Employment Agency

Status: Current

Legislation: Payroll Tax Act 2009

Date Issued: 8 July 2011

Information Circulars do not have the force of law.

Preface

This Information Circular provides information for employment agents regarding their payroll tax liabilities under the Payroll Tax Act 2009 (the “Act”), but it does not constitute a Revenue Ruling.

If any uncertainty exists with a particular aspect of the information provided, please contact RevenueSA. The information provided in this Information Circular is correct at the time of publication.

A reference to state(s) includes the Australian Capital Territory and the Northern Territory.

Overview

The employment agency provisions apply to employment agency contracts and are contained in Division 8, Part 3 of the Act. Employment agency contracts are defined in section 37(1) of the Act as:

a contract, whether formal or informal and whether express or implied, under which a person (an employment agent) procures the services of another person (a service provider) for a client of the employment agent.

For more information on contractors engaged under a relevant contract, see the Payroll Tax: Contractors information Circular.

Section 37(3) of the Act defines a ‘contract’ to include an agreement, an arrangement or an undertaking. However, Section 37(2) states that a contract is not an employment agency contract if it is, or results in the creation of, a contract of employment between the service provider and the client.

Essentially, an employment agency contract exists where an employment agent ‘on-hires’ a service provider to their client, and the client and service provider do not enter into any form of agreement between themselves.

Typically, an employment agency arrangement involves the following:

- the service provider contracting with the employment agent; and

- the employment agent contracting with the client.

The above arrangement can be differentiated from a ‘placement’ arrangement where the parties would typically contract as follows:

- service provider with the client;

- employment agent with the client; and/or

- service provider with the employment agent.

Section 32(3) of the Act provides that an ‘employment agency contract’ is not a ‘relevant contract’. Therefore, employment agents do not have access to the exemptions contained in the contractor provisions in section 32(2) of the Act for their employment agency contracts.

Deeming provisions

The Act contains several deeming clauses that determine the South Australian payroll tax liability of employment agents. Under an employment agency contract:

- the employment agent is deemed to be an employer;

- the service provider or on-hired worker is deemed to be an employee of the employment agent regardless of the structure through which services are provided; and

- all payments made to (or on behalf of) the service provider are deemed to be wages regardless of the service provider’s structure (that is, a company, partnership or individual).

Liability

What is liable?

The Act provides that wages paid or payable by an employment agent under an employment agency contract are:

- any amount paid or payable to, or in relation to, the service provider in respect of the provision of services in connection with the employment agency contract;

- the value of any benefit provided for or in relation to the provision of services in connection with the employment agency contract that would be a fringe benefit if provided to a person in the capacity of an employee; and

- any payment made in relation to the service provider that would be a superannuation contribution if made in relation to that person in the capacity of an employee.

What is not liable?

Allowances and Reimbursements paid to Service Providers

Allowances paid to employees are generally subject to payroll tax. Accordingly, allowances paid to service providers (or on-hired workers) constitute deemed wages. The only allowances that may not be wholly taxable are:

- accommodation allowances;

- motor vehicle allowances; and

- living away from home allowances.

Accommodation or motor vehicle allowances paid to a service provider are deemed wages only to the extent that these allowances exceed the exempt rates. Living away from home allowances are deemed wages only if they are taxable under the Fringe Benefits Tax Assessment Act 1986 (Cwlth) (the “FBT Act”).

For further information see Revenue Ruling PTA005.

Reimbursements of business expenses incurred by employees on behalf of their employers are not taxable unless they have a taxable value under the FBT Act. A reimbursement of an expense is not subject to payroll tax if it has all of the following characteristics:

- at the time of payment, the expense has already been incurred by the employee (if the payment was made in advance, the employee has provided the employer with a receipt relating to the expense and refunded any excess from the advance payment);

- the expenditure by the employee was incurred in the course of the employer’s business; and

- the precise amount is reimbursed.

Payroll tax is not imposed on amounts paid as reimbursements of business expenses (as described above) by the employment agent to the service provider.

The employment agent must retain sufficient information to demonstrate that the payment is a reimbursement (for example, copies of receipts provided by the service provider).

For further information see Revenue Ruling PTA011.

What is not liable?

GST

Section 44(1) of the Act specifically excludes any Goods and Services Tax (GST) payable on the supply to which wages paid or payable relates. Therefore, the GST portion of the payment to a service provider under an employment agency contract is not included as wages for payroll tax purposes.

What is not liable?

Exempt organisations

An exemption for employment agents is provided under Section 40(2) of the Act for wages paid to a service provider, under an employment agency contract, where:

- the wages would be exempt from payroll tax under Part 4 (other than under Division 4 or 5 of that Part or section 50) of the Act had the wages been paid by the client to the service provider as an employee; and

- the client has given the employment agent a declaration to that effect (Employment Agency Contracts - Declaration by Exempt Clients form can be used to make this declaration).

Wages that are exempt under Part 4 of the Act include those paid by the following organisations:

- non-profit bodies having as their sole or dominant purpose a charitable purpose (but not including a school, an educational institution, an educational company or an instrumentality of the State of South Australia);

- public benevolent institutions (but not including an instrumentality of the State of South Australia);

- religious institutions;

- certain not-for-profit schools providing education at or below the secondary level;

- public and non-profit hospitals;

- health care service providers; and

- councils (except for wages paid in relation to certain activities - section 59 and 60).

The employment agent must obtain a declaration from the client before claiming the exemption.

There is no exemption for the employment agent merely because the client’s wages are below the payroll tax threshold.

For further information see Revenue Ruling PTA026.

Nursing agencies

Generally the employment agency provisions will apply in the same way to nursing agencies as they do to other employment agents.

However, in some instances, a nurse’s wages may be paid through an employment agency even though the nurse is actually an employee of the client.

Under such circumstances, the contract is not an employment agency contract and the employment agency provisions do not apply. In this situation the client is liable for any payroll tax in respect of wages paid or payable to the nurse notwithstanding that the payment is made to the nurse via the employment agent.

If the nurse is not an employee of the client, or has not been engaged by the client under a relevant contract, then the payroll tax liability shall remain with the employment agent.

Government departments and agencies

Commonwealth government

Payments made for workers on-hired to Commonwealth government departments and agencies are subject to payroll tax under the employment agency provisions. The exception to this is where the Commonwealth government agencies come within the exemptions in Part 4 of the Act as those exemptions do not apply to Commonwealth government departments.

For constitutional reasons, states cannot legislate to tax the Commonwealth. However, under the employment agency provisions, payroll tax is imposed on the employment agents and not on the Commonwealth government departments and agencies.

State government

Similarly, payments made for workers on-hired to South Australian government departments and agencies are subject to payroll tax under the employment agency provisions. The exception to this is where the South Australian government agencies come within the exemptions in Part 4 of the Act as those exemptions also do not apply to state government departments.

As is the case with Commonwealth government departments and agencies, the payroll tax liability is imposed on the employment agents and not on the state government departments and agencies.

Local government

Conversely, wages paid or payable by a local government (except for wages relating to certain municipal construction or business operations) are exempt from payroll tax under section 58 of the Act. Consequently, provided that the client who is a municipal council has given the employment agent the relevant declaration (Employment Agency Contracts - Declaration by Exempt Clients form may be used for this declaration), wages relating to workers on-hired to the municipal council are exempt from payroll tax under section 40(2) of the Act.

For further information see Revenue Ruling PTA028.

Chain of on-hire

In some cases multiple employment agency contracts may arise. For example, there can be situations where one employment agent on-hires labour to another employment agent, which then further on-hires that labour to their client.

For further information see Revenue Ruling PTA027.

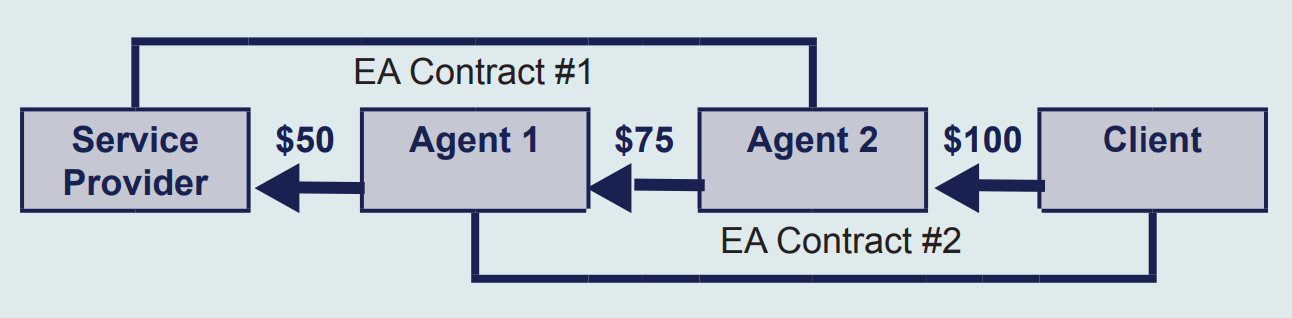

Example

In this scenario, there is a chain of on-hire comprising of two employment agency contracts:

EA Contract #1: Agent 1 procured the services of the Service Provider for Agent 2.

EA Contract #2: Agent 2 procured the Service Provider (via Agent 1) for its Client.

A strict application of the employment agency provisions would result in both amounts ($75 paid by Agent 2 to Agent 1 and $50 paid by Agent 1 to the Service Provider) being taxable wages.

However, the Commissioner of State Taxation (the “Commissioner”) has ruled in Revenue Ruling PTA027 that in these circumstances, only the employment agent that is closest to the ultimate client will be regarded as being liable for payroll tax.

Applying Revenue Ruling PTA027 to the above example, Agent 2 is closest to the Client and is therefore liable for payroll tax on $75. Upon receiving a declaration (Employment Agency Contracts - Chain of on-hire declaration form may be used for this declaration) from Agent 2 confirming its intention to bear the payroll tax liability in respect of the $75, Agent 1 is not required to pay payroll tax in respect of $50 paid to the Service Provider.

However, if the total wages of Agent 2 are under the payroll tax threshold, the liability shifts to Agent 1. Under these circumstances, Agent 1 would be liable for payroll tax on the $50 paid to the Service Provider.

Anti-avoidance provisions

Section 42 of the Act provides that if the effect of an employment agency contract is to reduce or avoid payroll tax liability of any party to the contract, the Commissioner may:

- disregard the contract;

- determine that any party to the contract is deemed to be an employer for the purposes of the Act; and

- determine that any payment made in respect of the contract is deemed to be wages for the purposes of the Act.

View this Information Circular as a PDF (PDF 244KB)