On this page

This page gives information about how land tax is assessed.

Assessment of land tax

Land tax is calculated based on the total taxable site value ![]() of the land you own as at midnight on 30 June each year.

of the land you own as at midnight on 30 June each year.

- Where more than one property is owned, all taxable site values are combined (aggregated) to give the total taxable site value for the ownership.

- If the total taxable site value is over the land tax threshold, land tax is applied at either the general tax rates or the trust tax rates.

- Each taxable property in the ownership is apportioned its share of land tax based on its site value. Exempt land is not included in the assessment calculation and will not have any land tax apportioned to it.

Determine the site value

- Each year, the Valuer-General determines site values and capital values for all rateable properties across South Australia.

- If you disagree with a site value that is in force (meaning the site value for the current financial year), you can lodge an objection with the Valuer-General. Objections must be lodged within 60 days of receiving the first notice of assessment.

Find out more about lodging an objection.

Aggregate property site values and apportion land tax

- When there is more than one taxable property in an ownership, the site values will be added together (aggregated) to determine the total taxable site value.

- Land tax is calculated and distributed proportionally to each taxable property based on its site value. Land that is exempt from land tax will not have any land tax apportioned to it.

Find out more about land tax exemptions.

Example - David's land tax assessment

David is the sole owner of 3 properties:

- Property A is his principal place of residence and is exempt from land tax.

- Property B and C are taxable.

These properties are not held on trust.

Total taxable site value

David's total taxable site value is determined by adding all of the taxable site values together:

| Property | Site Value |

|---|---|

| A | Exempt |

| B | $740,000 |

| C | $835,000 |

| Total taxable site value | $1,575,000 |

Calculating land tax

David's total taxable site value is over the general land tax threshold.

David's properties are assessed using the general tax rates.

Using the 2026-27 general land tax calculator, the land tax payable for a total taxable site value of $1,575,000 is $3,550.

Apportioned land tax

David's land tax would be apportioned as follows:

| Property | Site Value | Land tax |

|---|---|---|

| A | Exempt | nil |

| B | $740,000 | $1,667.94 |

| C | $835,000 | $1,882.06 |

| Total | $1,575,000 | $3,550 |

Ownership types

An ownership refers to all land owned by the same registered owner or owners.

If you own land under different ownerships, each ownership is assessed separately based on its total taxable site value ![]() .

.

You may receive separate land tax assessments for:

- Individual ownerships (for land you own or partly own)

- Joint ownerships (for land you own jointly with others)

- Trust ownerships (for land held on trust)

- Corporate Group ownerships (for land owned by Corporate Groups)

You will only receive a land tax assessment if the total taxable site value in an ownership exceeds the land tax threshold and has a land tax liability.

Where land is held by multiple people or entities such as trusts or corporations, each owner is jointly and severally liable for the full land tax shown on a land tax assessment.

The Commissioner of State Taxation can recover the entire land tax from any one of the owners, regardless of their share in the land.

If you only own land individually and you do not own land in any other ownership, all the land in your individual ownership will be assessed, and if the total taxable site value of the land you own exceeds the land tax threshold, you will receive a Land Tax Assessment.

If the total taxable site value of the land you own does not exceed the land tax threshold, you will not receive a Land Tax Assessment.

If you own land in a joint ownership and individually, land owned in the joint ownership will be assessed firstly in the joint ownership and also in your individual ownership.

Step 1

If the total taxable site value of land in the joint ownership exceeds the land tax threshold, you will receive a joint Land Tax Assessment. If the taxable site value in the joint ownership is below the threshold, you will not receive a joint assessment.

Step 2

You will be assessed on your share of jointly owned land and any other land you own or partly own.

If the total taxable site value of the land you own solely plus your share of land owned jointly exceeds the land tax threshold, you will receive an individual Land Tax Assessment.

Deductions

If you receive land tax assessments for both your individual and joint ownerships, a deduction may be applied in your individual Land Tax Assessment to prevent double taxation on the same parcel of land.

- The deduction reflects your share of land tax that has already been assessed in the joint ownership.

- It is applied to your individual ownership against the same jointly owned land.

- If the joint ownership does not incur land tax, no deduction will be applied in your individual assessment.

- If your total deductions exceed your individual land tax liability, your individual land tax liability is reduced to zero, and you will not receive an individual assessment.

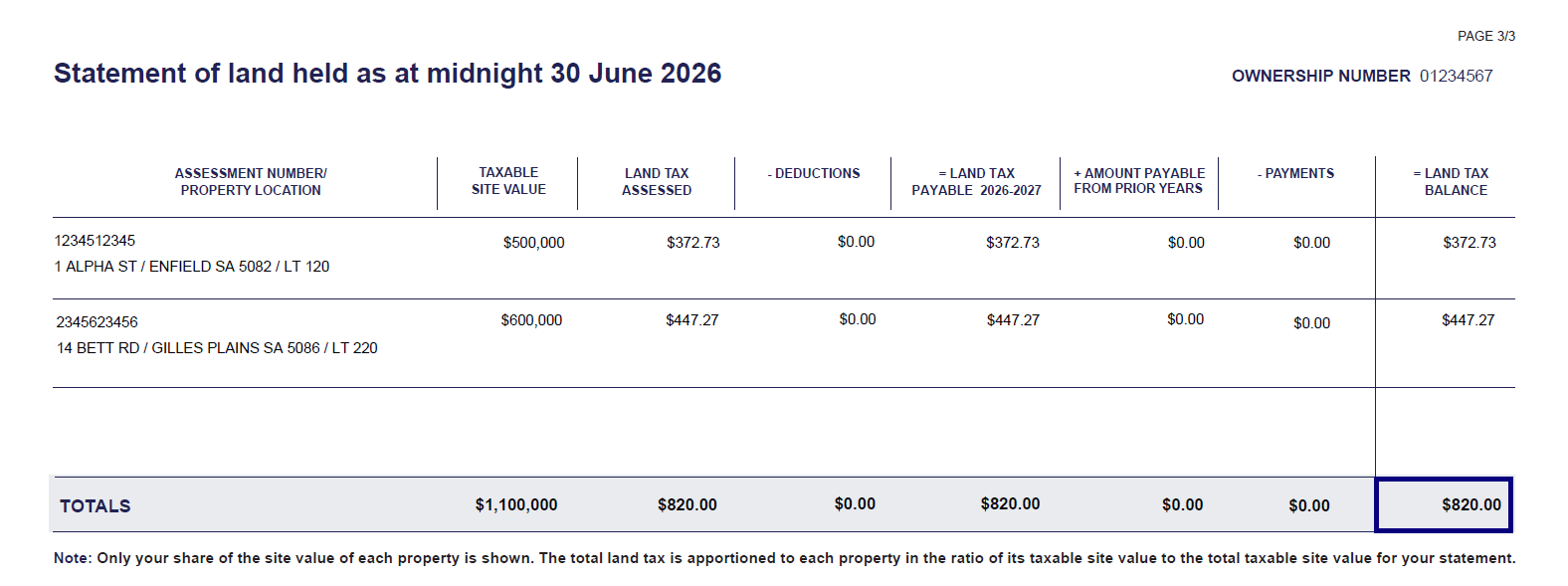

Example - Deduction for jointly owned land

Cara and David

Cara and David jointly own two properties, neither of which is exempt from land tax:

- 1 Alpha Street - site value: $500,000

- 14 Bett Road - site value: $600,000

- Total taxable site value = $1,100,000

Their total taxable site value is over the threshold, so they receive a joint land tax assessment, showing the land tax apportioned to each property:

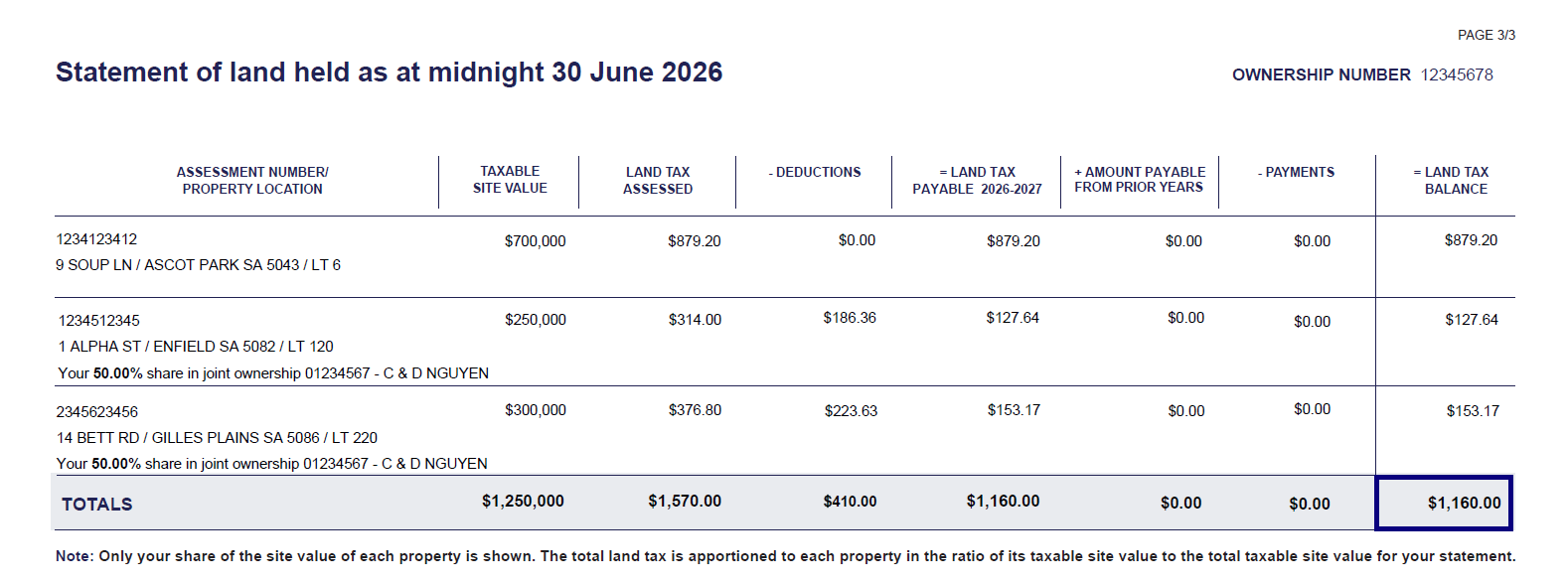

Cara's Individual Ownership

Cara also owns a property in her own name:

- 9 Soup Lane - site value: $700,000

Her individual land tax assessment will show:

- 9 Soup Lane - full ownership: $700,000 (full site value of the property)

- 1 Alpha Street - her 50% share: $250,000 (half of the site value of the property)

- 14 Bett Road - her 50% share: $300,000 (half of the site value of the property)

- Total taxable site value: $1,250,000

Her total taxable site value is over the land tax threshold, so she will receive an individual land tax assessment.

Cara will receive a deduction for her share of the land tax already assessed in the joint ownership:

- Deduction for 1 Alpha Street: $186.36 (50% of the land tax apportioned to the property in her joint ownership)

- Deduction for 14 Bett Road: $223.63 (50% of the land tax apportioned to the property in her joint ownership)

In this case, this deduction does not fully offset her individual land tax liability, so she will receive a Land Tax Assessment based on the total taxable site value of $1.25 million, with deductions applied for her share of jointly owned land.

David's individual ownership

Unlike Cara, David does not own any land in his own right.

His individual ownership would show:

- 1 Alpha Street - his 50% share: $250,000 (half of the total site value of the property)

- 14 Bett Road - his 50% share: $300,000 (half of the total site value of the property)

The total taxable site value is under the land tax threshold, so David will not receive an individual land tax assessment, and no deductions will be applied.

If David's individual ownership was over the tax free threshold (like Cara), David would also receive a deduction for his share of land tax assessed in the joint ownership.

If you only own land under one joint ownership, and you do not own or partly own any land under any other ownership, the land in your joint ownership will be assessed and if the total taxable site value of the land exceeds the land tax threshold, a joint Land Tax Assessment will be issued. You will not receive an individual Land Tax Assessment.

if the total taxable site value of the land in the joint ownership does not exceed the land tax threshold, you will not receive a Land Tax Assessment.

Interest in land - understanding your share

If you own land under a joint ownership, your share of the land will be assessed based on how the land is held:

- Tenants in common: You are assessed on the share specified on the Certificate of Title.

- Joint tenants: Each owner is taken to hold an equal share.

If you are an owner of land for land tax purposes because you are a beneficiary or unitholder of a trust, your share of the land will be assessed based on your beneficial interest in the trust.

You will only receive a land tax assessment for land you own or partly own. If your spouse or domestic partner owns land separately to you, their land holdings are not combined with yours for land tax assessment purposes.

If you are the director or shareholder of a company, the land held by that company will not be included in your individual assessment.

Confirming your share of land ownership

- Your Certificate of Title will show your share of interest in the property .

- You can check your land ownership details or request a copy of your Certificate of Title through the South Australian Integrated Land Information System (SAILIS). A fee may apply.

Property types

Land tax is calculated based on the site value ![]() of the land, not the capital value

of the land, not the capital value ![]() of a property.

of a property.

This means land tax may apply regardless of what types of buildings are on the land, even if individual owners do not have exclusive access the land in their ownership, such as in the case of an apartment building or shared site.

Select from the drop down panels below for more information about how land tax is treated for certain property types.

While there may not be any physical land associated with the apartment, the apartment is built on land, and a site value is determined for each apartment by the Valuer-General.

The owner of the apartment is seen as the owner of the land for land tax purposes.

The owner of the unit, townhouse or similar under a strata or community title is seen as the owner for land tax purposes.

Site value is determined by the Valuer-General for each unit, townhouse or similar. The site value is used to assess land tax.

If the unit, townhouse or similar is owned under a strata or community title, the site value will not include common land (for example, shared driveways).

The relevant community corporation will be liable for any common land that attracts land tax.

Shack site lessees of privately owned land are deemed to be the owner where:

- the shack site is on or adjacent to the banks of the River Murray, a tributary of the River Murray, or a lake or lagoon connected with the River Murray or a tributary of the River Murray; and

- a registered lease existed at midnight 30 June 1989 over the land and the term of the lease is at least 40 years.

The occupier of land in a defined shack-site area is similarly deemed to be the land tax owner. Shack-site areas have been defined as council areas where land is deemed by the Valuer-General to be shack-site land.

Find out more about shack site exceptions and other exceptions in the Land Tax Guide to Legislation.

Land held on trust

Land tax is calculated based on ownership. If you hold land on trust as a trustee, it will be assessed separately from any other land you own or partly own outside of the trust.

If you are a trustee for multiple trusts, you will receive a separate land tax assessment for each trust.

Land held on trust may be subject to trust tax rates, which have:

- A higher rate of land tax, and

- A lower tax-free threshold than the general tax rates.

Important: You must notify RevenueSA within one month of acquiring land on trust.

Failure to notify us may result in interest and penalty tax being charged on the additional amount of land tax that would have applied if you had notified us on time.

Corporate groups

If your corporation is considered related to other corporations, your corporation is part of a Corporate Group.

- All land owned by members of a Corporate Group is assessed at the general tax rates as if owned by a single owner, except for land held by a corporation acting as trustee of a trust.

- Land owned by a corporation as trustee of a trust is assessed separately from land owned by the Corporate Group.

Land tax is calculated based on ownership and property details as at midnight on 30 June each financial year.

- If your Corporate Group structure changes during the financial year, RevenueSA will use data from the Australian Securities and Investments Commission (ASIC) to recognise the change.

- The updated group structure will apply to land tax assessments for the following financial year.

Contact us

When contacting us please provide your ownership number and assessment number. You can find these numbers on your Land Tax Assessment (previously known as a Notice of Land Tax Assessment).

| online | complete a land tax assessment query form |

|---|---|

| contactus@revenuesa.sa.gov.au | |

| phone | (08) 8372 7534 |

| fax | (08) 8207 2100 |

| post |

RevenueSA Kaurna Country GPO Box 1647 ADELAIDE SA 5001 |

You can reach us during business hours, excluding public holidays:

- Monday, Tuesday, Thursday, Friday: 8:30am - 5:00pm (ACST or ACDT)

- Wednesday: 10:00am - 5:00pm (ACST or ACDT)

South Australia observes daylight saving.

- ACST: Australian Central Standard Time is from early April to early October.

- ACDT: Australian Central Daylight Time is from early October to early April.

Do you want to provide feedback or lodge a complaint?

You can do so via our feedback and complaints page.