Amongst other things, the Act contains provisions which set out when land owned subject to a trust is:

- exempt from land tax;

- liable for the either the trust or general land tax rates; and

- subject to aggregation with other land or assessed separately.

Trustees must notify RevenueSA within one month of certain changes occurring with respect to trust held land. These requirements are outlined below.

The following discussion sets out how trusts will be assessed for land tax.

Land subject to a trust that is excepted or exempted from land tax

Land that is exempt from land tax under the Act is not liable to land tax, including where the land is subject to a trust. Accordingly, land that is exempted from land tax will not be included in the taxable value of land in an assessment of a land tax liability.

The following discussion therefore proceeds on the basis that any land fully exempted from land tax will not be included in any assessment of a land tax liability.

Separate assessment of trust land

Other than where expressly provided for, pursuant to Section 11, where an owner is the owner of land as trustee of a trust (other than a trust arising because of a contract to purchase or acquire an estate or interest in the land), the trustee is to be assessed land tax on the whole of the land subject to the trust as if the land were the only land owned by the trustee.

This means that where an interest in land is held on trust, either by a trustee or trustees jointly (where two or more people own an interest in a parcel of land as trustees for the same trust, they will be treated as a single owner), the taxable value of the interest in the land:

- will be aggregated with the taxable value of all other land owned by the trustee(s) that is subject to the same trust (except where the trust is an excluded trust); but

- will not be aggregated with the taxable value of other land owned by the same owner in its own capacity, or as trustee of a different trust.

Example 5

land held on trust

Sam owns:

- land as the trustee of the First Trust (total taxable value of $500,000);

- land as the trustee of the Second Trust (total taxable value of $600,000);

- land with Alex both as trustees of the Third Trust (total taxable value of $650,000); and

- land that is not subject to a trust (total taxable value of $700,000).

None of the land that Sam is an owner of is subject to aggregation. Sam will receive four separate assessments for the:

- land owned as trustee of the First Trust (total taxable value of $500,000), calculated using the trust rates (unless a nomination is made);

- land owned as trustee of the Second Trust (total taxable value of $600,000), calculated using the trust rates (unless a nomination is made);

- land owned together with Alex as trustees of the Third Trust (total taxable value of $650,000), calculated using the trust rates (unless a nomination is made);

- land that is not subject to a trust (total taxable value of $700,000), calculated using the general rates.

Trust rates of land tax

Pursuant to Section 8A(1a), land held on trust for a fixed, discretionary or unit trust is generally assessed at the trust rates of land tax, unless a notice of the beneficial interest(s)/unit holdings or a designated beneficiary is in place (discussed further below) (Sections 8A(1b)(a), (b) or (c) for fixed trusts, unit trust schemes and discretionary trusts respectively).

The trust rates of land tax do not apply to land held by:

- an excluded trust (Section 8A(1b)(d));

- an implied, constructive or resulting trust (Section 13E);

- public unit trust schemes, being either a listed trust or a widely held trust (Section 8A(1b)(e)); or

- a corporation that holds land in its capacity as trustee of a trust and that corporation is grouped with one or more related corporations that own land and land tax is assessed in accordance with Section 13J (Section 8A(1c)), that is, in the case of related corporations arising pursuant to Section 13G(5) (discussed further below).

An exclusion from the higher trust rates does not exempt land from land tax. Instead, the general rates of land tax rates will apply.

The trust rates of land tax will apply where the land held on trust has a total site value greater than $25,000, where a notice of beneficial interest(s)/unit holdings or a designated beneficiary is not in place.

Where the trust rates of land tax apply, land tax is payable on the full value of the land held on trust (i.e. as though there was no tax free threshold). Land tax will not be payable though until the total value of the land held on behalf of the trust exceeds $25,000 (note that pursuant to Section 6, where the total amount of land tax payable by any taxpayer in respect of any year would be less than $20, no land tax is payable by the tax payer).

The trust rates incorporate an additional 0.5% on top of the general land tax rates for land holdings valued below the top marginal tax threshold.

When the total value of the taxable land exceeds the highest land tax threshold, the general and trust land tax rates are the same, with the rates being capped at the top marginal tax rate of 2.4%.

Trustees, at most, will pay an additional $6,452 for the 2020-21 financial year due to the higher rates of land tax applicable to trust held land.

A trustee has the option to notify RevenueSA of a designated beneficiary, beneficiaries or unitholders of a trust (for discretionary, fixed and unit trusts respectively).

Where a notice of beneficial interest(s)/unitholdings is in place, the trustee will not be liable for the higher trust rates of land tax. The trustee will instead be assessed at the general rates and the beneficiaries or unitholders, who will also be considered an owner (though not to the exclusion of the trustee), will be assessed for their interest in the trust held land in any individual assessments they receive.

Trustee notification requirements

Other than where land has been exempted from land tax by the Commissioner of State Taxation (the “Commissioner”), trustees must notify RevenueSA by 31 July 2020 that they own South Australian land on trust (unless they have previously notified RevenueSA that they are a trustee of land for the purposes of the Act and have received confirmation from RevenueSA that RevenueSA has recognised that the owner holds the land in their capacity as trustee of a trust).

Notifications can be provided via the RevenueSA Online portal available at www.revenuesaonline.sa.gov.au/login or by completing the Notification of Land Held on Trust form.

If a person does not have access to a computer or someone that can provide assistance, they can contact RevenueSA on 8226 3750 (option 2) for an alternative method.

In addition, trustees must notify RevenueSA within one month where the following occurs:

- they become a trustee of a trust that land is held on behalf of, including where they are already a trustee and acquire further land as trustee;

- the circumstances change so that proper grounds for an exemption from land tax cease to exist in regards to trust held land;

- they dispose of any land subject to the trust if the disposal does not result in any change in the legal ownership of the land;

- anything happens that results in the trust to which the land is subject becoming a different category of trust (being any of a fixed trust, a unit trust scheme, a discretionary trust, an excluded trust or a public unit trust scheme), e.g. a discretionary trust becomes a fixed trust;

- there is a change in the beneficial interest(s) of a fixed trust, where a notification of beneficial interest is in force;

- there is a change of unit holdings in a unit trust, where a notification of unit holdings in the trust is in force;

- where a corporation is the trustee of a fixed trust or a unit trust scheme and a corporation becomes, or other related corporations between them become, the owner of more than 50% of:

- where corporation 1 is the trustee of a fixed trust—the total beneficial interests in land subject to the trust; or

- where corporation 1 is the trustee of a unit trust scheme—the total number of units held by the unit holders in the scheme;

- the administration of a deceased estate that includes land in South Australia is completed; or

- where notification has not been provided previously by the trustee of an administration trust – probate being granted or letters of administration having been issued.

Failing to notify within the required time limit may give rise to a tax default under the Taxation Administration Act 1996. When this happens, the trustee may be liable for interest and penalty tax on the additional amount that would have been assessed if the trustee had notified within the required time.

Taxing trusts

There are different land tax considerations for different trust types or scenarios:

- discretionary trusts;

- unit trusts;

- fixed trusts;

- trusts where a beneficiary of a trust (first trust) is a trustee of another fixed or unit trust (second trust) ("a beneficiary trustee")

- excluded trusts;

- implied, constructive or resulting trusts; and

- public unit trust schemes (being either listed trusts or a widely held trusts).

For land tax purposes, a discretionary trust is a trust under which the vesting of the whole or any part of the trust property is either:

- required to be determined by a person either in respect of the identity of the beneficiaries or the quantum of interest to be taken, or both, or

- will occur in the event that a discretion conferred under the trust is not exercised.

A discretionary trust does not include an excluded trust.

In most instances, a trust established for the benefit of a family group is a discretionary trust. The trustee has the discretion as to which beneficiary can benefit from the trust fund and in what amount. If the trustee does not exercise the discretion, the trust deed sets out who will benefit from the trust fund.

Taxing discretionary trusts

The treatment of land held on behalf of a discretionary trust for land tax depends on:

- whether or not the land was subject to the trust at midnight on 16 October 2019 (being the prescribed time);

- if the land was subject to a trust as at midnight on 16 October 2019, whether there is a designated beneficiary in place; and

- whether the land constitutes the principal place of residence (“PPR”) for the trustee or the designated beneficiary.

Land subject to the trust as at midnight on 16 October 2019 (pre-existing trust land)

Land subject to a trust as at midnight on 16 October 2019 and held by a trustee of a discretionary trust will be taxed at trust rates of land tax, unless the trustee lodges with RevenueSA a written notice specifying one (1) beneficiary of the trust who is taken to be the designated beneficiary of the trust.

If there is a designated beneficiary in place, the trustee and the designated beneficiary will be assessed in two stages, with the trustee and the beneficiary being assessed at the general land tax rates (and not the trust rates of land tax).

If there is no designated beneficiary, or the designated beneficiary notice is lodged after 30 June 2021, or if the designated beneficiary notice is withdrawn by the trustee or the designated beneficiary, the trustee is assessed at the trust rates of land tax.

However, as discussed further below (see Beneficiary-trustees of fixed and unit trusts), if a notification is provided by a fixed trust or a unit trust scheme and a beneficiary/unitholder is a discretionary trust, the trust land tax rates will automatically apply to that particular interest in land that the discretionary trust is deemed to hold, including land that was subject to a fixed trust or unit trust scheme as at midnight on 16 October 2019.

Designated beneficiary

A trustee of a discretionary trust may only nominate one beneficiary who will be taken to be the designated beneficiary for that trust.

The deadline for nominating a designated beneficiary for pre-existing trust land is 30 June 2021.

Once this deadline has passed, RevenueSA will not accept late notices of designated beneficiaries.

The notice will take effect at the option of the trustee for either the tax year in which the notice is lodged or for the following year.

A designated beneficiary for land tax purposes must:

- be a natural person

- be a beneficiary of the trust as at midnight on 16 October 2019

- be over 18 years of age and

- have verified by statutory declaration that they consent to being the designated beneficiary of the trust.

If all the beneficiaries of the trust are under 18 years of age, the trustee is able to be the designated beneficiary provided they are a natural person.

The trustees of discretionary trusts will only be able to nominate a designated beneficiary for land tax purposes for land that the trustee owned, on behalf of the trust, as at midnight on 16 October 2019, with the land then being assessed at the general rates of land tax. This requirement likewise applies where there has been a change of trustee(s) (i.e. the trustee(s) has been replaced, an additional trustee has been added, or one removed).

Any land that becomes subject to a discretionary trust from 17 October 2019 onwards will be assessed at the higher trust rates.

A designated beneficiary may be substituted—

- if the designated beneficiary dies or becomes incapacitated; or

- if the Commissioner is satisfied that, because of a marriage, de facto relationship or domestic relationship that has broken down irretrievably, the designated beneficiary will no longer be a beneficiary of the trust; or

- in circumstances prescribed by the regulations. At the time of publication, there are no regulations. Should there be any regulations be made in regards to this point, this section will be updated accordingly.

To substitute a designated beneficiary, the trustee must provide written notice to the Commissioner advising the Commissioner of the reasons for the substitution and the name of another beneficiary of the trust who is to be taken to be the new designated beneficiary.

If the notice of the designated beneficiary is withdrawn by the trustee, or where the designated beneficiary notifies the Commissioner, in writing, that they no longer consent to being the designated beneficiary (as opposed to where the designated beneficiary can be substituted), the trustee will not be able to later lodge another notice and will be liable for land tax at the trust rates of land tax.

The withdrawal of the notice will take effect, for the financial year following the date the notification is received.

Where a trustee has nominated a designated beneficiary, the land subject to the trust will be aggregated with any other interests in land that the designated beneficiary owns. In other words, it will be treated like any other land they own or are deemed to be an owner of.

PPR exemption for discretionary trusts

In the first instance, land owned by a trustee who is a natural person which constitutes their PPR may be eligible for a land tax exemption.

If a designated beneficiary notice is in force, the designated beneficiary is considered to be an owner of any land held on behalf of the trust. If that land includes land that is occupied by the beneficiary as his or her PPR, that land may be eligible to receive an exemption from land tax if:

- the land constitutes the designated beneficiary’s PPR; and

- the land would, if it were owned by a natural person, be wholly or partially exempted from land tax on the basis that it is the designated beneficiary’s PPR.

If those conditions are met, the land that is occupied by the designated beneficiary as his or her PPR would be exempt from land tax and will not be included in the assessment of land tax for the trustee or the beneficiary.

However, once a notice is withdrawn, the designated beneficiary will no longer be considered an owner of the land held on behalf of the trust, and the land will no longer be eligible to receive a PPR exemption on this basis that it is the designated beneficiary’s PPR. Land tax will then be assessed against the land, using the trust rates of land tax.

Where:

- a trustee of a discretionary trust held land as at midnight 16 October 2019 but does not nominate a designated beneficiary by 30 June 2021; or

- land becomes subject to a discretionary trust from 17 October 2019 onwards,

only a trustee who is also a natural person and living upon the land as their PPR will be eligible to claim a PPR exemption.

Assessment of pre-existing trust land held by discretionary trusts with a designated beneficiary

A discretionary trust with pre-existing trust land and a designated beneficiary notice in force will be assessed in two stages (please refer to the joint ownership information for instances where land is jointly owned by multiple owners, with there being an assessment stage at the joint ownership level prior to the two stages discussed further below).

Stage 1 - Assessing the trustee of the discretionary trust

The trustee is assessed at the general rates for pre-existing trust land held on behalf of the discretionary trust.

All land held by the same trustee for the same trust will be aggregated together and land tax will be calculated on the total site value of the land held on behalf of the trust.

The trustee will receive a notice of assessment for the land tax assessed against the land they hold on behalf of the trust.

Where the trustee owns a portion of a parcel of land on behalf of a trust, their land tax assessment will include a deduction equal to the trustee’s portion of the land tax assessed under the joint ownership that they are a member of. This deduction will reduce the land tax payable under the trustee’s ownership and, in some cases, the trustee may not have any further land tax liability to pay.

Where the deduction reduces the land tax payable to zero, a notice of assessment will not be issued to the trustee.

Stage 2 - Assessing the designated beneficiary

The designated beneficiary will be assessed land tax based on their interest in all land they own, including any land that they hold in their own capacity and any land held on behalf of a trust of which they are the designated beneficiary.

The designated beneficiary’s assessment will include a deduction equal to the land tax assessed under the trust ownership (Stage 1 above).

If the designated beneficiary does not own other taxable land (i.e. in their own capacity or as a beneficiary of another trust), the deduction will reduce the land tax payable to zero and there will be no further land tax liability for the designated beneficiary.

If the designated beneficiary owns other land, the designated beneficiary is assessed on all of their interests in taxable land, including land they own by themselves or jointly with others, at the general rates of land tax.

Trust deduction

To avoid double taxation, any land tax assessed against the trustee in respect of pre-existing trust land is to be deducted from the land tax assessed against the designated beneficiary. The deduction is applied to the total land tax assessed for the designated beneficiary and not just to the land tax assessed for the land subject to the trust.

The deduction will never reduce the amount of land tax assessed against the designated beneficiary below zero.

If, after the trust deduction, a designated beneficiary is not liable for land tax, they will not receive a notice of assessment.

A designated beneficiary can find their deduction on their notice of assessment.

Example 6

Land held on trust

George is the trustee of 3 separate discretionary trusts. He owns for each trust separately a single parcel of land with a site value of $300,000 (combined $900,000 in site value).

George, as trustee, will be assessed at the trust rates of land tax on each of the trusts separately.

Alternatively, George has the option of nominating a designated beneficiary for each trust.

Where a designated beneficiary is nominated, a trust with the nomination in place will be liable for land tax at the general rates of land tax rather than the trust rates of land tax. In this example, as the site value of each property falls under the land tax free threshold, there is no land tax payable by George.

The designated beneficiary will have the value of land held on trust aggregated with any other land they are an owner of for land tax purposes. Any land tax payable by the trustee is to be deducted from any land tax payable by the designated beneficiary. In this case, no deduction will be available to the designated beneficiary as there is no land tax payable by the trustee.

Land acquired from 17 October 2019 onwards (subsequent trust land)

Land acquired by a trustee of a discretionary trust from 17 October 2019 onwards will be taxed at the trust rates of land tax.

This applies even if the trustee has designated a beneficiary for pre-existing trust land.

Land tax on both pre-existing trust land and subsequent trust land

For discretionary trusts that own both pre-existing trust land and subsequent trust land, without a designated beneficiary in place, land tax is calculated using the trust rates of land tax on the total value of the land held on behalf of the trust.

For discretionary trusts that own both pre-existing trust land and subsequent trust land, with a designated beneficiary nomination in place, land tax is calculated by using the following formula that proportionally applies the general rates of land tax to pre-existing trust land, and the trust rates of land tax to subsequent trust land:

L = [(R1 * T) * (A / T)] + [(R2 * T) * (B / T)]

Where

L = Land tax assessed

R1 = General land tax rates

R2 = Trust land tax rates

T = Total taxable value of all land subject to the trust

A = Total taxable value of all pre-trust land

B = Total taxable value of all post-trust land.

For land tax purposes, a unit trust is an arrangement made for the purpose, or having the effect, of providing facilities for participation by a person, as a beneficiary under the trust, in any profit or income arising from the acquisition, holding, management or disposal of property under the trust.

Beneficiaries of a unit trust are generally called unitholders and are entitled to trust funds in proportion to their unitholdings.

A unit trust does not include an excluded trust.

Taxing unit trusts

A trustee of a unit trust has two options which are to:

- notify RevenueSA of all the unitholders of the trust and pay land tax at the general rates of land tax; or

- not notify RevenueSA and pay land tax at the trust rates of land tax.

Effect of notifying of unitholders

By notifying RevenueSA of the unitholders:

- both the unitholders and the trustee will be considered owners of the land held by the trustee on behalf of the trust; and

- the trustee will be assessed at general rates of land tax.

Each unitholder will be treated as if they own a percentage of the trust land which is equal to the number of units they hold as a fraction of the total number of units of the trust.

The notification of unitholdings will take effect at the option of the trustee for either the tax year in which the notification is lodged or for the following year.

If there is a change in the unitholdings while a notification of unitholdings is in force, the trustee must notify RevenueSA within one month of the change. Failing to notify may give rise to a tax default under the Taxation Administration Act 1996. When this happens, the trustee may be liable for interest and penalty tax on the additional amount of land tax that would have been assessed if the trustee had notified RevenueSA.

The notification remains in force until it is withdrawn by the trustee. If the notification is withdrawn, the trustee will not be able to lodge another notification and is liable for land tax at the trust rates of land tax.

Unlike discretionary trusts, a unitholder cannot withdraw a notice of unitholders.

PPR exemption for unit trusts

In the first instance, land owned by a trustee who is a natural person and which constitutes their PPR may be eligible for a land tax exemption.

If a beneficiary notice is in force, the unitholders are considered to be owners of any land held on behalf of the trust. If that land includes land that is occupied by all of the unitholders as their PPR, that land may be eligible to receive an exemption from land tax if:

- the land constitutes the PPR of all unitholders and

- the land would, if it were owned by a natural person, be wholly or partially exempted from land tax on the basis that it is the PPR of all unitholders.

If those conditions are met, the land that is occupied by all of the unitholders as their PPR would be exempt from land tax and will not be included in the assessment of land tax for the trustee or the unitholders.

However, once a notice is withdrawn, the unitholders will no longer be considered owners of the land held on behalf of the trust, and the land will no longer be eligible to receive a PPR exemption on the basis that it is the unitholders’ PPR. Land tax will then be assessed against the land, using the trust rates of land tax.

Assessing unit trusts with notified unitholders

Unit trusts that have a notice of unit holdings in force will be assessed in two stages:

Stage 1 - Assessing the trustee of the unit trust

The trustee of the unit trust will be assessed at the general rates.

All land held by the same trustee for the same trust, including any portion of land held by that trustee on behalf of the same trust, will be aggregated together and land tax will be calculated on the total site value of the land held on behalf of the trust.

Where the trustee owns a portion of a parcel of land on trust, such that it is a joint owner of the land, the trust assessment will include a deduction equal to the trustee’s portion of the land tax assessed under the joint ownership. This deduction will reduce the land tax payable under the trustee’s ownership and, in some cases, the trustee may not have any further land tax liability to pay.

Stage 2 - Assessing the notified unitholders

Each unitholder will be assessed land tax based on their interest in all land they own, including any land held on behalf of a trust in which they are a unitholder.

The unitholder’s assessment will include a deduction equal to their share of the land tax assessed under the trustee’s ownership (Stage 1 above).

If the unitholder does not own any other taxable land, the deduction will reduce the land tax payable to zero and there will be no further land tax liability for the unitholder.

If a unitholder does own other taxable land (unless they in turn are a trustee, see further below), they will be assessed at the general rates on the aggregated value of their proportionate interest in the trust held land (equal to their proportionate share of unitholdings in the trust) and any other taxable land they own. This includes land they own by themselves or jointly with others.

If a notified unitholder is the trustee of another trust, it will be treated as a beneficiary-trustee. This is discussed further below.

Trust deduction

To avoid double taxation, any land tax assessed against the trustee in respect of land held on behalf of the unit trust is to be deducted from land tax assessed against the unitholder(s). The deduction is applied to the total land tax assessed for the unitholder(s) and not just to the land tax assessed for the land subject to the unit trust.

This deduction is equal to the unitholder’s proportionate share of the land tax in the trustee’s assessment.

The deduction will never reduce the amount of land tax assessed against the unitholder below zero.

If, after the trust deduction, a unitholder is not liable for land tax, they will not receive a notice of assessment.

A unitholder can find their deduction on their notice of assessment.

For land tax purposes, a fixed trust is a trust that is not an excluded trust, a discretionary trust or a trust to which a unit trust scheme relates.

The beneficiaries of a fixed trust are fixed, along with their proportional interest in the trust, e.g. a trust for 2 siblings who are each entitled to 50% of the trust fund.

Taxing fixed trusts

A trustee of a fixed trust has 2 options:

- notify RevenueSA of all the beneficial interests in the trust and pay land tax at the general rates of land tax or

- not notify RevenueSA and pay the trust rates of land tax for the trust held land.

Effect of notifying of the beneficial interests

By notifying RevenueSA of the beneficial interests:

- both the beneficiary(ies) and the trustee will be considered owners of the trust held land and

- the trustee will be assessed land tax at general rates of land tax.

Each beneficiary will be treated as if they own a portion of the trust held land equal to their interest in the trust. Land tax will be assessed against the beneficiaries at the general rates of land tax.

The notification of beneficial interests will take effect at the option of the trustee for either the tax year in which the notification is lodged or for the following year.

If there is a change in the beneficiaries while a notification of beneficiaries is in force, the trustee must notify RevenueSA within one month of the change. Failing to notify may give rise to a tax default under the Taxation Administration Act 1996. When this happens, the trustee may be liable for interest and penalty tax on the additional amount of land tax that would have been assessed if the trustee had notified RevenueSA.

The notification will remain in force until the trustee withdraws it. However, once a notification is withdrawn, the trustee cannot lodge another notification and is liable for land tax at the trust rates of land tax.

Unlike discretionary trusts, a beneficiary of a fixed trust cannot withdraw a notice of beneficial interests.

PPR exemption for fixed trusts

In the first instance, land owned by a trustee who is a natural person and which constitutes their PPR may be eligible for a land tax exemption.

If a beneficiary notice is in force, the beneficiaries are considered to be owners of any land held on behalf of the trust. If that land includes land that is occupied by all of the beneficiaries as their PPR, that land may be eligible to receive an exemption from land tax if:

- the land constitutes the PPR of all beneficiaries; and

- the land would, if it were owned by a natural person, be wholly or partially exempted from land tax on the basis that it is the PPR of all beneficiaries.

If those conditions are met, the land that is occupied by all of the beneficiaries as their PPR would be exempt from land tax and will not be included in the assessment of land tax for the trustee or the beneficiaries.

However, once a notice is withdrawn, the beneficiaries will no longer be considered owners of the land held on behalf of the trust, and the land will no longer be eligible to receive a PPR exemption on the basis that it is the beneficiaries’ PPR. Land tax will then be assessed against the land, using the trust rates of land tax.

Assessing fixed trusts with notified beneficial interests

Fixed trusts that have notified RevenueSA of the beneficial interests in the trust are assessed in two stages:

Stage 1 - Assessing the trustee of the fixed trust

The trustee for the land held on fixed trust is assessed at the general rates.

All land held by the same trustee for the same trust will be aggregated together and land tax will be calculated on the total site value of the land held on behalf of the trust.

Where the trustee owns a portion of a parcel of land on trust, such that it is a joint owner of the land, the trust assessment will include a deduction equal to the trustee’s portion of the land tax assessed under the joint ownership. This deduction will reduce the land tax payable under the trustee’s ownership and, in some cases, the trustee may not have any further land tax liability to pay.

Stage 2 - Assessing the notified beneficiary

Each beneficiary will be assessed land tax based on their interest in all land they own, including any land held by a fixed trust that they are beneficiary of.

The beneficiary(ies) will be assessed land tax at the general land tax rates of land tax.

The beneficiary’s assessment will include a deduction equal to their share of the land tax assessed under the trustee’s ownership (Stage 1 above).

If the beneficiary does not own any other taxable land, the deduction will reduce the land tax payable to zero and there will be no further land tax liability to pay by the beneficiary.

If a beneficiary does own other taxable land, they will be assessed at the general rates of land tax on the aggregated value of their proportionate interest in the trust held land and any other taxable land they own. This includes land they own by themselves or jointly with others.

If the notified beneficiary is the trustee of another trust, being either a fixed or unit trust, it will be treated as a beneficiary-trustee. This is discussed further below.

Trust deduction

To avoid double taxation, any land tax assessed against the trustee in respect of land held on behalf of the fixed trust is to be deducted from land tax assessed against the beneficiary(ies). The deduction is applied to the total land tax assessed against the beneficiary(ies) and not just to the land tax assessed for the land subject to the trust.

This deduction is equal to the beneficiary’s proportionate share of the land tax in the trustee’s assessment.

The deduction will never reduce the amount of land tax assessed against the beneficiary below zero.

If, after the trust deduction, a beneficiary is not liable for land tax, they will not receive a notice of assessment.

A beneficiary can find their deduction on their notice of assessment.

Beneficiary-trustees of fixed and unit trusts

Where a beneficiary/unitholder of a fixed/unit trust (but not a discretionary trust) is a trustee of another trust (i.e. a beneficiary-trustee) and a notification has been provided of the beneficial interests/unitholders for the first trust, the beneficiary/unitholder will be assessed land tax in the two stage process discussed above.

Stage 1 - first trust

The trustee of the first trust is liable to land tax at the general rates of land tax.

Stage 2 - second trust is either a fixed trust or unit trust scheme

If the trustee of the second trust (the beneficiary-trustee) does not notify the Commissioner of the beneficial interests/unitholdings of the second trust, the beneficiary-trustee is liable to land tax at the trust rates of land tax. Alternatively, the trustee of the second trust (the beneficiary-trustee) has the option to notify the Commissioner of the beneficial interests/unitholdings of the second trust.

Where the trustee of the second trust elects to lodge a beneficiary notice, the trustee of the second trust will thereby be liable to the general rates of land tax (and not the trust rates of land tax) and the beneficiaries/unitholders of the second trust will be assessed as notified beneficiaries/unitholders.

Stage 2 - second trust is a discretionary trust

However, if the second trust (or any other subsequent trust) beneficiary/unitholder is a trustee of a discretionary trust, the trust rates of land tax will automatically apply to the interest in the land that the trustee of the discretionary trust is deemed to hold.

In this regard, Section 13A(9) requires that to be considered pre-existing trust land the land must has been subject to the trust as at midnight 16 October 2019.

However, rather than the land being subject to the discretionary trust (i.e. the second trust) as at midnight 16 October 2019, the land in this instance was instead subject to the fixed/unit trust (i.e. the first trust) as at midnight 16 October 2019.

Consequently, in assessing the discretionary trust for land tax, the land constitutes subsequent trust land and not pre-existing trust land as the land was not subject to the discretionary trust as at midnight 16 October 2019.

For the avoidance of doubt, a trustee of the discretionary trust can still designate a beneficiary and land that was subject to the discretionary trust itself as at midnight 16 October 2019 will be assessed at the general rates of land tax.

If a discretionary trust has an interest in both (1) pre-existing trust land and (2) subsequent trust land (including an interest in land held by being a beneficiary/unitholder of a fixed/unit trust), the land tax assessed would be calculated by using the same formula outlined above (see ‘Land tax on both pre-existing trust land and subsequent trust land’) that proportionally applies general rates of land tax to pre-existing trust land (for land owned subject to the discretionary trust), and trust rates of land tax to the subsequent trust land (land to the fixed/unit trust as at midnight 16 October 2019).

The following 2 examples illustrate the above.

Example

a unitholder of a unit trust (first trust) is the trustee of a fixed trust (second trust)

ABC Pty Ltd is the trustee of the ABC Unit Trust (i.e. the first trust), and holds land on behalf of that trust. The trust’s only unitholder, Mr Smith, holds these units as the trustee of the Smith Fixed Trust (i.e. the second trust).

Notifications for the first trust (ABC Unit Trust)

ABC Pty Ltd can notify RevenueSA of the unitholder (i.e. Mr Smith) and thereby pay the general rates of land tax and not the trust rates of land tax.

Notifications for the second trust (Smith Fixed Trust)

As Mr Smith is a notified unitholder, he is also considered an owner of the land held by ABC Pty Ltd as trustee for the ABC Unit Trust.

It is then mandatory for Mr Smith to notify RevenueSA that he holds his beneficial interest in the ABC Unit Trust on trust for the Smith Fixed Trust.

Mr Smith can then choose to notify RevenueSA of the beneficiaries in the Smith Fixed Trust.

If Mr Smith notifies RevenueSA of the beneficiaries of the Smith Fixed Trust, it will be assessed at general rates of land tax for its interest in the ABC Unit Trust together with any other land Mr Smith holds on behalf of the Smith Fixed Trust.

If Mr Smith does not notify RevenueSA of the beneficiaries in the Smith Fixed Trust, it will be assessed at the trust rates of land tax for its interest in the ABC Unit Trust together with any other land it holds on trust for the Smith Fixed Trust.

Either way, Mr Smith will receive a deduction for the land tax that ABC Pty Ltd has been assessed on the land that ABC Pty Ltd holds on behalf of the ABC Unit Trust.

Example

a unitholder of a unit trust (first trust) is the trustee of a discretionary trust (second trust)

DEF Pty Ltd is the trustee of the DEF Unit Trust (i.e. the first trust), and holds land on behalf of that trust.

The trust’s only unitholder, Ms Jones, holds the units as the trustee of the Jones Discretionary Trust (i.e. the second trust).

Ms Jones also owns land directly as trustee of the Jones Discretionary Trust.

Notifications for the first trust (DEF Unit Trust)

DEF Pty Ltd can notify RevenueSA of the unitholder (i.e. Ms Jones) and thereby pay the general rates of land tax and not the trust rates of land tax.

DEF Pty Ltd will then be assessed on the trust held land at the general rates of land tax.

Notifications for the second trust (Jones Discretionary Trust)

As Ms Jones is a notified unitholder, she is also considered an owner of the land held by the DEF Unit Trust.

It is then mandatory for Ms Jones to notify RevenueSA that she holds her beneficial interest in the DEF Unit Trust on trust for the Jones Discretionary Trust.

If Ms Jones notifies RevenueSA of a designated beneficiary for the Jones Discretionary Trust:

- the land owned by Ms Jones that was subject to the Jones Discretionary Trust as at midnight 16 October 2019 will be assessed at the general rates of land tax; and

- the land owned by DEF Pty Ltd as trustee of the DEF Unit Trust, for which Ms Jones as trustee of the Jones Discretionary Trust is liable for land tax (by virtue of DEF Pty Ltd giving notice of the unitholders) will automatically be assessed at the trust rates of land tax for its interest in the DEF Unit Trust. As discussed further above, the land was not subject to the Jones Discretionary Trust as at midnight 16 October 2019 (rather it was only subject to the DEF Unit Trust).

If Ms Jones instead does not nominate a designated beneficiary in the Jones Discretionary Trust, Ms Jones will be assessed at the trust rates of land tax for both (i) her interest in the land subject to the DEF Unit Trust and (ii) the land she holds on behalf of the Jones Discretionary Trust.

Either way, Ms Jones will receive a deduction that will reduce the land tax assessed against the land held on behalf of the Jones Discretionary Trust equal to the land tax that DEF Pty Ltd has been assessed on the land it holds on behalf of the DEF Unit Trust.

Excluded trusts

Whilst excluded trusts may have various interests in land arising by way of:

- being the sole owner;

- being a joint owner;

- having beneficial interest(s) in any number of fixed trusts, where a notification of beneficial interest is in force; or

- being a unit holder in any number of unit trusts, where a notification of unit holdings in the trust is in force;

only land of which they are the sole owner will be aggregated for the purposes of assessing land tax at the general rates of land tax (and not the trust rates of land tax). Consequently, an excluded trust will not receive a separate notice of assessment that includes its share of joint holdings.

The following are excluded trusts:

- charitable trusts;

- concessional trusts (e.g. established for a person who has a disability or is subject to a guardianship or administration order);

- a trust the sole beneficiary or beneficiaries of which is or are an association referred to in Section 4(1);

- a trust, for any tax year in relation to which it is a superannuation trust;

- a trust established by a superannuation trust solely for the purposes of an arrangement of a kind authorised under Section 67A of the Commonwealth Superannuation Act;

- a trust that holds child maintenance land. Child maintenance land is land held on trust that was transferred to the trustee for the benefit of a beneficiary as the result of a family breakdown within the meaning of Section 102AGA of the Income Tax Assessment Act 1936 of the Commonwealth; and

- an administration trust.

Excluded trusts: concessional trusts

A concessional trust is:

- a trust of which each beneficiary is—

- a person in respect of whom a guardianship order or an administration order is in force under the Guardianship and Administration Act 1993; or

- a person with a disability within the meaning of the Disability Services Act 1993; or

- a trust created under an order of a court or tribunal, or otherwise created under an Act, for the benefit of a person under disability; or

- a special disability trust (within the meaning of Section 5); or

- a trust of a kind prescribed by the regulations.

Excluded trusts: superannuation trusts

A superannuation trust is, in relation to a financial year, a trust established before the start of the financial year that, in relation to the year of income ending in that financial year, is:

- a complying superannuation fund (within the meaning of Section 42 or 42A of the Superannuation Industry (Supervision) Act 1993 of the Commonwealth (the “Commonwealth Superannuation Act”); or

- a complying approved deposit fund (within the meaning of Section 43 of the Commonwealth Superannuation Act); or

- a pooled superannuation trust (within the meaning of Section 44 of the Commonwealth Superannuation Act).

Example

land held on trust

Land valued above the taxable threshold is owned in equal shares by (1) Ms Jones and (2) Jones Co Pty Ltd as trustee of the Jones Super Fund (the “Super Fund”). Both owners each own other land solely.

The joint owners are assessed together at the general rate of land tax.

Ms Jones will be assessed at the general rates of land tax on her individual interest in the jointly owned land and the other land she owns. Any assessment issued to her will also include a joint ownership deduction.

However, as an excluded trust, the Super Fund’s interest in the joint ownership will not be aggregated for the purposes of assessing land tax. The trustee for the Super Fund will only receive a notice of assessment for the other land it owns solely.

Excluded trusts: administration trusts for deceased estates

An administration trust is a trust under which the assets of a deceased person are held by a personal representative, but only during the period ending on the earlier of:

- the completion of administration of the deceased estate; or

- the third anniversary of the death of the deceased person or a further period (if any) approved by the Commissioner in any particular case.

A trustee of an administration trust must notify RevenueSA within one month after probate has been granted, or letters of administration have been issued, in relation to the deceased estate.

Similarly, the trustee must notify RevenueSA within one month of the completion of the administration of a deceased estate.

Implied, constructive or resulting trusts

An implied, constructive or resulting trust is not intentionally created but is imposed by law or arises in certain circumstances.

A trustee of an implied, constructive or resulting trust will be:

- separately assessed on all trust held land at the general rates of land tax; and

- assessed as if the trust held land was the only land owned by the trustee.

Example 10

land held on trust

Sam owns two parcels of land. Following a dispute between Sam and Alex, a court has ordered that Sam holds one of the parcels of land on trust for Alex.

Accordingly, Sam will be:

- separately assessed on the land held on trust for Alex at the general rates of land tax, as opposed to the trust rates of land tax; and

- assessed as if the trust held land was the only land owned by Sam, such that it will not be assessed together with the other parcel of land Sam owns.

Public unit trust schemes (listed trusts or a widely held trusts)

Trustees of public unit trust schemes being either listed trusts or widely held trusts, will be assessed on the whole of the land subject to the trust at the general rates of and tax (and not the trust rates of land tax) as if the land were the only land owned by them.

A listed trust is a unit trust scheme some or all of the units in which are quoted on a recognised financial market, being a financial market operated by the Australian Securities Exchange Limited or a financial market of a stock exchange prescribed by the Stamp Duties Regulations 2013.

A widely held trust has the same meaning as that term would have in the Stamp Duties Act 1923 if a reference in Section 97(1) of that Act to “300 unitholders” were a reference to “50 unitholders” (in summary, a widely held trust is a unit trust scheme which has not less than 50 unitholders none of whom, individually or together with any associated person, is entitled to more than 20% of the units in the trust).

Testamentary trusts

A testamentary trust arises where property of a deceased person is held by a personal representative or trustee, but only once the personal representative or trustee is actually holding the property. It is generally established as part of a will and is created to hold and safeguard some or all of a deceased person’s assets for the benefit of others.

A testamentary trust may only arise once an administration trust ends (see above for discussion on administration trusts).

A testamentary trust does not qualify as an administration trust, such that it is not capable of being an excluded trust and in the first instance is to be assessed at the trust rates of land tax.

Whether a testamentary trust is a fixed trust or a discretionary trust is dependent on the terms of the particular testamentary trust.

A trustee of a testamentary trust that is a fixed trust (i.e. the beneficiaries are fixed, along with their proportional interest in the trust) can notify RevenueSA of all the beneficiaries of the trust.

The results of notifying are discussed above. In particular, if land constitutes the PPR of all the beneficiary(ies), they may be entitled to exemption from land tax on the land where the requirements are met.

If a testamentary trust is instead a discretionary trust, the trustee may notify RevenueSA of a beneficiary who will be the designated beneficiary of the trust, subject to meeting the various requirements.

Key requirements here include that the land needs to have been subject to the testamentary trust as at midnight on 16 October 2019. RevenueSA also needs to be notified of the designated beneficiary by 30 June 2021 (please refer to the discussion above for further information in this regard).

The results of notifying are discussed above. In particular, if land constitutes the PPR of the designated beneficiary, they may be entitled to an exemption from land tax on the land where the requirements are met.

Related corporations who are trustees

Where a corporation is a trustee, the land held by that corporation as trustee will not be subject to the related corporation provisions found in Part 3, Division 6, “Grouping of Related Corporations”. Instead, the land will be assessed in accordance with the trust provisions as discussed above.

There is one exception to the above though, which is discussed below.

Part 3, Division 6 provides for corporations to be related corporations in certain circumstances.

Where two or more corporations that own land are related corporations, they are to be jointly assessed for land tax on the land as if it were owned by a single corporation. The general rates of land tax will also apply, as opposed to the trust rates of land tax.

For fixed or unit trusts with a corporation as trustee, Section 13G(5) provides that corporations are related corporations if one of the corporations (corporation 1) is the trustee of a fixed trust or a unit trust scheme (the trust) and another corporation (corporation 2) owns, or other related corporations between them own, more than 50% of—

- the total beneficial interests in land subject to the fixed trust; or

- the total number of units held by the unit holders in the unit trust scheme.

Section 13G(5) will apply to land owned by:

- corporation 1 as trustee of the trust; and

- corporation 2 in its own right and not solely as trustee of a trust (discussed further below).

Where Section 13G(5) applies and there are two or more related corporations that both own land that are to be jointly assessed for land tax on the land pursuant to Section 13J, the corporate trustee cannot give notice of the unitholders/beneficiaries of the trust.

In this regard, Section 13G(5) expressly provides that where the provision is enlivened, such corporations are related corporations. If Section 11 (and the further ability to give notice of the unitholders/beneficiaries of the trust pursuant to Sections 12 and 13) were to instead apply, such that land owned by a trustee of a trust was instead to be assessed separately and not aggregated and assessed pursuant to Division 6, then the express inclusion of Section 13G(5) (so as to provide that corporations are related corporations in such circumstances) would be rendered ineffective.

Sections 13J(5) to (11) however set out the means by which a related corporation can be exempted from the application of Division 6.

However, where corporation 2 owns land as trustee of a trust, Section 11 will apply to any land corporation 2 owns as trustee of a trust, such that the land will not be included in the joint assessment for land tax.

If there is only one related corporation that owns land, land tax cannot be assessed pursuant to Section 13J.

As such, where Section 13G(5) applies and a corporation that owns land is not a related corporation of any other corporation that owns land, it will not be assessed for land tax pursuant to Section 13J, and instead only the owner of the land will be assessed (either at the general rates of land tax or at the trust rates of land tax where the land is owned subject to a trust). Please refer to the related corporations information for further information regarding related corporations.

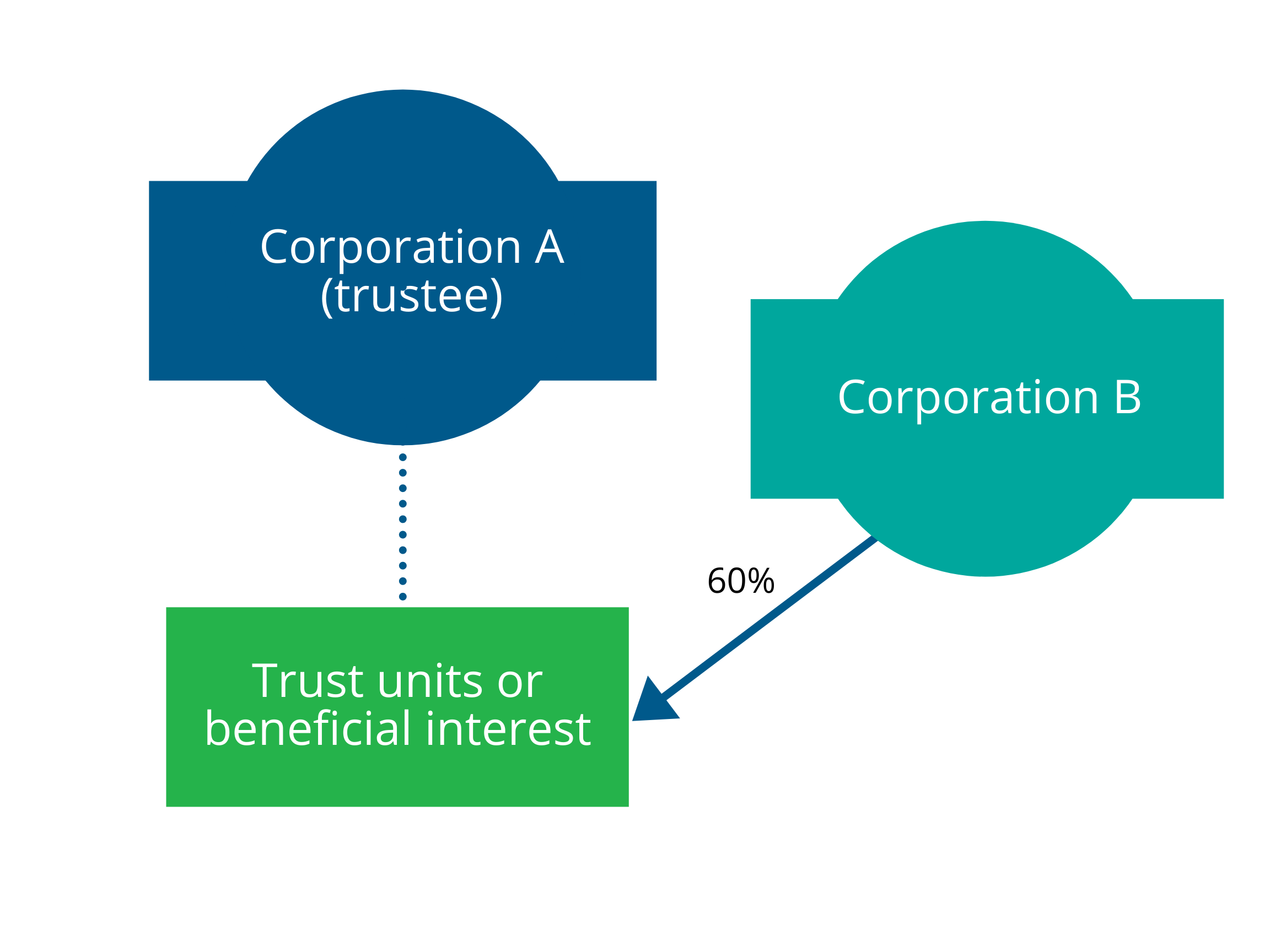

Example 11

Corporation A is the trustee of a unit trust scheme.

Corporation B owns 60% of the units in the unit trust scheme.

Neither Corporation A or Corporation B are related corporations of any other corporation.

As Corporation B owns more than 50% of the total number of units held by the unitholders in the unit trust scheme, Corporation A and Corporation B are related corporations.

If both corporations own land, with Corporation A owning land as trustee of the trust and Corporation B owning land in its own right, they are to be jointly assessed for land tax at the general rates of land tax on the land as if it were owned by a single corporation.

However, if only one of the corporations owns land, the land would not be jointly assessed for land tax.

If only Corporation A owned land, unless a notice of beneficial interest(s)/unitholding(s) or a designated beneficiary is in place, as Corporation A owns the land as trustee of a trust, it would be assessed for land tax at the trust rates of land tax and not the general rates of land tax.

If only Corporation B owned land, Section 13J would not apply and they would not be jointly assessed for land tax.

Impact of notification of beneficiaries outside of the Act

Where the Act provides for a beneficiary or unitholder to be an owner of the land for the purposes of the Act (i.e. where they are a notified beneficiary/unitholder or designated beneficiary), the extent by which they are taken to own land as a result is limited to the Act only.

For example, the beneficiary or unitholder will not be taken to have:

- been conveyed or transferred an interest in land for the purposes of the Stamp Duties Act 1923, such that a liability to stamp duty arises; or

- a relevant interest in residential property for the purposes of the First Home and Housing Construction Grants Act 2000, such that they will remain eligible for a grant where the eligibility requirements are met; or

- become an owner of the land such that there are Federal taxation, benefit or other consequences.