On this page

This page gives information about the land tax exemption for land used in the business of primary production.

Primary production land tax exemption

Land may be exempt from land tax if it is owned and used wholly or primarily for a relevant primary production business, which can include:

- Agriculture or the gathering in of crops

- Apiculture

- Dairy farming

- Forestry or any other business consisting of the cultivation of soils

- Horticulture

- Intensive agistment of declared livestock (cattle, sheep, pigs or poultry only)

- Pasturage

- Poultry farming

- Propagation and harvesting of fish or other aquatic organisms

- Rearing of livestock

- Viticulture

Eligibility

A primary production exemption can apply to any eligible land within South Australia.

Eligibility and application of this exemption is determined by the:

- land size,

- location of the land (whether the land is located inside or outside the defined rural area),

- use of the land, and

- ownership structure of the land and who is conducting the business activity.

Land size

The land must be 0.8 hectares or greater in area. This may be:

- One parcel of land, or

- The total of a number of pieces of adjoining land which are all used for the primary production business.

Defined rural area

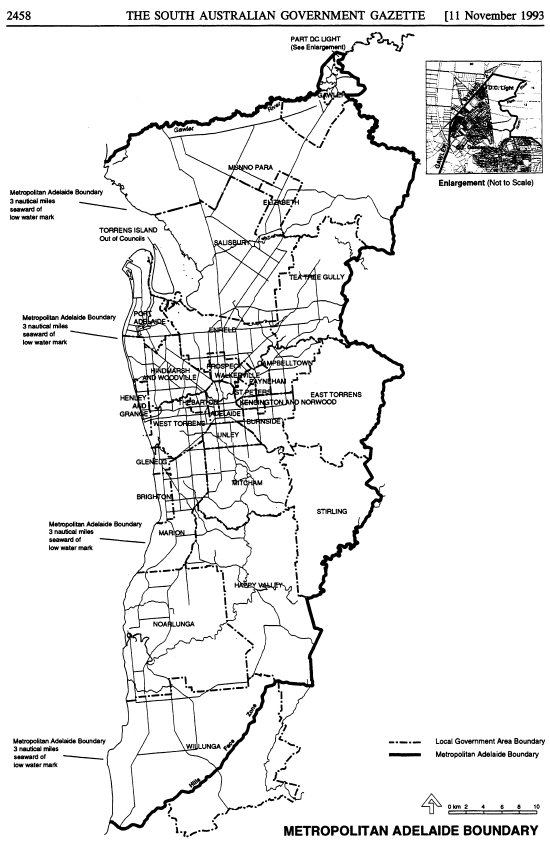

The defined rural area consists predominantly of the greater metropolitan areas of Adelaide and Mount Gambier.

- Metropolitan Adelaide covers an area approximately from Willunga, south of Adelaide, to Gawler, north of Adelaide, and from the coastline in the west to the inner Mt Lofty Ranges in the east.

- Metropolitan Mt Gambier covers the majority of the City of Mount Gambier council area.

Defined rural area map

Reference

Reproduced from the South Australian Government Gazette No 114 (11 November 1993): 2458, accessed from AustLII.

Land outside the defined rural area

RevenueSA will automatically apply the primary production exemption to individual parcels of land greater than 0.8 hectares that have a primary production land use code. Land use codes (LUCs) are assigned by the Valuer-General.

If you own adjoining parcels of land that have a combined area of more than 0.8 hectares (this can include adjoining land that already qualifies for automatic exemption), you will need to submit an application to RevenueSA demonstrating that each parcel of land too small to qualify on its own is used for primary production.

For land located outside the defined rural area, the owner does not need to be the person conducting the business of primary production on the land.

Land inside the defined rural area

For any land located inside the defined rural area, you must apply for the primary production exemption and meet all eligibility criteria.

Different eligibility criteria applies based on the ownership type and business activity of the owners of the land.

A business is considered relevant to land used for primary production if:

- It involves primary production activities on the land, or the processing or marketing of primary produce, and

- The land or its produce is used to a significant extent to support that business.

Select the ownership type that best describes your circumstances below for more information.

Ownership types

Where the land is solely owned by a natural person, the owner must be actively engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

Where the land is held under Joint or common ownership by two or more natural persons:

- At least one owner must be actively engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

- Any co-owners that are not engaged in the business of primary production must be a relative of an owner who is.

Where land is owned by a single company, one of the following conditions must be met:

- A natural person who owns a majority of the company's issued shares is engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

- Two or more natural persons who together own a majority of the company's issued shares are each engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

- Two or more relatives who together own a majority of the company's issued shares, and at least one of them is engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

- The main business of the company must be a business of primary production that is conducted upon the land.

Where the land is owned jointly by multiple companies, or by a combination of companies and individuals:

- The main business of each owner must be the business of primary production conducted upon the land.

Where the land ownership is held by a retired person (solely, jointly or in common):

- Immediately prior to retirement, the retired owner must have been engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

- A close relative of the retired person must currently be engaged on a substantially full-time basis in the business of primary production conducted upon the land, either independently or as an employee.

- If the land is jointly commonly owned, all co-owners must be close relatives of the retired person.

Where the land ownership is held by an executor or administrator of a deceased estate (solely or by tenancy in common):

- Immediately prior to their death, the deceased owner must have been engaged in the business of primary production conducted upon the land on a substantially full-time basis (either on their own behalf or as an employee).

- A close relative of the deceased person must be currently engaged on a substantially full-time basis (either on their own behalf or as an employee) in the business of primary production conducted upon the land.

- If the land is owned jointly or in common, all co-owners of the land must be close relatives of the deceased person.

Relatives, close relatives and domestic partners

A person is a relative of another if:

- they are spouses or domestic partners, or

- one is an ascendant or descendant of the other, or of the other’s spouse or domestic partner,

- one is a brother or sister of the other or a brother or sister of the other’s spouse or domestic partner, or

- one is an ascendant or descendant of a brother or sister of the other or of the other’s spouse or domestic partner.

A person is a close relative of another if:

- they are spouses or domestic partners, or

- one is a parent or child of the other, or

- one is a brother or sister of the other.

A person is the domestic partner of a person if they live with the person in a close personal relationship.

How to apply

Complete the Apply for land tax exemption or relief form. Select Primary production as the property type option that best describes the use or circumstances of the property.

You will need:

- Your ownership number: This can be found in the top right corner of your Land Tax Assessment or Emergency Services Levy Notice of Assessment.

- The assessment number: This can be found on your Land Tax Assessment, Emergency Services Levy Notice of Assessment, water rates, or council rates notice.

- Supporting documentation that evidences that the criteria for exemption are satisfied.

Contact us

When contacting us please provide your ownership number and assessment number. You can find these numbers on your Land Tax Assessment (previously known as a Notice of Land Tax Assessment).

| online | complete a land tax assessment query form |

|---|---|

| contactus@revenuesa.sa.gov.au | |

| phone | (08) 8372 7534 |

| fax | (08) 8207 2100 |

| post |

RevenueSA Kaurna Country GPO Box 1647 ADELAIDE SA 5001 |

You can reach us during business hours, excluding public holidays:

- Monday, Tuesday, Thursday, Friday: 8:30am - 5:00pm (ACST or ACDT)

- Wednesday: 10:00am - 5:00pm (ACST or ACDT)

South Australia observes daylight saving.

- ACST: Australian Central Standard Time is from early April to early October.

- ACDT: Australian Central Daylight Time is from early October to early April.

Do you want to provide feedback or lodge a complaint?

You can do so via our feedback and complaints page.