On this page

Definitions of terms used across this website.

A B C D E F G H I J K L M N O P Q R S T U V W X Y Z

A

stamp duty

According to value. The phrase is used in relation to duties levied according to the value of the subject matter.

stamp duty

Occurs when ad valorem duty on one instrument covers the total duty payable on the transaction. Any other document which completes the transaction will not require further duty and will be ‘adjudged duly stamped’.

land tax

When the taxable value of all land owned by the same taxpayer is added together for the calculation of land tax.

first home owner grant

A person applying for a grant who, on completion of the purchase of a home or construction of a new home, will hold a relevant interest in the land on which the home is built.

first home owner grant

A person applying for a grant who, on completion of the purchase of a home or construction of a new home, will hold a relevant interest in the land on which the home is built.

emergency services levy

The rate applicable to an ESL Area Code.

general

To make a calculation or to determine an amount for the purpose of tax.

emergency services levy | land tax

The number allocated to separate assessed pieces of land in South Australia. Also referred to as a valuation number.

stamp duty

To transfer an interest in property.

stamp duty

A document transferring ownership or giving the right to transfer ownership.

stamp duty

Not connected in such a way as to bring into question the ability of one to act independently of the other (relates to parties to a transaction).

emergency services levy | land tax

A unique number given to each piece of land that is assessed separately for land tax and the emergency services levy.

It may also be called a valuation number on your council rates notice or an account number on your SA Water bill.

The images below are for illustrative purposes only.

Emergency services levy

Land tax

stamp duty

The interest in a trust property of the beneficiary of a trust (that is, an equitable interest, by way of contrast with the legal or nominal interest of the trustee). A beneficial interest includes a potential beneficial interest for stamp duty purposes.

land tax | stamp duty

1. A person for whose benefit trust property is held; or

2. A person designated in a will as the recipient of a bequest.

emergency services levy

A person or business to whom the Notice of Emergency Services Levy Assessment is sent, which may differ slightly from the registered proprietor, for example, Certificate of Title may show the owner's maiden name, but the account is sent in the married name. The registered proprietor of the property remains liable for the levy under the Emergency Services Funding Act 1998.

stamp duty

In good faith, honestly (for example, bona fide transaction).

land tax | stamp duty

The business of primary production includes:

- agriculture

- pasturage

- horticulture

- viticulture

- apiculture

- poultry farming

- dairy farming

- forestry or any other business consisting of the cultivation of soils

- the gathering of crops

- the rearing of livestock

- propagation and harvesting of fish or other aquatic organisms.

Additionally land tax purposes, the business of primary production also includes:

- Intensive agistment of declared livestock (being cattle, sheep, pigs or poultry)

emergency services levy

Land carrying out the business of primary production is considered to be land marked as RU (Rural) on a Notice that has been determined by the Valuer-General as land used for primary production.

emergency services levy | stamp duty

The capital value includes the land and all improvements such as buildings, sheds, wells, dams and commercial planting of trees. It is the total value of the land and all things fixed to it and is determined by qualified Valuers from the Office of the Valuer General.

general

A record on the Certificate of Title held at Land Services SA. A caveat prevents any dealing with the land inconsistent with the interest claimed by the person lodging the caveat. The existence of a caveat is noted on the Title but unlike registration of an interest this noting does not in itself confer any interest. The existence of an interest depends on the contract or other dealing involved. In some ways a caveat is a notice of the existence of unregistered interests, if no caveat is noted, another person might infer that no unregistered interests exist.

emergency services levy | land tax | stamp duty

An official recorded issued by Land Services SA of land ownership in South Australia, showing the registered proprietor of the land under the Torrens System. It is equivalent to title deeds under the old system.

stamp duty

A certificate evidencing that a document has either been assessed with stamp duty or is exempt from stamp duty.

The Certificate of Stamp Duty was introduced on 1 July 2019. Prior to this date a document was stamped to evidence that it had been assessed with stamp duty or was exempt from stamp duty.

general

A true copy of an original document that has been sighted and certified by an authorised person* and noted as follows: ‘I certify that I have sighted the original document and this is a true copy of it’. This certification must have the certifier’s name, title, registration number (where applicable) and be signed and dated.

*An authorised person includes a legal practitioner, justice of the peace (JP), registered conveyancer, magistrate, notary public, police officer, bank manager and officers of RevenueSA.

stamp duty

Any kind of personal property as opposed to real property (land). A distinction is drawn between chattels real, that is, interests related to real estate but not classified as real property interests, notably leases, and chattels personal, comprising all other types of personal property.

first home owner grant

Means the relationship between two adult persons (whether or not related by family and irrespective of their gender) who live together as a couple on a genuine domestic basis, but does not include:

- the relationship between a legally married couple; or

- a relationship where one of the persons provides the other with domestic support or personal care (or both) for fee or reward, or on behalf of some other person or an organisation of whatever kind.

Note: Two persons may live together as a couple on a genuine domestic basis whether or not a sexual relationship exits or has ever existed, between them.

first home owner grant

Date of contract to purchase or build a home, or for an owner builder – date the foundations commenced to be laid.

The commencement date of an eligible transaction is:

- in the case of a contract:

- the date when the contract is made;

- in the case of the building of a home by an owner builder:

- the date when laying the foundations for the home commences; or

- another date the Commissioner of State Taxation considers appropriate in the circumstances of the case.

general

Commissioner of State Taxation, RevenueSA.

general

A Community Title is a title over property (generally units) which involves common property (for example, driveway). Each unit has a separate title that is owned by the registered proprietor as recorded on the title.

first home owner grant

When the applicant is entitled to possession of the property under the contract, or the building is ready for occupation as a place of residence and the applicant is registered on the Certificate of Title.

Subject to any qualifications prescribed by legislation, an eligible transaction is completed when:

- in the case of a contract for the purchase of a home:

- the purchaser becomes entitled to possession of the home under the contract; and

- if the purchaser is to obtain a registered title to the land on which the home is situated - the necessary steps to obtain registration of the purchaser's title have been taken;

- in the case of a contract to have a home built the building is ready for occupation as a place of residence;

- in the case of the building of a home by an owner builder - the building is ready for occupation as a place of residence.

first home owner grant | stamp duty

A comprehensive building contract where a builder agrees to build a home, from the time the building starts to when it is finished and is ready for occupation.

stamp duty

An agreement between 2 or more persons which creates an obligation to do, or not to do, a particular thing. A contract creates a legal relationship between the parties to the contract.

general

Related by blood

first home owner grant

Purchase price or cost of construction of the home.

stamp duty

The amount of money paid by the transferee to the transferor for the property.

emergency services levy

Contiguous land are parcels of land which abut (touch) one another or are separated only by certain types of public land where:

- the owner or occupier of all the land concerned is the same;

- all the land is used for the same purpose as defined by the Valuer-General; and

- all the land is contained within the same Emergency Services Area (for example: Regional Area 1).

Pieces of land will be taken to be contiguous if they abut (touch) one another at any point or if they are separated only by:

- a street, road, lane, footway, court, railway, thoroughfare or travelling stock route; or

- a reserve or other similar open space dedicated for public purposes.

Pieces of land will be considered to be separated by intervening land if a line projected at right angles from any point on the boundary of one of them, across the intervening land, would intersect a boundary of the other piece of land.

stamp duty

1. The formal transfer of property; or

2. The instrument by means of which such a transfer is effected.

For a complete list refer to the definition in section 60 of the Stamp Duties Act 1923.

stamp duty

Where the purchaser named in a contract for sale and purchase of land directs the vendor to transfer the land to another party. Refer to Revenue Ruling SDA009 - Conveyance by Direction for further information.

general

Land owned by the State of South Australia.

first home owner grant | stamp duty

Curtilage is a term to define the land immediately surrounding a house or a dwelling, including any closely associated buildings and structures, but excluding any associated 'open fields beyond'.

It defines the boundary within which a home owner can have a reasonable expectation of privacy and where 'intimate home activities' take place.

stamp duty

A person is in a de facto relationship with another person if:

- the persons are not legally married to each other; and

- the persons are not related by family; and

- having regard to all the circumstances of their relationship;

they have a relationship as a couple living together on a genuine domestic basis.

Working out if persons have a relationship as a couple

Those circumstances may include any or all of the following:

- the duration of the relationship;

- the nature and extent of their common residence;

- whether a sexual relationship exists;

- the degree of financial dependence or interdependence, and any arrangements for financial support, between them;

- the ownership, use and acquisition of their property;

- the degree of mutual commitment to a shared life;

- whether the relationship is or was registered under a prescribed law of a State or Territory as a prescribed kind of relationship;

- the care and support of children;

- the reputation and public aspects of the relationship.

stamp duty

A document which has been signed, sealed and delivered, proving or testifying the agreement of the signatories to its contents.

general

Also called a ‘deed of company arrangement’. In corporations law, voluntary administration is a process begun by the appointment of an administrator to a company which is in financial difficulties (but could possibly be saved). During this process, the administrator investigates the company's affairs to recommend to creditors whether it should come under administration according to a Deed of Administration, be wound up, or revert to normal operation by its directors.

stamp duty

The person or group holds a share or unit in a land holding entity

land tax | stamp duty

In a discretionary trust the trustee has the discretion to nominate which beneficiary will benefit from the trust fund and the amount they will receive.

A trust established for the benefit of a family group is usually a discretionary trust.

first home owner grant

A person is the domestic partner of another if they live together in a close personal relationship.

stamp duty

A person is, on a certain date, the domestic partner of another if:

- the person is, on that date, in a registered relationship with the other; or

- the person is, on that date, living with the other in a close personal relationship; and:

- the person:

i) has so lived with the other continuously for the period of 3 years immediately preceding that date; or

ii) has during the period of 4 years immediately preceding that date so lived with the other for periods aggregating not less than 3 years; or - a child, of whom the 2 persons are the parents, has been born (whether or not the child is still living at that date).

- the person:

Close personal relationship means the relationship between 2 adult persons (whether or not related by family and irrespective of their sex or gender identity) who live together as a couple on a genuine domestic basis, but does not include:

- the relationship between a legally married couple; or

- a relationship where one of the persons provides the other with domestic support or personal care (or both) for fee or reward, or on behalf of some other person or an organisation of whatever kind.

Note: Two persons may live together as a couple on a genuine domestic basis whether or not a sexual relationship exists, or has ever existed, between them.

Registered relationship means a relationship that is registered under the Relationships Register Act 2016, and includes a corresponding law registered relationship under that Act.

stamp duty

The value stamp duty is calculated on.

This is generally the greater of the consideration or the market value.

first home owner grant

Contract for the purchase of a new home, contract to build a home or construct a home as an owner builder on or after 1 July 2000.

emergency services levy

South Australia is divided into 4 designated emergency services areas (R1 - R4), each with a specific factor representing differences in emergency service coverage. Each property is assigned to an area based on its location.

Regional area 1 (R1)

Land that is within the cities and towns of Berri, Goolwa, Kadina, Loxton, Mount Barker, Mount Gambier, Murray Bridge, Naracoorte, Nuriootpa, Port Augusta, Port Lincoln, Port Pirie, Renmark, Tanunda, Victor Harbor and Whyalla.

Regional area 2 (R2)

Land that is within the area of a council but is not part of Regional Area 1 or Regional Area 4:

- Adelaide Plains Council

- Barunga West Council

- Ceduna (District Council of)

- Clare and Gilbert Valleys Council

- Cleve (District Council of)

- Coober Pedy (District Council of)

- Coorong District Council

- Elliston (District Council of)

- Flinders Ranges Council (The)

- Franklin Harbour (District Council of)

- Goyder (Regional Council of)

- Grant (District Council of)

- Kangaroo Island Council

- Karoonda East Murray (District Council of)

- Kimba (District Council of)

- Kingston District Council

- Light Regional Council

- Lower Eyre Council

- Mid Murray Council

- Mount Remarkable (District Council of)

- Northern Areas Council

- Orroroo Carrieton (District Council of)

- Peterborough (District Council of)

- Robe (District Council of)

- Roxby Downs (Municipal Council of)

- Southern Mallee District Council

- Streaky Bay (District Council of)

- Tatiara District Council

- Tumby Bay (District Council of)

- Wakefield Regional Council

- Wudinna District Council

- Yorke Peninsula Council

Regional area 3 (R3)

Land within the State that is outside council boundaries and not governed by an incorporated body (known as an unincorporated area). These regions, administered by the State Government and often referred to as outback Australia, cover about 70% of South Australia and include coastal waters, coastline, and extensive arid landscapes.

Regional area 4 (R4)

'Greater Adelaide' being the combined areas of the following metropolitan council areas:

- City of Adelaide

- Adelaide Hills Council

- Alexandrina Council

- The Barossa Council

- City of Burnside

- City of Campbelltown

- City of Charles Sturt

- Town of Gawler

- City of Holdfast Bay

- Corporation of the City of Marion

- Corporation of the City of Mitcham

- District Council of Mount Barker

- City of Norwood, Payneham and St. Peters

- City of Onkaparinga

- City of Playford

- City of Port Adelaide Enfield

- City of Prospect

- City of Salisbury

- City of Tea Tree Gully

- City of Unley

- District Council of Victor Harbor

- Town of Walkerville

- City of West Torrens

- District Council of Yankalilla

stamp duty

A burden or charge, particularly on property.

first home owner grant | stamp duty

An established home is a home that has previously been occupied or sold as a place of residence

general

Payment given as a favour or from a sense of moral obligation rather than because of any legal requirement.

Ex gratia relief from a state revenue obligation may be granted in certain circumstances not covered by the legislation.

first home owner grant | stamp duty

A burden or charge, particularly on property.

general

Released from or not subject to an obligation or liability to which others are subject to (for example, specific taxes).

general

An instrument or circumstance where no tax or duty is payable because of a specific exemption placed in the relevant legislation.

stamp duty

A group of persons connected by an unbroken series of relationships of consanguinity (related by blood) or affinity (related by marriage).

stamp duty

Released from or not subject to an obligation or liability to which others are subject to (for example, specific taxes).

emergency services levy

The fixed charge is the minimum fixed amount payable for each property.

general

In this type of trust, the beneficiaries and their share of the trust are fixed. A fixed trust does not allow other beneficiaries to be added or removed or for the beneficiaries’ share or beneficiaries’ assets in the trust to be changed or reallocated.

A good example of a fixed trust is a trust for two siblings who are each entitled to 50% of the trust fund.

stamp duty

A transfer of an interest less than a full interest.

land tax | stamp duty

This term indicates ownership of land, granting the owner the absolute right to the land and its associated structures.

emergency services levy

The general remission is the portion of the emergency services levy that the State Government contributes on behalf of levy payers.

It is calculated as the difference between the prescribed rates and factors and the effective rates and factors used to calculate the levy.

Unlike other concession, remissions or relief, the general remission is automatically applied to your Notice of Emergency Services Levy Assessment - no application is required.

first home owner grant

The land is to be used for primary production by the applicant(s) seeking the first home owner grant; and the land is, by itself, or in conjunction with other land owned by the applicant(s), capable of supporting economical viable primary production operations.

The relevant component of the genuine farm for the purposes of determining the value for the first home owner grant is the home and curtilage or the part of the land that is to constitute the site and curtilage of the home that is to be built.

first home owner grant

Guardian of a person under a legal disability includes a trustee who holds a property on trust for the person under an instrument of trust or by order or direction of a court or tribunal.

emergency services levy | first home owner grant | land tax | stamp duty

A building affixed to land that may lawfully be used as a place of residence and is, in the Commissioner of State Taxation’s opinion, a suitable building for use as a place of residence.

land tax

A Home Unit Company is a company that is the registered proprietor (as recorded on the title) over a property containing units or flats where individuals purchase a share in the company. This share in the company gives the individual shareholder an exclusive right to occupy a particular unit/flat by way of a lease.

stamp duty

In kind; in its own form.

A phrase describing the distribution of an asset in its present form, rather than selling it and distributing the cash. In specie distribution is made when cash is not readily available, or allocating the physical asset is the better alternative.

stamp duty

A person or group has an indirect interest in a private company or private unit trust scheme (entity B) if the person or group has a direct interest in a private company or private unit trust scheme (entity A) which is a related entity to entity B

stamp duty

A formal legal document creating or recording some legal right of liability.

general

Amongst or between living persons.

general

The situation arising upon the death of a person who has not left a valid will, or who has failed to dispose entirely of his/her assets (partial intestacy).

general

To die without having left a valid will or having left a will which does not dispose entirely of the deceased’s assets.

general

Upon the death of a joint tenant that person’s interest in the property passes to the other joint tenants. For example, A, B & C on the title. C dies so their 1/3 interest passes to A & B who now hold a 50/50 interest.

Joint tenants always hold interests equally (often husband and wife owned property).

stamp duty

An entity that holds local land assets.

general

Land Services SA manages the Property Title Registry and Valuation Roll on behalf of the South Australian Government.

Previously Lands Title Office.

emergency services levy

Land use factors

The factor applied to the relevant land use category for the emergency services levy.

It is used to ensure that land with a greater chance of needing for an emergency service contributes more to the emergency services fund than land that doesn’t have the same risk attached to it (for example: land used for industrial purposes has a far greater risk attached to it than vacant land does).

Land use categories

The following land use categories apply for the emergency services levy:

- Residential (RE)

- Commercial (CO)

- Industrial (IN)

- Rural (primary production land) (RU)

- Vacant land (VA)

- Special community use (CU)

- Other (OT)

Special community use includes land used for the following purposes:

- Aboriginal community

- Boy scouts

- Cemeteries

- Charitable organisations

- Churches

- Community hospital

- Convalescent and rest homes

- Girl guides

- Health centre

- Hospital

- Institutional residential

- Institutional residential accommodation NEC

- MBHA Clinics

- Medical and health

- Mental hospital

- Nursing homes

- Old folk's homes

- Orphan's accommodation

- Places of assembly

- Private hospital

- Public conveniences and public utilities NEC

- Public halls

- Religious quarters - monasteries

- Retired and aged accommodation

- Sanatoria

- Seminaries

- Social services and welfare provision

- Social welfare

- Social welfare NEC

- YMCA and YWCA facilities

- Youth centres

NEC means 'not elsewhere classified'.

general

All properties in South Australia are assigned a land use code (LUC) by the Valuer-General, based on the predominant use of the land.

There are 10 primary codes:

- Commercial

- Industrial

- Institutions

- Open

- Primary production

- Public utilities

- Quarrying and mining

- Recreation

- Residential

- Vacant land

emergency services levy

The rate applicable to a Land Use Category.

general

The 'laws of intestacy' are set out in the Succession Act 2023. This Act states that if a person dies intestate, then the property should be distributed in the manner set out in that Act.

stamp duty

An agreement by which the owner of a property allows another to use it for a specified time, in return for payment.

general

The person to whom a lease is granted (the tenant).

general

The person who grants a lease (the landlord) to another person.

stamp duty

Letter whereby a purchaser appoints another party to enter into and execute a contract on their behalf (that is, act as their agent).

emergency services levy

Levy (fee) payable on an individual property or parcel of land.

emergency services levy

Account issued to property owners for payment of the emergency services levy.

emergency services levy

The rate set each year for the purposes of calculating the emergency service levy.

general

A freehold interest or estate subsisting as long as the grantee, or some other person, might live.

general

A freehold interest or estate subsisting as long as the grantee, or some other person, might live.

general

A person who is registered on the certificate of title as having a life interest in the property. This includes properties which are registered in the name of a trustee, but which are subject to a life interest.

stamp duty

Is a non-qualifying land asset consisting of an interest in land in South Australia.

stamp duty

The party who submits documentation for an assessment for themselves or on behalf of their client.

first home owner grant

In the case of a contract for the purchase of a home, the market value is the greater of:

- the consideration for the eligible transaction; or

- the market value of the property on which the home is situated, as at the commencement date of the eligible transaction.

In the case of a contract to build, the market value is calculated by adding together:

- the consideration for the comprehensive home building contract, or if the Commissioner of State Taxation considers that the total consideration payable for the building work may be less than the actual costs to build the home; and

- the market value of the property on which the home is to be built, as at the time when the building contract is made*.

* if land is purchased within 12 months of the building contract being executed and is in relation to an arms length transaction, the consideration paid for the land may be used as the market value.

In the case of an owner builder, the market value is taken to be the market value of the property on which the home is situated at the time when the eligible transaction is completed (this generally means when the building is ready for occupation as a place of residence).

Stamp duty

The price which a willing but not anxious vendor could reasonably expect to obtain and a hypothetical willing but not anxious purchaser could reasonably expect to have to pay.

general

Where more than one registered proprietor owns an undivided portion of the whole property.

Example: 2 maisonettes are held through 2 moiety titles, each relating to 50% of the whole property. The registered proprietor of each title has a 50% interest in both maisonettes, however documents registered on the titles provide for exclusive rights of occupation for each maisonette.

land tax

Refers to the actual land tax applied to a parcel of land.

Where the owner owns 2 or more taxable parcels of land, this amount takes into account other taxable properties in the ownership, tax is calculated on the total of the site values of the taxable land and apportioned back to the individual parcel of land (multiple holding).

Where the owner only owns one taxable parcel of land, the tax is calculated on the site value of that property, however, it is still referred to multiple holding (in this circumstance, single holding is the same as multiple holding).

first home owner grant | foreign ownership surcharge | land tax

A natural person (does not include a company or trust).

first home owner grant | stamp duty

A new home is a home that has been built but has not been previously occupied or sold as a place of residence. This includes houses, flats, units, duplexes, townhouses, apartments and substantially renovated homes.

For a substantially renovated home to be eligible, it must be purchased from a developer, who has undertaken substantial renovations, not just purely cosmetic changes. The developer must be registered for GST purposes for developing the property and claimed GST offsets on the renovations to the home and provide evidence of this. See ATO Goods and Services Tax Ruling (GSTR 2003/3) for more information.

stamp duty

Land that is predominately used for residential purposes or for primary production.

first home owner grant

When any part of the eligibility criteria is not met, the applicant(s) must notify the Commissioner of State Taxation within 14 days of the event.

An example would be where an applicant is not able to occupy the home as their principal place of residence within 12 months of completion of the eligible transaction.

general

A notional value is a concessional property valuation available to primary producers and others under certain circumstances. Notional values are aimed at encouraging the retention of primary production uses on land where there is pressure to alter the use away from primary production.

first home owner grant | stamp duty

An off the plan apartment is an apartment that has not yet been built and exists as a plan that is yet to be constructed or for which construction has commenced and where the work has not been substantially completed.

first home owner grant | stamp duty

A person who has a relevant interest in land on which a home is built.

first home owner grant | stamp duty

An owner of land who builds a home, or has a home built, on the land without entering into a comprehensive building contract.

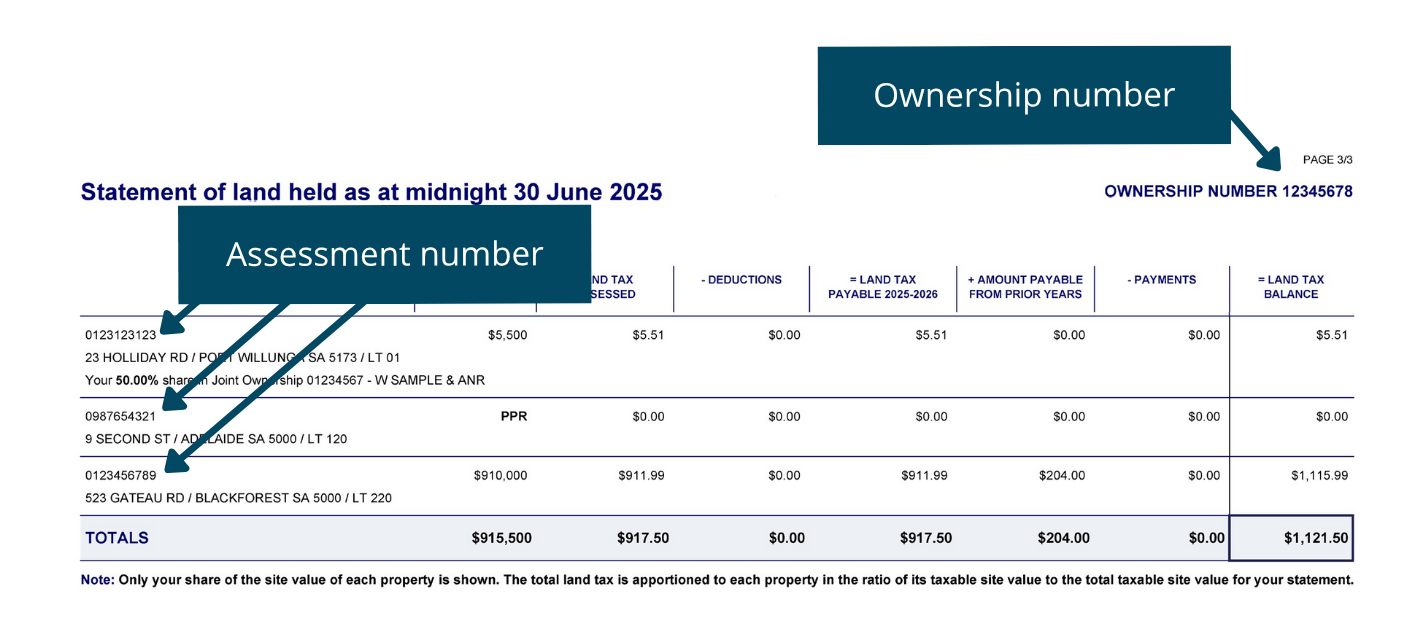

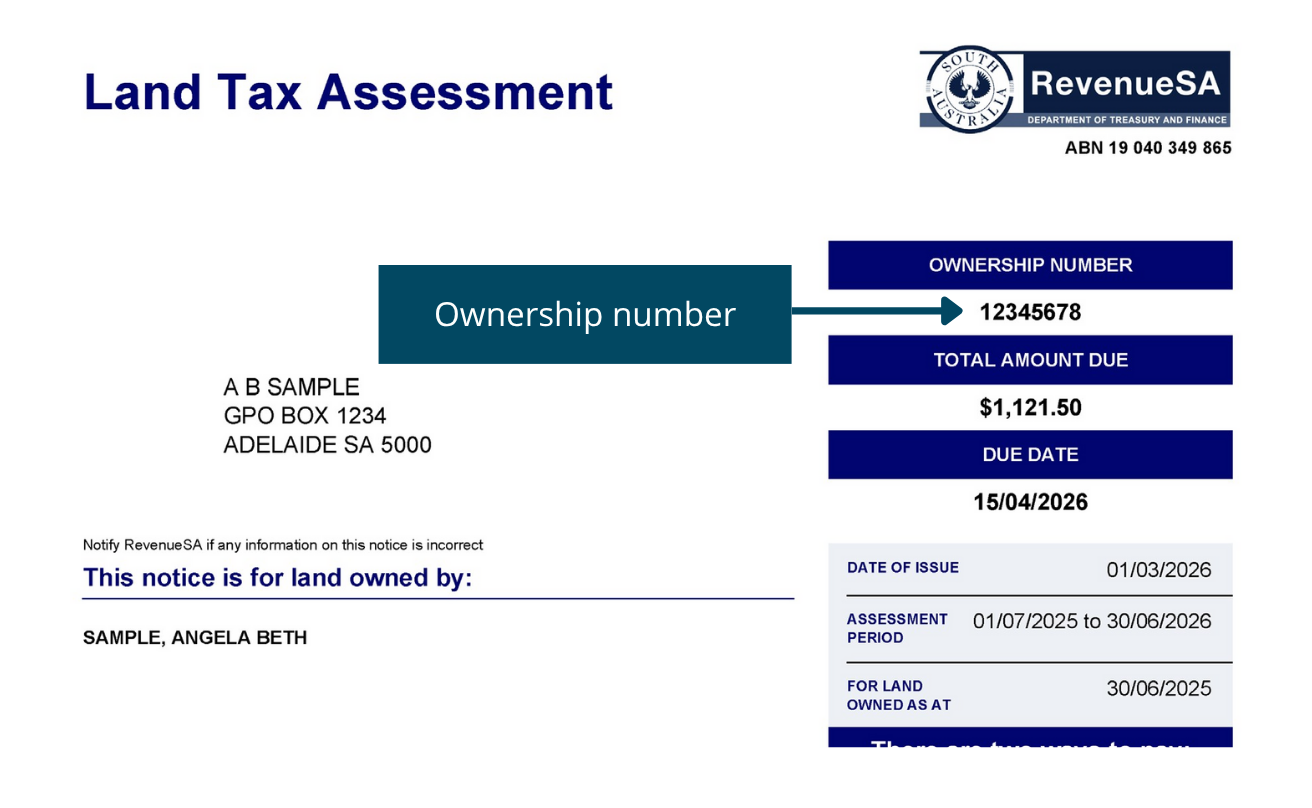

emergency services levy | land tax

An ownership number is a unique number assigned to land owners or joint owners. This number can be used for queries, applications and correspondence, and helps RevenueSA identify who you are and what land you own.

The ownership number is shown in the top right corner of your Notice of Emergency Services Levy Assessment and Land Tax Assessment.

The images below are for illustrative purposes only.

Emergency services levy

Land tax

stamp duty

The division of land among joint tenants or tenants in common so that each becomes sole owner of a part of the land.

first home owner grant | foreign ownership surcharge | stamp duty

A person who holds a permanent residency visa under section 30 of the Migration Act 1958 (Cwlth) or a New Zealand citizen who is the holder of a special category visa under section 32 of the Migration Act 1958 (Cwlth).

stamp duty

The rights, expectancies or possibilities of an object of a discretionary trust in, or in relation to, property subject to the discretionary trust. Object is a person on whom the trustee can vest any trust property.

stamp duty

In relation to a private company or private unit trust scheme – a proportionate interest in the entity of 50% or more; and in relation to a listed company or a public unit trust scheme – a proportionate interest of 90% or more.

emergency services levy

Land carrying out the business of primary production is considered to be land marked as RU (Rural) on a Notice that has been determined by the Valuer-General as land used for primary production.

land tax | stamp duty

The business of primary production includes:

- agriculture

- pasturage

- horticulture

- viticulture

- apiculture

- poultry farming

- dairy farming

- forestry or any other business consisting of the cultivation of soils

- the gathering of crops

- the rearing of livestock

- propagation and harvesting of fish or other aquatic organisms.

Additionally land tax purposes, the business of primary production also includes:

- Intensive agistment of declared livestock (being cattle, sheep, pigs or poultry)

general | emergency services levy | first home owner grant | land tax |stamp duty

Your principal place of residence is the home where you primarily live on an ongoing basis.

It must meet all of the following conditions:

- Natural person - The home must be owned by a natural person.

- Primary residence - It is the main place where the owner (or owners) lives.

- Usual living activities - It is where you routinely undertake normal domestic activities such as cooking, eating, sleeping, and keeping your personal belongings.

- Occupied continuously - Occupation is on a permanent and ongoing basis, not temporarily or merely with an intention to occupy in the future.

- Residential design - The building is a permanent, fixed structure designed and constructed primarily for residential purposes.

general

A document issued by the court certifying that a Will has been proved as valid, and authorising the executor to administer the estate.

emergency services levy | land tax

Report that provides information on encumbrances, charges, liens, acts etc. over a particular property.

Issued under Section 7, Land and Business (Sale and Conveyancing) Act 1994.

stamp duty

A proportionate interest in a relevant entity (a private company, private unit trust scheme, listed company or a public unit trust scheme) means:

- for a person or group that has a direct interest or an indirect interest in the entity – the percentage representing the extent of that interest; or

- for a person or group that has both a direct interest and an indirect interest in the entity – an aggregate percentage representing the extent of both those interests.

general

Person or entity purchasing a property.

stamp duty

Qualifying land means land that is being used other than for residential purposes or for primary production as defined the Stamp Duties Act 1923.

The Commissioner will generally rely on land use codes to determine whether he considers land to be residential or primary production land. The land use codes within the following Land Use Code (LUC) headings will be taken to be qualifying land:

- Commercial (LUC 2000-2999)

- Industrial (LUC 3100-3999)

- Vacant Land* (with some exceptions) (LUC 4110-4600)

- Institutions (LUC 5100-5990)

- Public Utilities (LUC 6100-6990)

- Recreation (LUC 7100-7900)

- Mining and Quarrying (LUC 8100-8409)

The following residential Land Use Codes will also be taken to be qualifying land:

- Hotel (LUC 1810);

- Motel (LUC 1820); and

- Hotel/Motel Community (LUC 1831).

*unless the land is within a zone established by a Development Plan under the Planning, Development and Infrastructure Act 2016 that envisages the use, or potential use, of the land as non-residential and non-primary production.

Stamp duty on transfers of residential and primary production land will remain unchanged. Vacant land will be considered to be used for primary production or residential purposes in certain circumstances. The conveying document must be submitted to the Commissioner advising the LUC, the actual use of the land as at the date of the conveyance and any other details to evidence whether the land should be regarded as Qualifying Land.

stamp duty

Land property.

general

Means the Australian Stock Exchange Limited or a stock exchange classified by regulation as a recognised stock exchange.

emergency services levy | land tax

Your reference number (also called a payment reference number) is a unique 10-digit identifier that applies to a specific payment transaction.

You must provide your reference number every time you make a payment with BPAY. This ensures your money is assigned to the correct payment.

Important:

- RevenueSA uses more than one biller code to ensure that payments for different transactions are allocated correctly - for example, emergency services levy assessments, land tax assessments, certificates of land tax payable and certificates of emergency services levy payable.

- Your reference number can change - always ensure you check both the payment reference number and biller code before making a payment.

first home owner grant

A person is related to or associated with another party when:

- one is the spouse/domestic partner of the other;

- they are related by blood, marriage or adoption;

- they are a shareholder or director of the other party, being a company;

- they are a beneficiary of a trust for which the other party is a trustee; or

- the transaction is otherwise not at arm's length.

stamp duty

Includes persons who are connected by blood or marriage and also includes “related persons” as defined in Section 60A(6) of the Stamp Duties Act 1923, which includes:

- natural persons who are either members of a partnership or who are related as spouses or as a parent and a child;

- related companies for Corporations Act 2001 purposes;

- trustees who have a common beneficiary in relation to their individual trusts;

- natural person and a company, where the natural person is a major shareholder, director, secretary of the company or in another related company;

- natural person beneficiary and the trustee of the trust; or a

- company and a trustee under certain circumstances (refer Section 60A(6)(f) of the Stamp Duties Act 1923).

first home owner grant | stamp duty

A person with a relevant interest may be described as someone who will have a legal entitlement to occupy the home being bought or constructed. Usually this will be the person(s) registered as proprietor on the Title. This commonly is an estate in fee simple. Other forms of interest are defined in the First Home and Housing Construction Grants Act 2000.

Each person acquiring a relevant interest must be an applicant on the First Home Owner Grant Application form.

stamp duty

An interest in land, vesting in possession on the determination of a prior particular estate in the same land: to A for life, remainder to B in fee simple. A contingent remainder is for a future interest which will only arise (that is, vest in interest) on the happening of some contingency, and if it does not arise, will vest in possession on the determination of the prior particular estate: to A for life with remainder to B in fee simple if B attains the age of 21.

stamp duty

A person entitled to a remainder interest.

emergency services levy

Rebate applied in respect to the emergency services levy

general

Payment to the lessor by the lessee for the right to exclusive possession of premises for a period.

first home owner grant | stamp duty

The home you primarily reside in. This home must be occupied by each applicant for a continuous period of at least 6 months, commencing within 12 months of the completion of the eligible transaction.

first home owner grant | stamp duty

The following are examples of the main property types which should be classified as ‘residential’. These classifications apply irrespective of whether the property being conveyed is established or newly constructed, and irrespective of whether it is purchased for owner occupation, investment (rental) or business use.

- houses;

- flats;

- units;

- apartments;

- holiday homes;

- vacant land zoned as residential use (if known);

- permanent houseboat moorings;

- permanent caravan park sites; or

- farms and other primary production land - only if predominantly for residential use.

There will be instances where a conveyance of real property has mixed uses – for example, a shop with a house/flat attached. In such instances the predominant use of the property should determine whether it is classified as residential or non-residential. Indicators of the predominant use may include which potential uses are most active currently, the respective floor area of the actual uses (if able to be determined) or the separate valuation of each of the respective uses.

first home owner grant | stamp duty

Land in Australia on which there is a home which can be lawfully occupied and is suitable for occupation as a place of residence. This includes houses, townhouses, units, flats, duplexes, converted warehouses and fixed movable homes.

first home owner grant | emergency services levy | land tax | stamp duty

The date on which the purchaser pays for the property and the vendor hands over a signed transfer document to the purchaser for registration at Land Services SA.

emergency services levy

A single farming enterprise consists of properties where:

- the owner or occupier of all the land concerned is the same;

- all of the land is used to carry on the business of primary production* and is managed as a single unit for that purpose; and

- all of the land is contained in the same or adjoining council area.

* Land marked as RU (Rural) on a Notice has been determined by the Valuer-General as land used for primary production.

The land may be adjoining (contiguous) or separated by other land.

land tax

Single holding amount is a calculation based on the site value of a property using the rates of land tax assuming that the property is the only taxable property in the ownership. This figure is used to adjust land tax against the property at time of sale by land brokers, agents and conveyancers.

land tax

The site value is the value of a piece of land excluding any value added by buildings or other improvements. It is the value of just the land, as if it were vacant. It is determined by qualified Valuers from the Office of the Valuer General.

first home owner grant | stamp duty

A person is the spouse of another if they are legally married.

general

A written statement which the declarant claims to be true and signs before an authorised person for legal purposes.

general

A Strata Title is a title over property (generally units) which involves common property (for example, driveway). Each unit has a separate title that is owned by the registered proprietor as recorded on the title.

first home owner grant | stamp duty

A home is a substantially renovated home if:

- the sale of the home is, under the A New Tax System (Goods and Services Tax) Act 1999 (Cwlth), a taxable supply as a sale of new residential premises within the meaning of Section 40-75(1)(b) (Meaning of new residential premises); and

- the home, as renovated, has not been previously occupied or sold as a place of residence.

stamp duty

The surrenderor is the registered lessee that gives up their rights to a Crown Lease, in effect, they surrender the Crown Lease.

general

A person or business entity which rents land or property from a landlord.

general

If property is owned by tenants in common, on the death of one of the tenants in common, the deceased person’s fractional share is distributed according to their will. If there is no will, the fractional share is distributed according to the rules that apply upon intestacy. For example, A B & C on the title. A dies and wills his interest to X, so the owners are now B, C and X.

A tenant in common can hold an uneven interest share, for example, A as to 50%, B as to 30% and C as to 20%.

general

The holding or possession of property.

general

A legal right to the possession of property, especially real property.

general

A search on the land which shows the names of the registered owners. A title search can be obtained from Land Services SA.

stamp duty

Also referred to as a ‘conveyance’

- The formal transfer of property; or

- The instrument by means of which such a transfer is effected.

For a complete list refer to the definition in Section 60 of the Stamp Duties Act 1923.

general

Person or entity from which property is transferred or conveyed (property transfers from the transferor to the transferee).

general

Person or entity who makes a transfer or conveyance of property (property transfers from the transferor to the transferee).

general

An arrangement for the holding and management of property by one party for the benefit of another, or for specific purposes.

general

An instrument creating and setting out the terms of a trust.

general

One who holds property for another under trust.

general

One authorised to act as trustee of a bankrupt’s estate.

first home owner grant

A numerical code that is assigned by FHOG Online to a first home owner grant application.

general

The measure of the interest held by a subscriber to a unit trust in the total trust fund.

general

A unit trust allows a beneficiary to receive part of any profit or income that comes through the purchase, holding, maintaining or disposal of property held in the trust. Beneficiaries of this type of trust are generally called unitholders. They are entitled to profits, income or other trust funds in proportion to their unitholding.

stamp duty

Pursuant to section 71 of the Stamp Duties Act 1923, the value of the property conveyed by any conveyance operating as a voluntary disposition must be declared in the conveyance. This is the value of the property being conveyed.

general

Person selling a property.