On this page

This page gives information about transitional land tax relief.

About transitional land tax relief

Amendments to the Land Tax Act 1936 introduced revised land tax aggregation provisions, which came into effect from midnight on 30 June 2020.

Relief on your land tax

This video is intended as a guide only.

We recommend you seek independent advice on state revenue matters and how they impact you and your circumstances.

[chime rings]

[music stops]

Transitional relief will be available for taxpayers whose land tax is higher due to the new method of aggregation.

In a nutshell, aggregation means ‘grouped together’. Aggregation for land tax means land is grouped together according to who owns or part-owns the land.

You can only apply for relief if your land tax is higher because of the changes to aggregation.

The relief doesn’t apply if your increase is because of

the higher trust land tax rates

or because you’ve been nominated as a beneficiary or unitholder of land held on trust

or an increase in your site value

or because you’ve acquired other land

or because an exemption from land tax has ended.

The relief only applies on property you owned at 16 October 2019.

If you sell property, the relief only applies to those properties you still have in the current financial year which you owned at 16 October 2019.

The relief doesn’t apply on properties you’ve bought or acquired after 16 October 2019.

To be eligible for relief your tax increase needs to be between $2,500 and $102,500 higher than it would have been using the 2019-20 land tax rates and aggregation method.

No relief is payable on the first $2,500 of your land tax assessment increase.

After you have applied for relief, if you are eligible, the amount of relief you receive will be taken off the amount you owe in land tax.

If you have outstanding land tax from previous years, you must be in a payment arrangement with RevenueSA to be eligible and any relief you receive will offset your outstanding debt before any refund is issued.

The maximum relief in the 2020-21 financial year is up to 100% of your increase to a maximum of $100,000.

If your increase is above the maximum of $102,500, you are not eligible for any land tax relief.

The maximum relief available is scheduled to change in the 2021-22 and 2022-23 financial years.

Your increase still needs to be between $2,500 and $102,500 to claim for relief in those years.

In 2021-22 the relief is 70% of your land tax increase to a maximum of $30,000.

In 2022-23 the relief is 15% of your land tax increase to a maximum of $15,000.

See our website for examples of different scenarios.

Applying for the relief is quick and easy via RevenueSA Online.

[music plays]

More information can be found at www.revenuesa.sa.gov.au/landtax

Eligibility

You may be eligible for full or partial land tax relief if your Land Tax Assessment for the 2020–21, 2021–22, or 2022–23 financial year increased by:

- More than $2,500, and

- Less than or equal to $102,500.

You are not eligible for relief if the increase results from any of the following:

- The increase is due to higher trust rates of land tax that apply to certain trusts

- Nomination of beneficiaries, unitholders, or a designated beneficiary (for fixed trusts, unit trust schemes, and discretionary trusts respectively)

- Purchase of additional land

- Loss of an exemption on land

- An increase in site value

Eligible Land

Relief applies only to land that:

- You owned or partly owned as at midnight, 16 October 2019, and

- You still own in the land tax year for which you are applying (2020–21, 2021–22, or 2022–23)

Land acquired after midnight, 16 October 2019 is not eligible.

Relief is assessed per parcel of land, not based on total landholdings.

How to apply

- Complete the Land Tax Transitional Fund Application form.

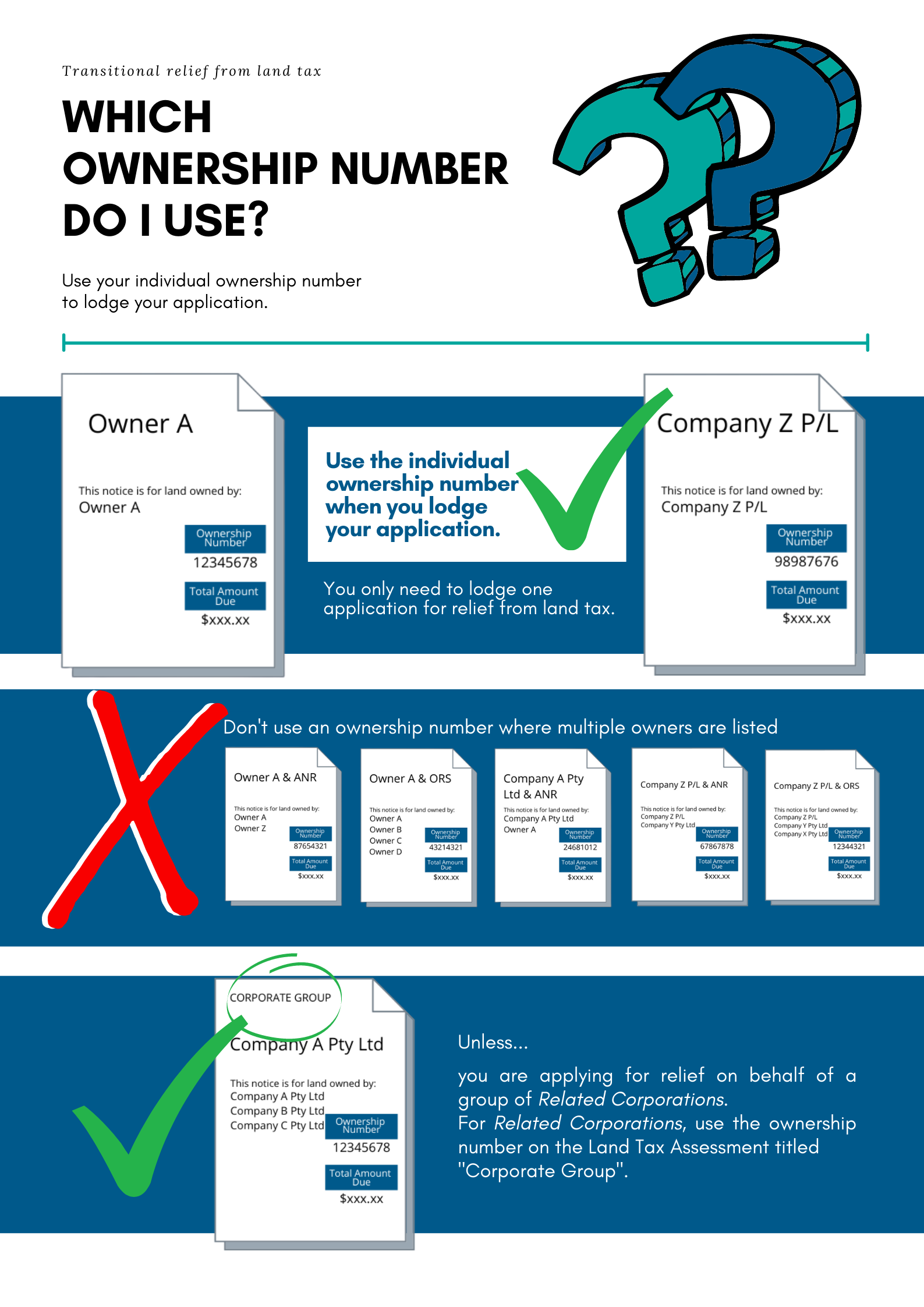

- If you have received more than one Land Tax Assessment, you need to use the individual ownership number when you apply (not ownership numbers where multiple owners are listed).

- Corporate Groups should use the ownership number on the Land Tax Assessment titled 'Corporate Group.'

[music plays]

Relief on your land tax: which details do I use to apply?

This video is intended as a guide only.

We recommend you seek independent advice on state revenue matters and how they impact you and your circumstances.

[music fades]

Tom has received his Land Tax Assessments.

[whoosh sound]

He owns land in multiple ownerships.

[pop sounds]

His land tax is higher than it would have been if the 2019-20 method of aggregation was still in place and he’s eligible for relief.

He can apply for relief, but which of his many ownership numbers does he use?

Tom has an individual Land Tax Assessment,

a Land Tax Assessment for property jointly owned with one other,

a Land Tax Assessment for property jointly owned with others and

a Land Tax Assessment for property he owns jointly with a corporation.

Tom needs to use his individual ownership number when he applies. He only needs to lodge one application.

Applying for the relief is quick and easy via RevenueSA Online.

Corporations can find details about which information to use on our website.

Other information

I have a land tax liability from a prior year. Am I still eligible?

If you have outstanding land tax obligations from a year prior to the 2020-21 financial year, you must have entered into a payment arrangement with RevenueSA in respect to the payment of the outstanding land tax amount to be eligible for relief.

How much is the relief?

Relief is not provided on the first $2,500 of the increase. For example, if your Land Tax Assessment has increased by $3,000, you may be eligible for up to $500 in relief.

Relief available is shown in the table below:

The relief is assessed on each relevant parcel of land, not at the total ownership level.

I have a land tax liability from a prior year. Am I still eligible?

If you have outstanding land tax obligations relating to prior years' liabilities, you must have entered into a payment arrangement with RevenueSA to be eligible for relief. The relief will reduce any outstanding land tax debt before a refund will be provided.

How much is the relief?

Relief is not provided on the first $2,500 of the increase. For example, if your Land Tax Assessment has increased by $3,000, you may be eligible for up to $500 in relief.

Relief available is shown in the table below:

| Financial year | Minimum increase | Maximum increase | Relief amount |

|---|---|---|---|

| 2020-21 | $2,500 | $102,500 | 100% of increase above $2,500 to a maximum of $102,500 |

| 2021-22 | $2,500 | $102,500 | 70% of increase above $2,500 to a maximum of $102,500 |

| 2022-23 | $2,500 | $102,500 | 15% of increase above $2,500 to a maximum of $102,500 |

How is the relief calculated?

The value of relief will be calculated on the difference between land tax payable, compared to the land tax that would have been payable on the relevant properties under the aggregation approach, tax rates and thresholds that applied in 2019-20.

More detailed information on the relief, how it is calculated and examples is available in the Transition Fund Guidelines.

Which ownership number do I use to apply?

If you have received more than one Land Tax Assessment, you need to use the individual ownership number when you apply.

Click on image to view larger version

Contact us

When contacting us please provide your ownership number and assessment number. You can find these numbers on your Land Tax Assessment (previously known as a Notice of Land Tax Assessment).

| online | complete a land tax assessment query form |

|---|---|

| contactus@revenuesa.sa.gov.au | |

| phone | (08) 8372 7534 |

| fax | (08) 8207 2100 |

| post |

RevenueSA Kaurna Country GPO Box 1647 ADELAIDE SA 5001 |

You can reach us during business hours, excluding public holidays:

- Monday, Tuesday, Thursday, Friday: 8:30am - 5:00pm (ACST or ACDT)

- Wednesday: 10:00am - 5:00pm (ACST or ACDT)

South Australia observes daylight saving.

- ACST: Australian Central Standard Time is from early April to early October.

- ACDT: Australian Central Daylight Time is from early October to early April.

Do you want to provide feedback or lodge a complaint?

You can do so via our feedback and complaints page.