On this page

This page provides information about how much stamp duty relief you may be eligible for.

Stamp duty relief available

You will not be eligible for stamp duty relief if you, another applicant, or your spouse or domestic partner have already received it (or any equivalent) in any state or territory of Australia. However, if relief was received and later paid back (including any penalties that may have been applied), you may be entitled to reapply for stamp duty relief.

The amount of stamp duty relief available, including whether this is applied to the foreign ownership surcharge (if applicable to the transaction), and eligibility requirements depends on the date you entered or enter into a contract to purchase any of the following:

- a new home

- an off-the-plan apartment

- vacant land to build your home on (including for owner builders and contracts to build or comprehensive building contracts)

In addition, when one or more of the applicants are not an Australian citizen or permanent resident of Australia, a foreign ownership surcharge may also be payable. Depending on the date of your contract, full, partial or no relief may be applied.

Contract periods

If you entered into your contract on or after 13 February 2025:

- Full stamp duty relief is available, regardless of the property value.

- Stamp duty relief is not applied to the foreign ownership surcharge. This means you will have to pay the surcharge, if applicable.

If you entered into your contract between 6 June 2024 and 12 February 2025:

- Full stamp duty relief is available, regardless of the property value.

- Full or partial stamp duty relief may also apply to the foreign ownership surcharge, if applicable.

If you entered into your contract between 15 June 2023 and 5 June 2024:

- Full or partial stamp duty relief is available, depending on the property value.

- Full or partial stamp duty relief may also be applied to the foreign ownership surcharge, if applicable.

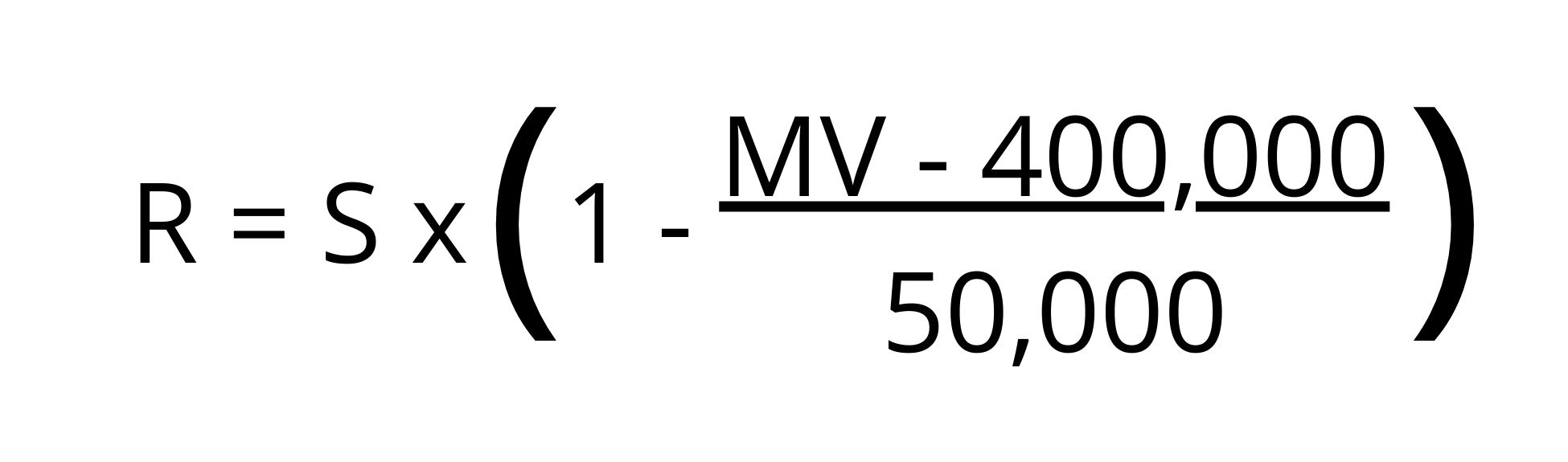

Calculation of partial stamp duty relief for new homes

Stamp duty relief for eligible first home buyers is calculated on the stamp duty that would apply and the foreign ownership surcharge (if applicable).

For new homes or an off-the-plan apartment:

- Full stamp duty relief applies if the dutiable value is $650,000 or less

- Partial stamp duty relief applies if the dutiable value is above $650,000 but less than $700,000

- No stamp duty relief applies if the dutiable value is $700,000 or more.

Calculate stamp duty using the stamp duty calculator.

Partial stamp duty relief

Partial stamp duty relief will be calculated as follows for new homes:

Where :

- R is the amount of reduction in stamp duty

- S is the total of stamp duty (the dutiable value) and foreign ownership surcharge that would apply if relief was not provided

- MV is the market value of the vacant land

Dutiable value

In the case of a contract to purchase a new home or an off-the-plan apartment, the dutiable value is the greater of either of the following:

- consideration for the purchase price

- market value of the property.

In most cases, the dutiable value of a property is the contract price you pay for it. However, if the price you pay for the property is less than market value, the dutiable value will be the market value.

RevenueSA may adopt or approve any reasonable method to determine the market value, including a valuation by a person appointed or approved by RevenueSA. In such cases, RevenueSA may charge the applicant for all or part of the valuation expenses, which can be recovered as a debt owed to the Crown.

RevenueSA will refer a valuation matter to the Valuer-General where necessary.

Stamp duty relief available for new homes

| Property Value | Stamp Duty Usually Applied | Stamp Duty Relief | Amount Payable |

|---|---|---|---|

| Less than $650,000 | Varies according to dutiable value | full relief | $0 |

| $650,000 | $29,580 | full relief | $0 |

| $660,000 | $30,130 | $24,104 | $6,026 |

| $670,000 | $30,680 | $18,408 | $12,272 |

| $680,000 | $31,230 | $12,492 | $18,738 |

| $690,000 | $31,780 | $6,356 | $25,424 |

| $700,000 or more | $32,330 | No relief | $32,330 |

Example

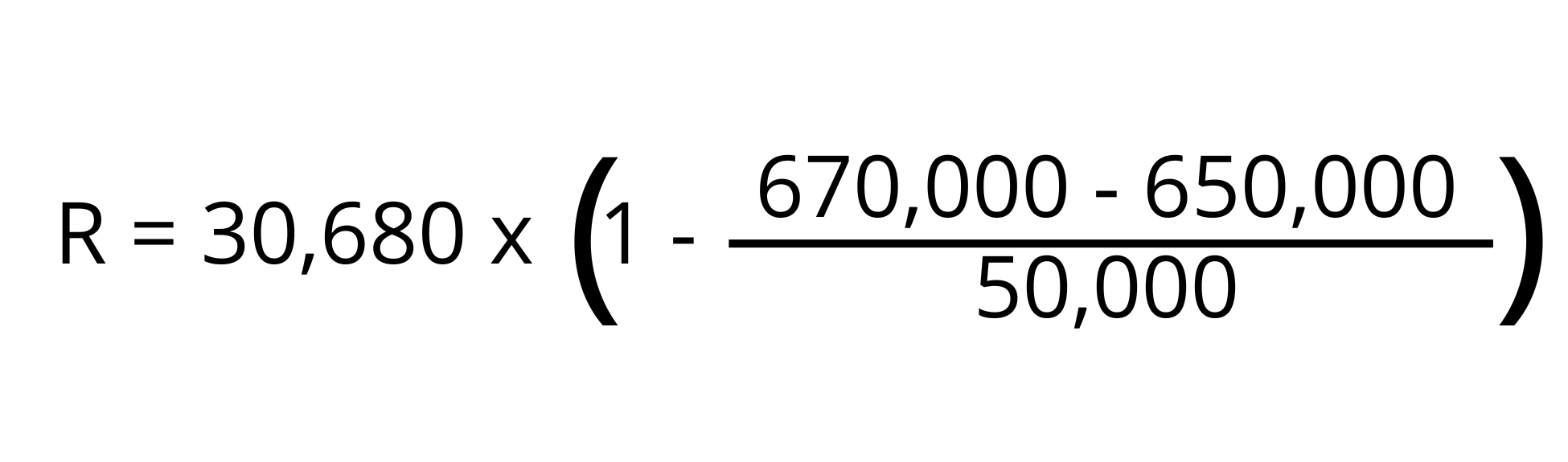

Peter and Mary enter into a contract to purchase a new home on 28 August 2023.

The home has not been previously occupied or sold as a place of residence. The purchase price is $670,000, and they will each have a 50% interest in the home.

The stamp duty payable on a $670,000 property is $30,680.

As the dutiable value of the property is between $650,000 and the $700,000 cap, partial stamp duty relief will apply if all eligibility criteria are satisfied.

| Stamp duty applied on property value of $670,000 | $30,680 |

| Stamp duty relief | - $18,408 |

| Total stamp duty payable | = $12,272 |

Stamp duty relief is calculated as follows:

= 30,680 x (1 - 0.4)

= 30,680 x 0.6

= $18,408 stamp duty relief

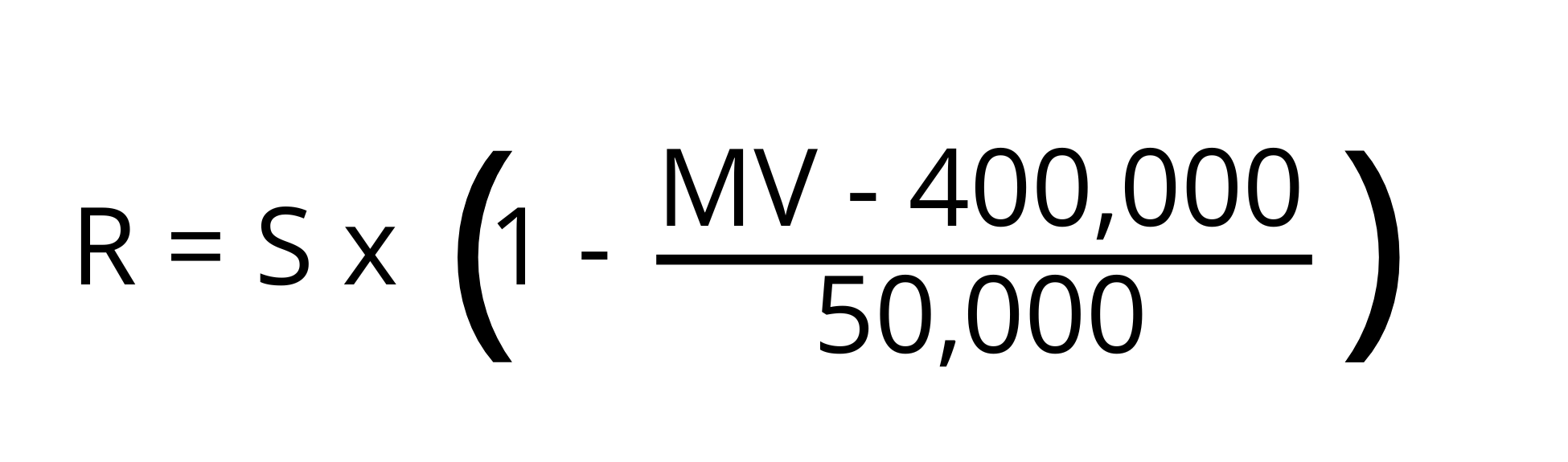

Calculation of stamp duty relief for vacant land

Stamp duty relief for eligible first home buyers is calculated on the stamp duty that would apply and the foreign ownership surcharge (if applicable).

For vacant land and house and land packages:

- Full stamp duty relief applies if the dutiable value is $400,000 or less

- Partial stamp duty relief applies if the dutiable value is above $400,000 but less than $450,000

- No stamp duty relief applies if the dutiable value is $450,000 or more.

Calculate stamp duty using the stamp duty calculator.

Partial stamp duty relief

Partial stamp duty relief will be calculated as follows for vacant land:

Where :

- R is the amount of reduction in stamp duty

- S is the total of stamp duty and foreign ownership surcharge that would apply if relief was not provided

- MV is the market value of the vacant land

Dutiable value

In the case of vacant land, the dutiable value is the greater of either of the following:

- consideration for the purchase price

- market value of the property.

In the case of a house and land package (comprehensive building contract), the dutiable value is:

- the market value of the property on which the home is to be built as at the date of transfer.

In most cases, the dutiable value of a property is the contract price you pay for it. However, if the price you pay for the property is less than market value, the dutiable value will be the market value.

RevenueSA may adopt or approve any reasonable method to determine the market value, including a valuation by a person appointed or approved by RevenueSA. In such cases, RevenueSA may charge the applicant for all or part of the valuation expenses, which can be recovered as a debt owed to the Crown.

RevenueSA will refer a valuation matter to the Valuer-General where necessary.

Stamp duty relief available for vacant land

| Property Value | Stamp Duty Usually Applied | Stamp Duty Relief | Amount Payable |

|---|---|---|---|

| Less than $400,000 | Varies according to the dutiable value | full relief | $0 |

| $400,000 | $16,330 | full relief | $0 |

| $410,000 | $16,830 | $13,464 | $3,366 |

| $420,000 | $17,330 | $10,398 | $6,932 |

| $430,000 | $17,830 | $7,132 | $10,698 |

| $440,000 | $18,330 | $3,666 | $14,664 |

| $450,000 or more | $18,330 | No relief | $18,330 |

Example

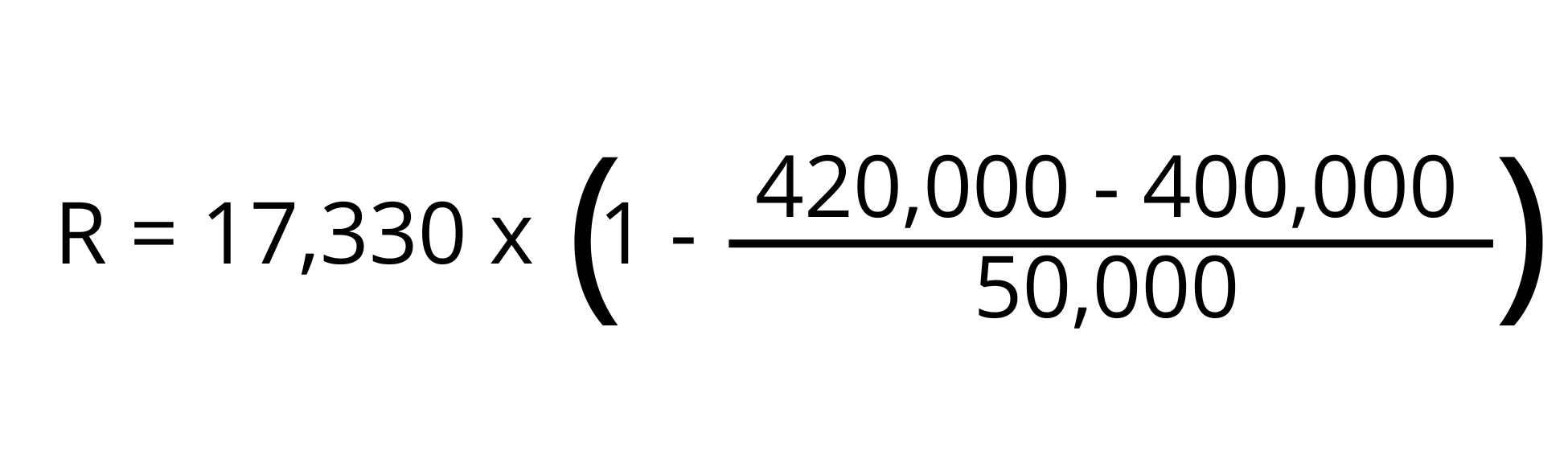

Allan enters into a contract on 05 January 2024 to purchase vacant land. He intends to build his principal place of residence on the land.

The purchase price is $420,000.

The stamp duty payable on $420,000 is $17,330.

As the dutiable value of the property is between $400,000 and the $450,000 cap, partial stamp duty relief will apply if all eligibility criteria are satisfied.

| Stamp duty applied on property value of $420,000 | $17,330 |

| Stamp duty relief | - $10,398 |

| Stamp duty payable | = $6,932 |

Stamp duty relief is calculated as follows:

= 17,330 x (1 - 0.4)

= 17,330 x 0.6

= $10,398 stamp duty relief

If you entered into your contract before 15 June 2023:

- No stamp duty relief (including for the foreign ownership surcharge) applies to any contracts entered into before 15 June 2023.

Foreign ownership surcharge

A foreign ownership surcharge will apply when one or more of the applicants are not an Australian citizen or permanent resident of Australia. The foreign ownership surcharge is applied at 7% on the interest the foreign person ![]() has in the residential land or home.

has in the residential land or home.

Eligible first home buyers may receive full or partial relief on the amount of the foreign ownership surcharge payable, depending on when you enter or entered into your contract.

No stamp duty relief will apply to any foreign ownership surcharge payable for contracts entered into on or after 13 February 2025.

If you entered into your contract between 15 June 2023 and 12 February 2025:

- Full or partial stamp duty relief may apply to any foreign ownership surcharge payable.

New homes, off-the-plan homes and substantially renovated homes

- Full relief applies to homes with a dutiable value of $650,000 or less.

- Partial relief applies to homes with a dutiable value above $650,000 but below $700,000.

- No relief applies to homes with a dutiable value of $700,000 or more.

Calculations for new homes

Stamp duty relief is calculated as:

Where :

- R is the amount of reduction in stamp duty

- S is the total of stamp duty and foreign ownership surcharge that would apply if relief was not provided

- MV is the market value of the new home (including the land on which the home is situated)

Example

Suzie and Colin enter into a contract to purchase a new home on 25 September 2023.

The home has not been previously occupied or sold as a place of residence. The purchase price is $690,000, and they will each have a 50% interest in the home.

The dutiable value of the property exceeds $650,000, but not the $700,000 cap, so Suzie and Colin will receive partial stamp duty relief.

Suzie is an Australian citizen, but Colin is not. The foreign ownership surcharge of 7% will be applied to Colin's 50% interest in the land; in other words, it will apply to $345,000.

Provided that all other criteria are satisfied, Suzy and Colin will receive a reduction in the stamp duty payable of $44,744. This is calculated as follows:

| Stamp duty payable on $690,000 dutiable value | $31,780 |

| Foreign ownership surcharge (applied to Colin's 50% interest in the home) | + $24,150 |

| Total duty that would be payable before relief is applied | = $55,930 |

| Stamp duty relief | - $11,186 |

| Total stamp duty and foreign ownership surcharge payable | = $44,744 |

Vacant land:

- Full relief applies to applies to vacant land with a dutiable value of $400,000 or less, including house and land packages where the land value is $400,000 or less.

- Partial relief applies to vacant land with a dutiable value above $400,000 but below $450,000, including house and land package where the land value is above $400,000 but below $450,000.

- No relief applies for vacant land, including house and land packages, where the land value is $450,000 or more.

Calculations for vacant land

Stamp duty relief is calculated as:

Where :

- R is the amount of reduction in stamp duty

- S is the total of stamp duty and foreign ownership surcharge that would apply if relief was not provided

- MV is the market value of the new home (including the land on which the home is situated)

Cancelling and re-signing contracts

If you entered into a contract to purchase a new home, an off-the-plan apartment, vacant land or a house and land package and subsequently have had to cancel that contract, you may still be eligible for stamp duty relief.

However, if the contracts are for the purchase of the same new home or vacant land, RevenueSA may not accept the new contract if the eligibility criteria changed between the date of the original contract and the new contract, meaning you may not be eligible for stamp duty relief.

You will need to provide RevenueSA a copy of the original contract and the new contract along with an explanation of why your contract was cancelled. You may be asked to provide further documentation in order for your eligibility to be assessed.

Refund of stamp duty for eligible first home buyers

If you have already purchased a new home or vacant land and settlement has been finalised and you meet all applicable eligibility criteria, you can apply online for a refund of the stamp duty you paid.

You will need to complete the Application for refund of stamp duty form and upload the following in support of your application:

- Application for Stamp Duty Relief for Eligible First Home Buyers (PDF 406KB) including any required supporting documentation

In addition, you will also need to provide:

- Details of the transaction (the document ID, and duty paid, and interest and penalty tax paid if applicable)

- a SAILIS valuation relevant to the date of transfer

- bank details for where you want your refund to be paid

Applications for a refund of stamp duty must be made within 5 years from the date of settlement.

Contact Us

When contacting us please provide your property information (such as address, ownership number, site details, etc) and conveyancer information, where applicable.

| stamps@sa.gov.au | |

| phone | (08) 8372 7534 |

| fax | (08) 8226 3737 |

| post |

RevenueSA Kaurna Country GPO Box 1353 ADELAIDE SA 5001 |

| DX | DX 179 |

You can reach us during business hours, excluding public holidays:

- Monday, Tuesday, Thursday, Friday: 8:30am - 5:00pm (ACST or ACDT)

- Wednesday: 10:00am - 5:00pm (ACST or ACDT)

South Australia observes daylight saving.

- ACST: Australian Central Standard Time is from early April to early October.

- ACDT: Australian Central Daylight Time is from early October to early April.

Do you want to provide feedback or lodge a complaint?

You can do so via our feedback and complaints page.