory declaration has not been completed, or incorrectly compiled by the designated beneficiary.

- Trust deed has not been provided to RevenueSA.

- Land held by a discretionary trust was purchased or acquired on or after 17 October 2019.

For more information on nominating a designated beneficiary and evidence required see our land held on trust page.

My discretionary trust purchased/acquired land on or after 17 October 2019, why can’t I nominate a designated beneficiary?

The ability to nominate a designated beneficiary for land held by a discretionary trust is a concession provided to land owned as at the date the land tax reforms were introduced into Parliament (16 October 2019).

This means designated beneficiaries will only be acknowledged for land held on trust as at midnight, 16 October 2019. Any land purchased or acquired by the trust after this date is subject to the trust surcharge rates.

My trust held land as at 16 October 2019 and I have also purchased/acquired additional land since. What happens with the tax?

The land tax is calculated using a pro rata method based on the site values of the land held pre-16 October 2019 and the land held post-16 October 2019.

For more information on how land tax is calculated see our land held on trust page.

My land is held on trust but I haven’t advised RevenueSA, what do I need to do?

You must notify RevenueSA, using the online Trust Notification Advice, of any land held on trust or within one month of acquiring any land on trust. Once you have notified RevenueSA you don’t need to notify each financial year, unless some change has occurred in respect of that trust that might affect its liability to tax.

For more information on when and what you need to advise see our land held on trust page.

Corporations

How are related corporations billed for land tax?

Where corporations are related, all the land that the corporations own is grouped together and assessed for land tax as though all the land is owned by one corporation (other than land held by a corporation as trustee of a trust). The group of corporations is referred to as a Corporate Group.

Why am I part of a Corporate Group?

Land owned by corporations which are considered to be related will be grouped together and assessed as though it was all owned by one owner.

Corporations are considered to be related for land tax purposes when:

- control is exercised by a corporation over another/other corporations;

- control is exercised by the same person(s) over 2 or more corporations;

- control is exercised jointly by a corporation and its shareholders, who between them own more than 50% of issued share capital, over another corporation;

- a corporation owns more than 50% of the beneficial interests/units in land subject to a fixed trust/unit trust; or

- where 2 corporations are related, a third corporation will be grouped if it is related to at least one of them.

You can find out more about how related corporations are treated for land tax on the Related Corporations page.

Who will receive the Land Tax Assessment for a Corporate Group?

Where related corporations are jointly assessed for land tax, one Land Tax Assessment is issued for the group and will be sent to the postal address deemed most appropriate by RevenueSA upon creation of the Corporate Group.

The Land Tax Assessment will specify each land owning related corporation, the land owned by the related corporations and the percentage interest each corporation has in the land taxed.

Should a Corporate Group want to change the postal address that their Land Tax Assessment is issued to, a representative of the group can do so by completing the Lodge a Land Tax Query form (select option Update billing details for Corporate Group).

I'm a corporation but haven't got a Land Tax Assessment. What's happening?

You may have been grouped together with other corporations as part of a related corporate group. See Why am I part of a corporate group? for details about related corporations.

Where related corporations are jointly assessed for land tax, one Land Tax Assessment is issued for the group and will be sent to the postal address deemed most appropriate by RevenueSA upon creation of the Corporate Group.

The corporation that received the Land Tax Assessment may be in contact with you for your share of the total land tax liability.

You may also not yet have received a Land Tax Assessment because your corporation holds land jointly, or holds land on trust, or is a beneficiary of land held on trust.

Why does my Land Tax Assessment show land owned by other corporations?

If you are considered to be related to other corporations, all the land owned by those related corporations is now assessed as though it was owned by one owner.

You can learn more on the related corporations page.

It means that the land owned by all members of the Corporate Group appear on one Land Tax Assessment that is issued for the group and sent to the postal address deemed most appropriate by RevenueSA upon creation of the Corporate Group.

The Land Tax Assessment will specify each land owning related corporation, the land owned by the related corporations and the percentage interest each corporation has in the land taxed.

What happens if a corporation owns land as trustee of a trust?

Land owned by a corporation as trustee of a trust will not be assessed with other land owned by the Corporate Group and will be assessed separately.

To advise of land held on trust, please use the online Trust Notification Advice.

For more information please see the land held on trust page.

Who is liable for the Land Tax Assessment?

As has always been the case, all owners listed on a Land Tax Assessment are equally and severally liable to make sure the land tax is paid. This means that each members is responsible for making sure that the liability is paid on time.

The burden of the land tax is distributed between the related corporations in the relative proportions of the value of their interests in the taxable land.

The Land Tax Assessment for related corporations lists all the related corporations.

If the Corporate Group’s land tax liability is paid by one of the related corporations, that corporation can recover a proportionate amount from each of the related corporations based on the value of each of the related corporations’ land holding interests. RevenueSA has no involvement in this.

How do I know how much I owe?

The land tax assessed against each parcel of land held by the members of the Corporate Group is displayed on the Land Tax Assessment.

If you are a member of a Corporate Group and would like to receive a copy of your group’s Land Tax Assessment, you can email landtax@sa.gov.au, quoting the ownership number for the Corporate Group or the name of the company you represent, and a copy of the Land Tax Assessment will be issued to you.

Notices

Why is this the first time I have received a Land Tax Assessment?

There are 4 main reasons why you may have received a Land Tax Assessment for the first time:

- the total taxable site value of all taxable land owned by you as at midnight, 30 June may now exceed the threshold of $482,000, or if held on trust exceeds the threshold of $25,000;

- if you own land in multiple ownership, your share of land owned is now combined in your individual Land Tax Assessment;

- you may have bought additional land in the last financial year; or

- land previously exempt from land tax may now no longer satisfy the exemption criteria.

Can I have a separate notice for each property?

No. The Land Tax Act 1936 requires land tax to be calculated on the basis of the total taxable site value of all land owned (by an owner or a group of owners) as at midnight 30 June.

Aggregation of the value of all properties of an owner for land tax assessment purposes is applied by all Australian jurisdictions that impose land tax. It is not considered equitable that 2 owners holding land identical in total value, one with one property and the other with 2 or more properties should pay different amounts of land tax.

What does ANR and ORS mean?

ANR means 'Another' and ORS means 'Others'.

If a property is purchased by 2 entities, both names are registered on the certificate of title, however our ownership record will show the first named on the certificate of title, with the other name abbreviated to ANR

Example:

A property purchased by Joe Boggelsworth & Mary Smith would have both names registered on the certificate of title, but as Joe's name was registered first, our ownership record will display as 'J Boggelsworth & ANR'.

If a property is purchased by more than 2 entities, all names are registered on the certificate of title, however our ownership record will show the first named on the certificate of title, with all other names abbreviated to ORS.

Example:

A property purchased by Bloggs Pty Ltd, Mary Smith Inc and Jim Brown would have all names registered on the certificate of title but as Bloggs Pty Ltd was registered first, our ownership record will display as 'Bloggs Pty Ltd & ORS'.

Why is INSTALMENT 1 more than my other instalments?

RevenueSA has experienced delays in the billing of some complex ownerships for the 2020-21 financial year.

As a result your first instalment may include:

- remaining instalments for your 2020-21 land tax assessment, and this is reflected in the ‘amount payable from prior years’ column on your 2021-22 Land Tax Assessment; and/or

- the full amount of your land tax if you have not yet received a Land Tax Assessment for the 2020-21 financial year for this ownership, and this is reflected in the ‘amount payable from prior years’ column on your 2021-22 Land Tax Assessment; and/or

- any unpaid land tax for previous financial years.

If you have concerns about paying by the due dates, we are here to help.

Please contact us before the due date of your first instalment, you can:

The higher instalment 1 reflects your instalment payment for your 2021-22 land tax plus any amount payable from prior years (further explanation on reason is below).

You can choose to pay your land tax amount equally over the 4 instalments. The first instalment on your 2021-22 Land Tax Assessment includes one-quarter of your 2021-22 land tax plus any amount payable from prior years. Instalments 2, 3 and 4 are for the balance of your 2021-22 land tax.

For example, if your 2021-22 Land Tax Assessment includes land tax of $1,000 for 2021-22 plus $800 from prior years. Your existing instalments are as follows:

- Instalment 1 = $1,050

- Instalment 2 = $250

- Instalment 3 = $250

- Instalment 4 = $250

You can request to pay equally over your 2021-22 instalments:

- Instalment 1 = $450

- Instalment 2 = $450

- Instalment 3 = $450

- Instalment 4 = $450

To request this option, please complete the online request form and select ‘Pay over 4 instalments’. To complete this form you will need your ownership number and due date (located on the top right on the front page of your Land Tax Assessment).

Your request will be processed and a confirmation will be provided via email including details of your revised instalment amounts and due dates*.

* If you do not pay the full amount of an instalment by the due date, your total unpaid land tax balance will become payable and interest and penalty tax may apply. If you are unable to make payment before the due date, please contact RevenueSA to make alternative payment arrangements.

Refer to the back of your Land Tax Assessment for payment details.

If you require a longer payment plan, our Debt Management Services Team can assist you. Please complete the online request form and select ‘request a longer payment plan’.

To complete this form you will need your ownership number and due date (located on the top right on the front page of your Land Tax Assessment). You will also need to provide information on how much and how often you can make a payment.

We may ask for additional supporting information and if approved, confirmation will be provided via email including details of your revised payment plan and due dates*. Depending on the terms of the payment plan – some conditions may apply.

* If you do not pay the full amount of an instalment by the due date, your total unpaid land tax balance will become payable and interest and penalty tax may apply. If you are unable to make payment before the due date, please contact RevenueSA to make alternative payment arrangements.

Refer to the back of your Land Tax Assessment for payment details.

Can I make more frequent payments?

You can make more frequent payments (for example: monthly, fortnightly or weekly) using the payment reference. If you choose to make smaller payments, you must ensure the full amount of the instalment is paid by the instalment due date or contact us for an extension*.

For example instead of paying an instalment payment of $1,000 in one payment, you can make smaller payments over a number of weeks, as long as you ensure the $1,000 has been paid by the due date*.

* If you do not pay the full amount of an instalment by the due date, your total unpaid land tax balance will become payable and interest and penalty tax may apply. If you are unable to make payment before the due date, please contact RevenueSA to make alternative payment arrangements.

Refer to the back of your Land Tax Assessment for payment details.

I’m having difficulty paying. What should I do?

Payment by quarterly instalments is provided for land tax. If you wish to organise a payment arrangement, please contact RevenueSA on 8226 3750 (option 2) before the due date on your Land Tax Assessment.