Guides to Legislation do not have the force of law.

This is a general guide to the Land Tax Act 1936 for related corporations.

This document should not be read in isolation to the legislation and does not in any way override the Land Tax Act 1936.

In this Guide:

- all references made to Sections, Parts or Divisions relate to the Land Tax Act 1936 unless otherwise specified.

- a reference to the Commissioner is a reference to the Commissioner of State Taxation.

We hope you find this Guide to be helpful and we would certainly welcome any comments or suggestions that would help us to improve it.

For further details on any matters relating to the Acts mentioned in this Guide, please feel free to contact RevenueSA on (08) 8226 3750 (select option 2).

Commissioner of State Taxation

9 July 2021

Part 3, Division 6 “Grouping of Related Corporations” of the Land Tax Act 1936 provides for corporations to be related corporations in certain circumstances.

Where 2 or more corporations that own land are related corporations, they are to be jointly assessed for land tax on the land as if it were owned by a single corporation.

A corporation may have various interests in land arising by way of:

- being the sole owner;

- being a joint owner;

- having beneficial interest(s) in any number of fixed trusts, where a notification of beneficial interest is in force; or

- being a unitholder in any number of unit trusts, where a notification of unit holdings in the trust is in force.

Land that is or exempt from land tax under the Land Tax Act 1936 is not liable to land tax. Accordingly, land that is exempted from land tax will not be included in the taxable value of land in an assessment of a land tax liability.

The following discussion therefore proceeds on the basis that any land exempted from land tax will not be included in any assessment of a land tax liability.

Sections 13G and 13I set out the circumstances in which corporations are related to each other. The different means by which corporations are grouped are discussed further below.

Subject to Section 13G(5) (discussed further below), Section 11 operates such that where a corporation is the owner of land as trustee of a trust (other than a trust arising because of a contract to purchase or acquire an estate or interest in the land), the trustee will instead be assessed for land tax on the whole of the land subject to the trust as if the land were the only land owned by the trustee.

This means that where an interest in land is held on trust, the taxable value of the interest in that land:

- will be aggregated with the taxable value of other land held by the same owner that is subject to the same trust; but

- will not be aggregated with the taxable value of other land owned by the same taxpayer and not subject to the same trust.

Section 11 only applies where the land is directly owned by the trustee (discussed further below).

Land owned by a corporation as trustee of a trust is liable for land tax at the trust rates and will be subject to the trust provisions, except where Section 13G(5) applies (discussed further below).

See the Guide to Legislation: Land Tax - land held on trust for more detailed information.

Example 1

A Pty Ltd and B Pty Ltd are related corporations as a result of having the same shareholders.

A Pty Ltd owns land as trustee of a trust.

B Pty Ltd owns land in its own right.

Pursuant to Section 11, the land owned by A Pty Ltd as trustee of a trust will not be aggregated with the land held by B Pty Ltd under the grouping provisions.

As A Pty Ltd holds land as trustee of a trust, it will be liable for land tax at the trust land tax rates unless subject to meeting the necessary requirements, the trustee chooses to give notice of its beneficiaries/unit holders, in which case it will be liable to the general land tax rates.

Section 13J(1) provides that related corporations that own land are to be jointly assessed for land tax on the land as if it were owned by a single corporation.

In this regard, Section 13J(1) requires that there needs to be 2 or more related corporations that own land in order for the section to apply.

As such, Section 13J will not apply where only one related corporation owns land.

Example 2

Corporation A and Corporation B are related corporations.

Corporation A owns land as trustee of a trust.

Corporation B owns no land.

Division 6 does not apply in this instance as:

- only one corporation, Corporation A, owns land; and

- in any event, Corporation A is to be assessed separately on the land it owns as trustee of the trust in accordance with Section 11.

Section 13G(2) provides that 2 corporations are related to each other if one of those corporations:

- controls the composition of the board of the other corporation; or

- is in a position to cast, or control the casting of, more than 50% of the maximum number of votes that might be cast at a general meeting of the other corporation; or

- holds more than 50% of the issued share capital of the other corporation.

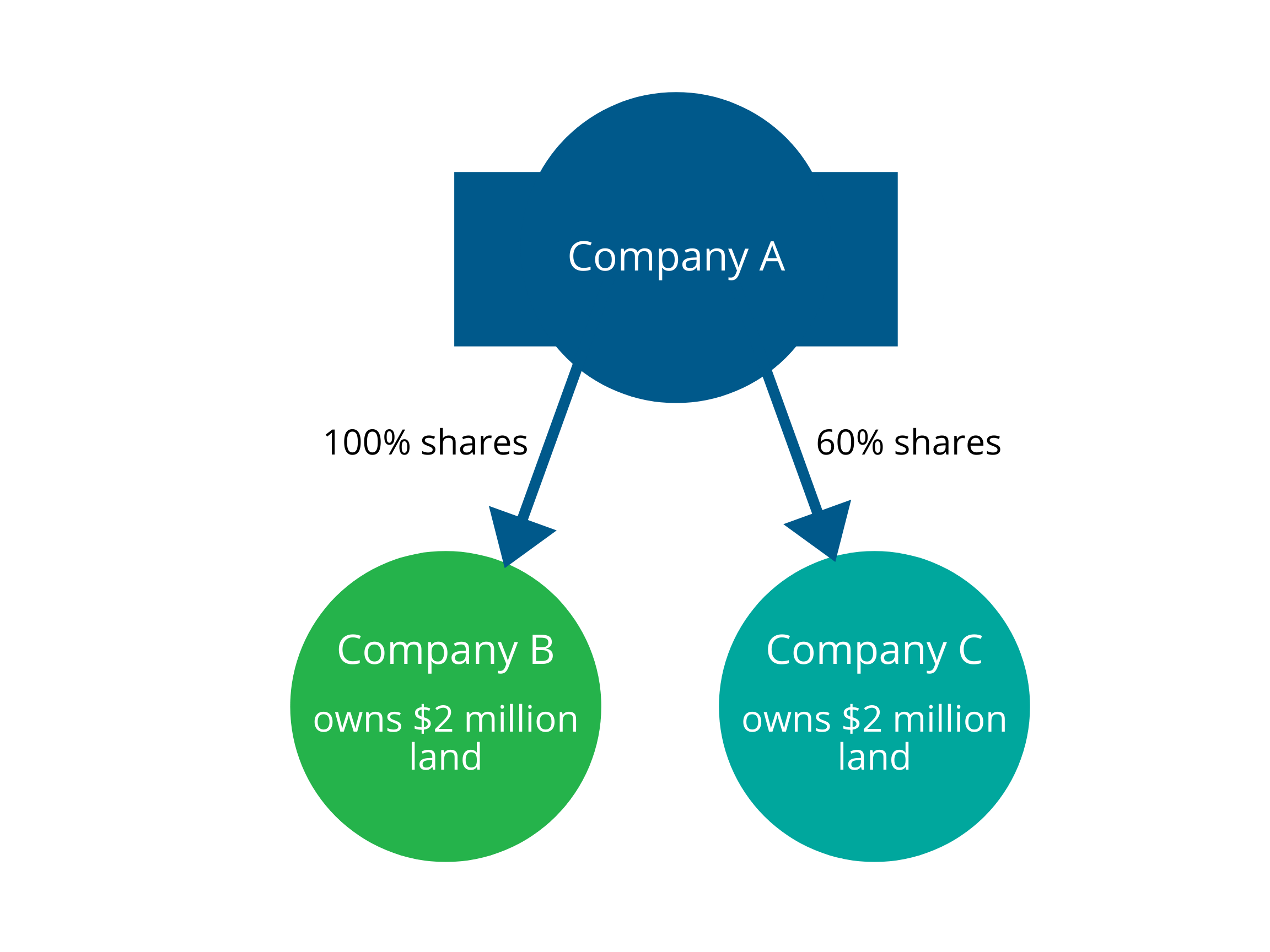

Example 3

Company A is a holding company, which owns 100% of the shares in Company B. Company B owns $2 million in land.

Company A also owns 60% of the shares in Company C.

Company C owns $2 million in land.

Companies A, B and C are related corporations and will be grouped for land tax purposes.

Companies B and C will be jointly assessed on the aggregated site value of all of the land that these corporations own (that is, $4 million).

Section 13G(3) provides that corporations are related if a person (including a corporation) has, or persons (including corporations) have together, a controlling interest in each of the corporations.

Section 13H provides that a person has, or persons have together, a controlling interest in a corporation if:

- that person, or those persons acting together, can control the composition of the board of the corporation; or

- that person is, or those persons acting together are, in a position to cast or control the casting of more than 50% of the maximum number of votes that might be cast at a general meeting of the corporation; or

- that person holds, or those persons acting together hold, more than 50% of the issued share capital of the corporation.

A person does not need to have a controlling interest in 2 corporations by the same means for a group to exist.

For example, if a shareholder of one corporation is able to cast more than 50% of the votes at a general meeting of the corporation, and that shareholder also owns more than 50% of the issued share capital of another corporation, the 2 corporations are related because the shareholder has a controlling interest in both corporations.

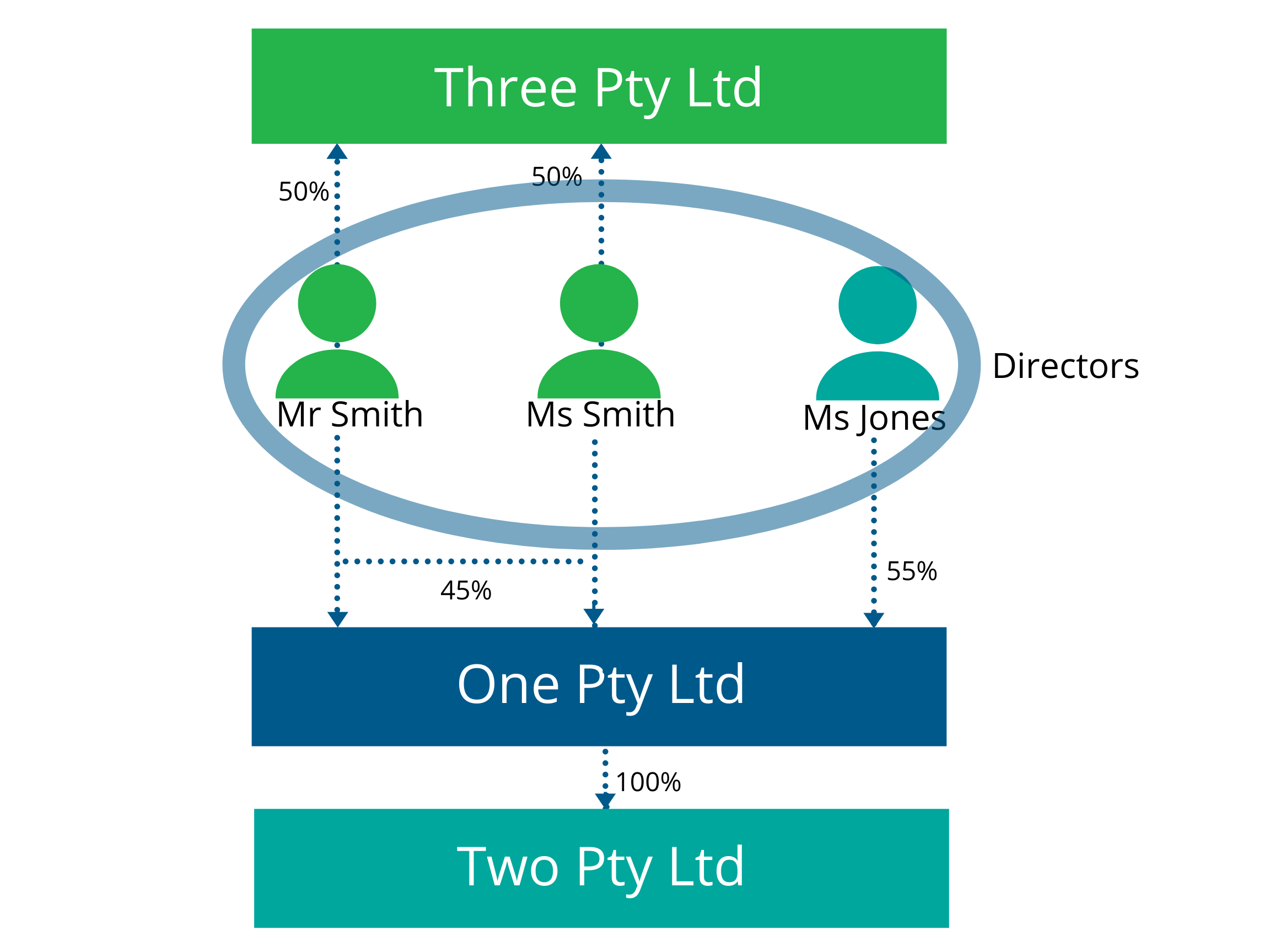

Example 4

Mr Smith and Ms Smith are 2 of the 3 directors of One Pty Ltd (66.66%). Mr Smith and Ms Smith together own 45% of the shares in One Pty Ltd, with the third director, Ms Jones, owning the remaining 55% of the shares.

One Pty Ltd and Two Pty Ltd are related corporations pursuant to Section 13G(2)(c) (discussed above) as One Pty Ltd holds more than 50% of the issued share capital of Two Pty Ltd (that is, One Pty Ltd owns 100% of the shares in Two Pty Ltd).

Mr Smith and Ms Smith control Three Pty Ltd pursuant to Section 13H(c) as together they own more than 50% of the shares in Three Pty Ltd (that is, together they own 100% of the shares).

Mr Smith and Ms Smith also control Two Pty Ltd pursuant to Section 13H(b), by virtue of them being the majority of directors in One Pty Ltd, such that they are in a position to control the casting of more than 50% of the maximum number of votes that might be cast at a general meeting of Two Pty Ltd.

Accordingly, pursuant to Section 13G(3), Two Pty Ltd and Three Pty Ltd are related corporations as the same persons, being Mr Smith and Ms Smith, have together a controlling interest in each of the corporations.

Two Pty Ltd and Three Pty Ltd will be jointly assessed on the aggregated site value of all of the land that these corporations own.

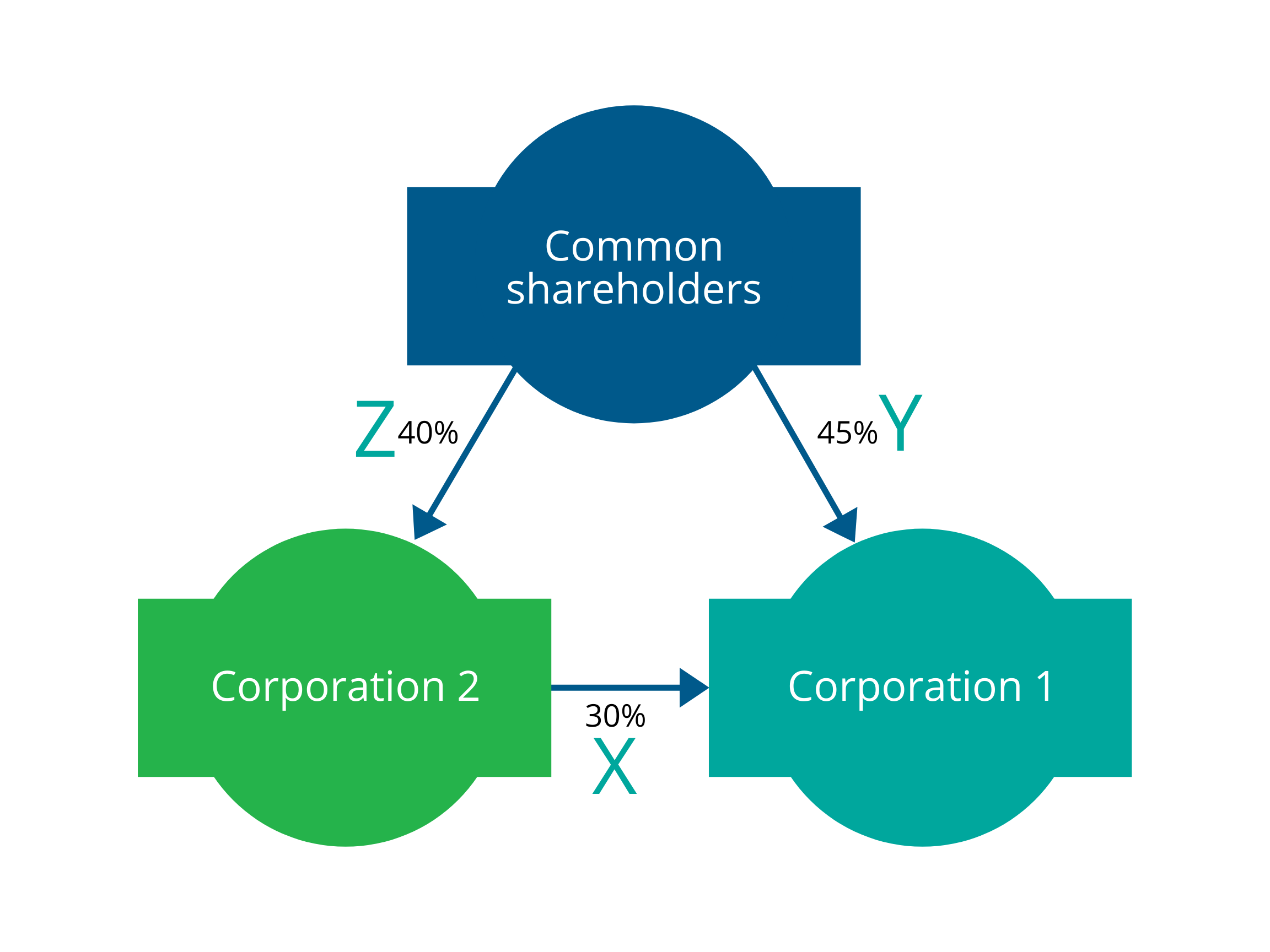

Section 13G(4) provides that corporations are related corporations if:

- more than 50% of the issued share capital of 1 of those corporations (corporation 1) is held by the other corporation (corporation 2) together with the shareholders of corporation 2; and

- the percentage of the issued share capital of corporation 2 held by shareholders of corporation 1 is more than the difference between 50% and the percentage of the issued share capital of corporation 1 held by corporation 2.

The corporations will be related where the following conditions are satisfied:

X + Y > 50% and Z > 50% – X.

where:

X is the shareholding in corporation 1 held by corporation 2 expressed as a percentage.

Y is the shareholding in corporation 1 held by the shareholders common to both corporations expressed as a percentage.

Z is the shareholding in corporation 2 held by the shareholders common to both corporations expressed as a percentage.

Example 5

Corporation 2 owns 30% of the share capital of Corporation 1 (X).

Shareholders of Corporation 2 own 45% of the share capital of Corporation 1 (Y).

Shareholders of Corporation 2 own 40% of Corporation 2’s share capital (Z).

30% (X) + 45% (Y), being 75%, is greater than 50%.

40% (Z) is greater than 50% less 30% (X), being 20%.

Therefore, Corporation 1 and Corporation 2 are related corporations.

Section 13G(5) provides that corporations are related if one of the corporations (corporation 1) is the trustee of a fixed trust or a unit trust scheme (the trust) and another corporation (corporation 2) owns, or other related corporations between them own, more than 50% of—

- the total beneficial interests in land subject to the fixed trust; or

- the total number of units held by the unit holders in the unit trust scheme.

Section 13G(5) will apply to land owned by:

- corporation 1 as trustee of the trust; and

- corporation 2 in its own right and not solely as trustee of a trust (discussed further below).

Where Section 13G(5) applies and there are 2 or more related corporations that both own land that are to be jointly assessed for land tax on the land pursuant to Section 13J, the corporate trustee cannot give notice of the unitholders/beneficiaries of the trust.

In this regard, Section 13G(5) expressly provides that where the provision is enlivened, such corporations are related corporations.

If Section 11 (and the further ability to give notice of the unitholders/ beneficiaries of the trust pursuant to Sections 12 and 13) were to instead apply, such that land owned by a trustee of a trust was instead to be assessed separately and not aggregated and assessed pursuant to Division 6, then the express inclusion of Section 13G(5) (so as to provide that corporations are related corporations in such circumstances) would be rendered ineffective.

Sections 13J(5) to (11) however set out the means by which a related corporation can be exempted from the application of Division 6.

However, where corporation 2 owns land as trustee of a trust, Section 11 will apply to any land corporation 2 owns as trustee of a trust, such that the land will not be included in the joint assessment for land tax.

In addition, as discussed above, if there is only one of any number of related corporations that owns land, land tax cannot be assessed pursuant to Section 13J.

As such, where Section 13G(5) applies and a corporation that owns land is not a related corporation of any other corporation that owns land, it will not be assessed for land tax pursuant to Section 13J, and instead only the owner of the land will be assessed.

Example 6

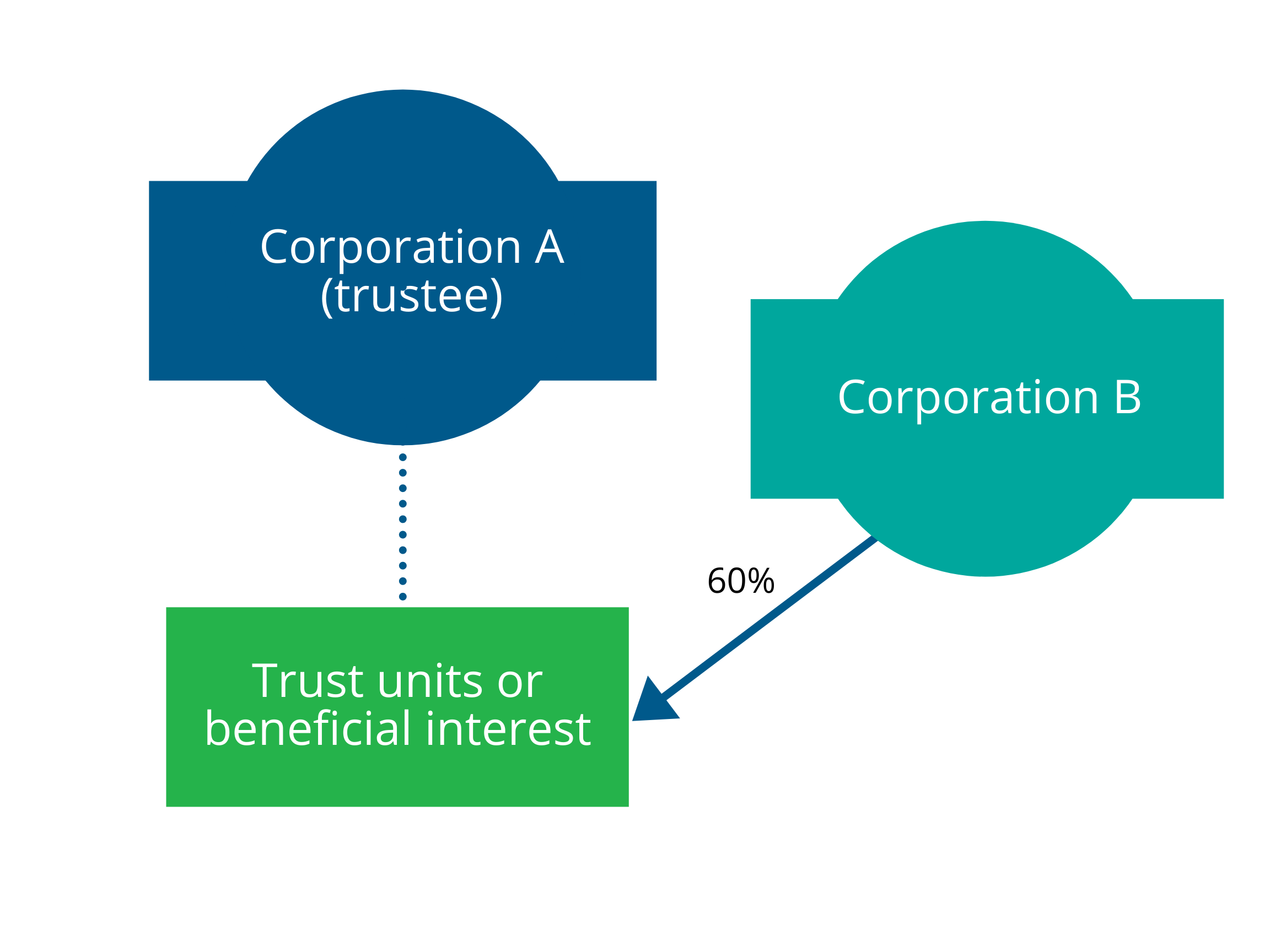

Corporation A is the trustee of a unit trust scheme.

Corporation B owns 60% of the units in the unit trust scheme.

Neither Corporation A or Corporation B are related corporations of any other corporation.

As Corporation B owns more than 50% the total number of units held by the unit holders in the unit trust scheme, Corporation A and Corporation B are related corporations.

If both Corporation A and Corporation B own land, with Corporation A owning land as trustee of the trust and Corporation B owning land in its own right, Section 13J would apply and they would be jointly assessed for land tax on the land.

If only Corporation A owned land as trustee of a trust, Section 13J would not apply and they would not be jointly assessed for land tax. Instead, as Corporation A owns the land as trustee of a trust, it would be liable to the trust land tax rates (unless a notice of beneficial interest(s)/unit holdings is in place – refer to the land held on trust information for further information on this).

If only Corporation B owned land, Section 13J would not apply and they would not be jointly assessed for land tax. Corporation B would instead be liable to the general land tax rates (assuming it did not the land as trustee of a trust).

One corporation is related to another corporation and that second corporation is, in turn, related to a third corporation, the first corporation and the third corporation will also be related. Therefore, all three corporations will be taken to be related.

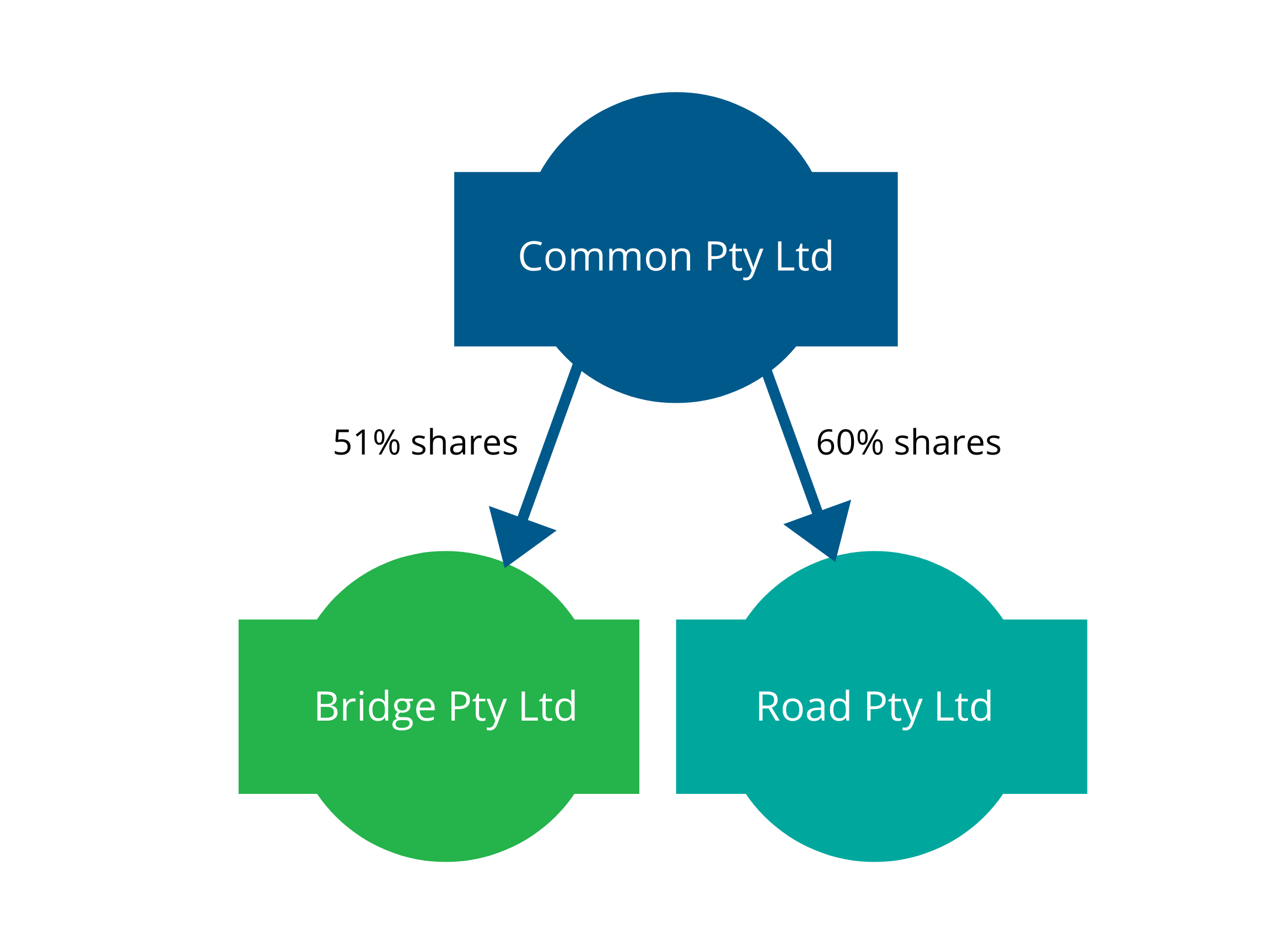

Example 7

Bridge Pty Ltd forms a group with Common Pty Ltd because Common Pty Ltd holds more than 50% of the issued capital of Bridge Pty Ltd.

For the same reason, Common Pty Ltd forms a group with Road Pty Ltd.

Therefore Bridge Pty Ltd, Common Pty Ltd and Road Pty Ltd form one group as Common Pty Ltd is a common member of both groups.

Under Section 13I(1)(g), if a trustee holds controlling interests in 2 or more corporations on behalf of different trusts, those corporations are not related to each other only because of that control.

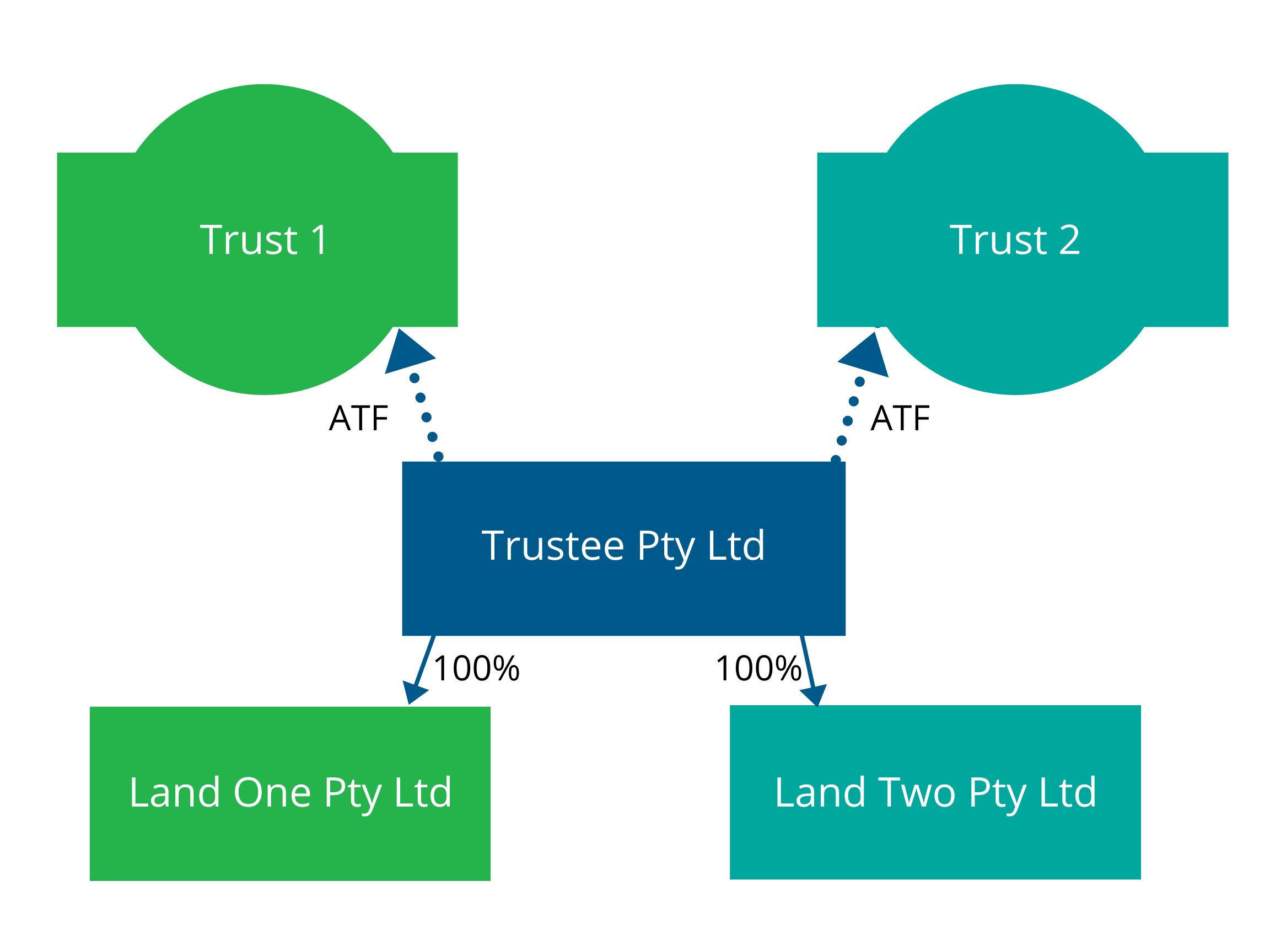

Example 8

Trustee Pty Ltd is a trustee corporation for various trusts. Its shareholders and directors do not own shares in, nor are they directors of, other corporations. Trustee Pty Ltd only owns shares in corporations on trust (in other words, it does not own shares in corporations in its own right).

Amongst other things, Trustee Pty Ltd holds a controlling interest in 2 corporations, Land One Pty Ltd and Land Two Pty Ltd (for example, Trustee Pty Ltd (i) owns all of the shares in both corporations, and (ii) controls the composition of the boards of both corporations), on behalf of different trusts, being Trust 1 and Trust 2.

The 2 corporations are not related corporations of each other only because of Trustee Pty Ltd’s controlling interest in both corporations.

The same would equally apply if Trustee Pty Ltd was instead a natural person trustee, as opposed to a corporate trustee.

Company A, is a beneficiary/unitholder of a fixed trust/unit trust. It is also a related corporation of Company B. Both corporations own land.

If the trustee of the trust gives notification of the beneficial interests/unitholdings:

- the trustee of the trust will not be subject to the trust land tax rates; and

- as a notified beneficiary/unitholder, Company A will be deemed to own the trust land.

As Company A and Company B are related corporations, the land owned by the 2 related corporations is to be jointly assessed for land tax on the land as if it were owned by a single corporation.

Both corporations will also be jointly and severally liable for the land tax.

Under Section 13I(1)(a), corporations may be related corporations whether or not they own land in South Australia. Therefore, 2 corporations that own land in South Australia can be grouped with each other if they are related to a third corporation that does not own land in South Australia.

Under Section 13I(1)(b), a reference to the issued share capital of a corporation does not include shares which carry no right to participate in a distribution of profits or capital beyond a specified amount (that is, preference shares).

Example 9

ABC Pty Ltd has on issue the following 2 classes of shares:

- 100 ordinary shares; and

- 100 preference shares which carry no right to participate in a distribution of profits beyond a specified amount.

In considering the issued share capital of ABC Pty Ltd (for example, whether shareholders have a controlling interest in ABC Pty Ltd), the preference shares are not included.

Under Section 13I(1)(c), any shares held or power exercisable by a person or corporation as a trustee or nominee for another person or corporation are taken to be also held or exercisable by the other person or corporation.

In terms of shares held or power exercisable by a natural person or corporation as a trustee for another person or corporation, the provision only applies to bare trusts. It does not apply to unit and discretionary trusts. As such, in terms of trusts, only the beneficiary(ies) of a bare trust will, in addition to the trustee, be taken to hold shares or exercise power in determining whether corporations are related corporations.

Example 10

Fred, as trustee, owns shares in Flintstone Pty Ltd as bare trustee (being a type of fixed trust) for Wilma, being the beneficiary.

Both Fred and Wilma are taken to each hold 100% of the shares in Flintstone Pty Ltd.

Under Section 13I(1)(d), any shares held or power exercisable by an excluded trust must be disregarded.

See the Guide to Legislation: Land Tax - land held on trust for more detailed information.

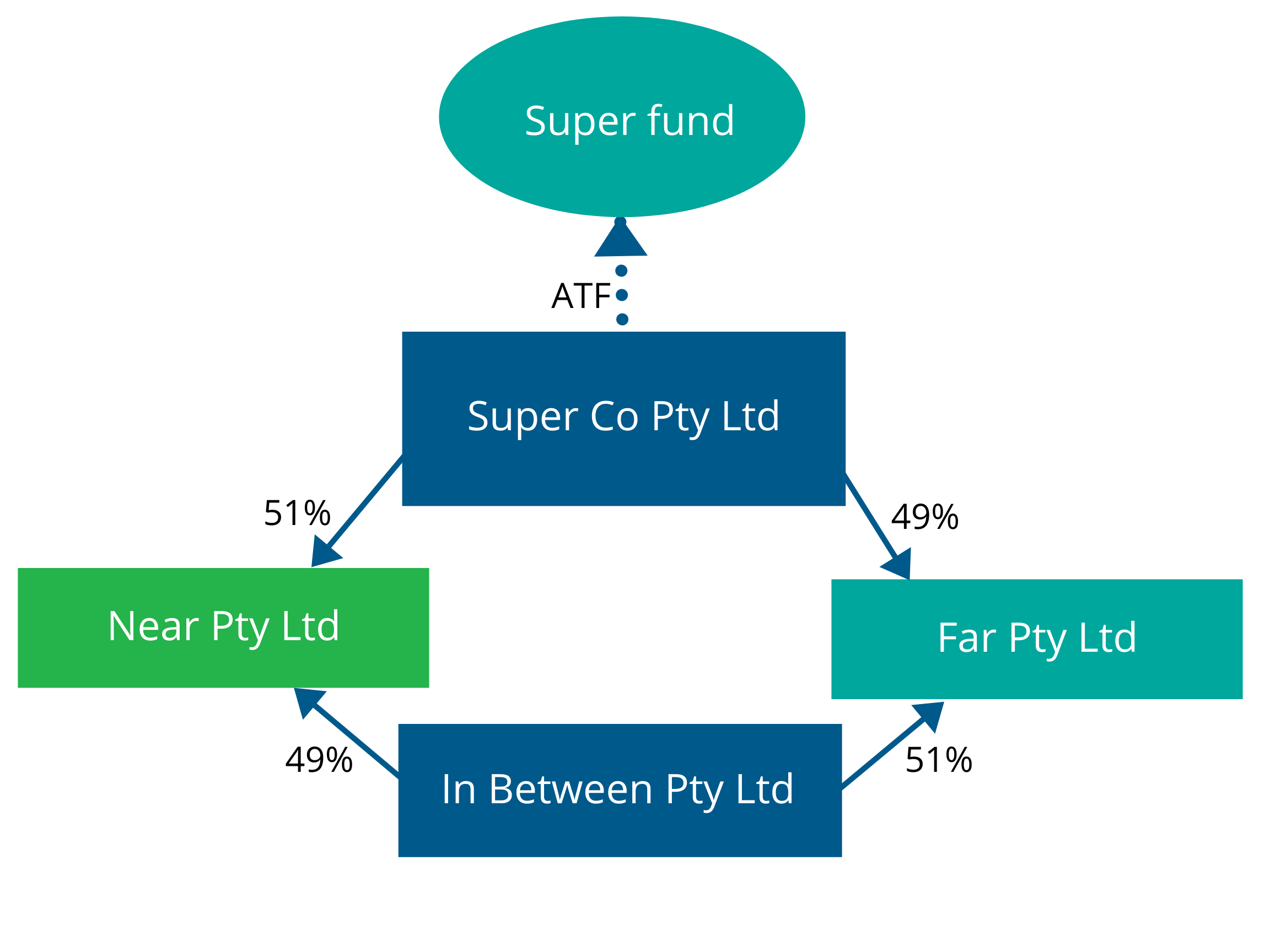

Example 11

A superannuation trust is a type of excluded trust.

Super Co Pty Ltd is the trustee of a superannuation trust, the Super fund.

As trustee of the Super fund, Super Co Pty Ltd owns shares in the following corporations which own land:

- 51% of the shares in Near Pty Ltd; and

- 49% of the shares in Far Pty Ltd.

The remaining shares in both corporations are held by In Between Pty Ltd, that is, 49% of Near Pty Ltd and 51% of Far Pty Ltd. In Between Pty Ltd does not own any land.

Near Pty Ltd and Far Pty Ltd might ordinarily be related corporations as a set of persons (that is, Super Co Pty Ltd and In Between Pty Ltd) has a controlling interest in both.

However, because the shares held and powers exercisable by Super Co Pty Ltd as trustee of the Super fund are disregarded due to it being an excluded trust, Near Pty Ltd and Far Pty Ltd are not related corporations. In this regard:

- no set of persons (that is, Super Co Pty Ltd and In Between Pty Ltd) has a controlling interest in each of the corporations, with Super Co Pty Ltd’s interest disregarded; and

- In Between Pty Ltd’s remaining interests of 49% of Near Pty Ltd and 51% of Far Pty Ltd remain unchanged (49% and 51% respectively) and do not consequently increase to 100% in both so as to give it a controlling interest in both entities.

Under Section 13I(1)(e), any shares held or power exercisable by virtue of a debenture, or a trust deed for securing the issue of debentures, must be disregarded.

Under Section 13I(1)(f), where shares in a company are used as security for a loan from a person who conducts a money lending business, the grouping provisions do not apply unless the money lender who obtains the security interest in the shares is associated with that company for example, as a director, secretary or related company if the money lender is a company.

Section 13I(1)(g) is discussed above.

Under Section 13I(1)(h), the composition of a corporation’s board is taken to be controlled by a person or another corporation if the person or other corporation, by the exercise of a power exercisable whether or not with the consent or concurrence of any other person, can appoint or remove all or a majority of the members of the board.

It is to be noted that Section 11 only applies where the land is directly owned by a trustee.

As such, Section 11 does not apply where a trustee owns shares in a corporation and that corporation in turn owns land (that is, Section 11 does not apply where a trustee indirectly owns land).

Under Section 13I(1)(e), any shares held or power exercisable by virtue of a debenture, or a trust deed for securing the issue of debentures, must be disregarded.

Under Section 13I(1)(f), where shares in a company are used as security for a loan from a person who conducts a money lending business, the grouping provisions do not apply unless the money lender who obtains the security interest in the shares is associated with that company for example, as a director, secretary or related company if the money lender is a company.

Section 13I(1)(g) is discussed above.

Under Section 13I(1)(h), the composition of a corporation’s board is taken to be controlled by a person or another corporation if the person or other corporation, by the exercise of a power exercisable whether or not with the consent or concurrence of any other person, can appoint or remove all or a majority of the members of the board.

Section 11 only applies to land owned by a trustee of a trust

It is to be noted that Section 11 only applies where the land is directly owned by a trustee.

As such, Section 11 does not apply where a trustee owns shares in a corporation and that corporation in turn owns land (that is, Section 11 does not apply where a trustee indirectly owns land).

Example 12

Alex owns all of the shares in One Pty Ltd. One Pty Ltd is the trustee of the Alex Family Trust.

Alex has a controlling interest in One Pty Ltd pursuant to Section 13H(c).

One Pty Ltd does not own land in its own right. It instead owns 100% of the shares in Two Pty Ltd which in turn owns land.

One Pty Ltd and Two Pty Ltd are related corporations pursuant to Section 13G(2)(c).

Section 11 does not apply as the trustee, One Pty Ltd, does not own land as trustee of a trust (i.e. it instead owns shares in a corporation that owns land).Alex also owns all of the shares in Three Pty Ltd which owns land in its own right.

Alex also owns all of the shares in Three Pty Ltd which owns land in its own right.

Alex has a controlling interest in Three Pty Ltd pursuant to Section 13H(c).

Pursuant to Section 13G(3), One Pty Ltd and Three Pty Ltd are related corporations as the same person, Alex, has a controlling interest in each of the corporations.

Pursuant to Section 13G(6), all three companies form a group as Two Pty Ltd and Three Pty Ltd are both related to One Pty Ltd.

Two Pty Ltd and Three Pty Ltd would be jointly assessed on the aggregated site value of all of the land that the 2 corporations own.

Under Section 13J(3), the Commissioner of State Taxation (the “Commissioner”), may issue notices of assessment for land tax:

- to the related corporations jointly; or

- to the related corporations separately; or

- to any 2 or more of the related corporations jointly and the remainder separately.

Where related corporations are jointly assessed for land tax and one notice of assessment is issued to one of the related corporations, pursuant to Section 17(1), the burden of the tax is to be distributed between the related corporations in the relative proportions of the value of their interests in the land taxed.

Pursuant to Section 17(2), a related corporation who has paid tax in respect of land is entitled to recover from every other related corporation in respect of the same land a proper proportion of the amount paid.

RevenueSA will issue one notice of assessment to the postal address of one of the related corporations.

In the first instance, the related corporation most recently incorporated will be selected as the recipient corporation of the related corporations notice.

However, related corporations can change the postal address that the notice is issued to by contacting RevenueSA.

The notice will specify each land owning related corporation, the land owned by the related corporations and the land tax assessed against each parcel of land.

Under Section 13J(5), a corporation that is a related corporation of another corporation may apply to the Commissioner to be exempted from being a related corporation and to instead be treated as a single corporation for the purposes of assessment of land tax in relation to land held by the corporation.

Under Section 13J(6), the Commissioner may only grant an application if the Commissioner is satisfied:

- that the land is being held for the purpose of being developed as a residential development of more than 10 allotments or lots; and

- as to any other matters prescribed by the regulations.

The land, which can comprise one or more parcels of land (which, in totality, must be subdivided into more than 10 allotments or lots), must be held by the one corporation, as opposed to being held by multiple related corporations.

Under Section 13J(7), an exemption granted on an application will be for an initial term specified by the Commissioner in the instrument of exemption (which will be based on the expected development period but may not exceed a period of 5 years).

Under Section 13J(8) the initial term of an exemption may be extended for a further period if the Commissioner is satisfied that the development of the land is occurring over a reasonable period in the circumstances.

Under Section 13J(9), an exemption will cease if the Commissioner determines that:

- the development has been substantially completed; or

- the development has not been substantially commenced within the period of 2 years after the grant of the application (or such longer period as the Commissioner may allow).

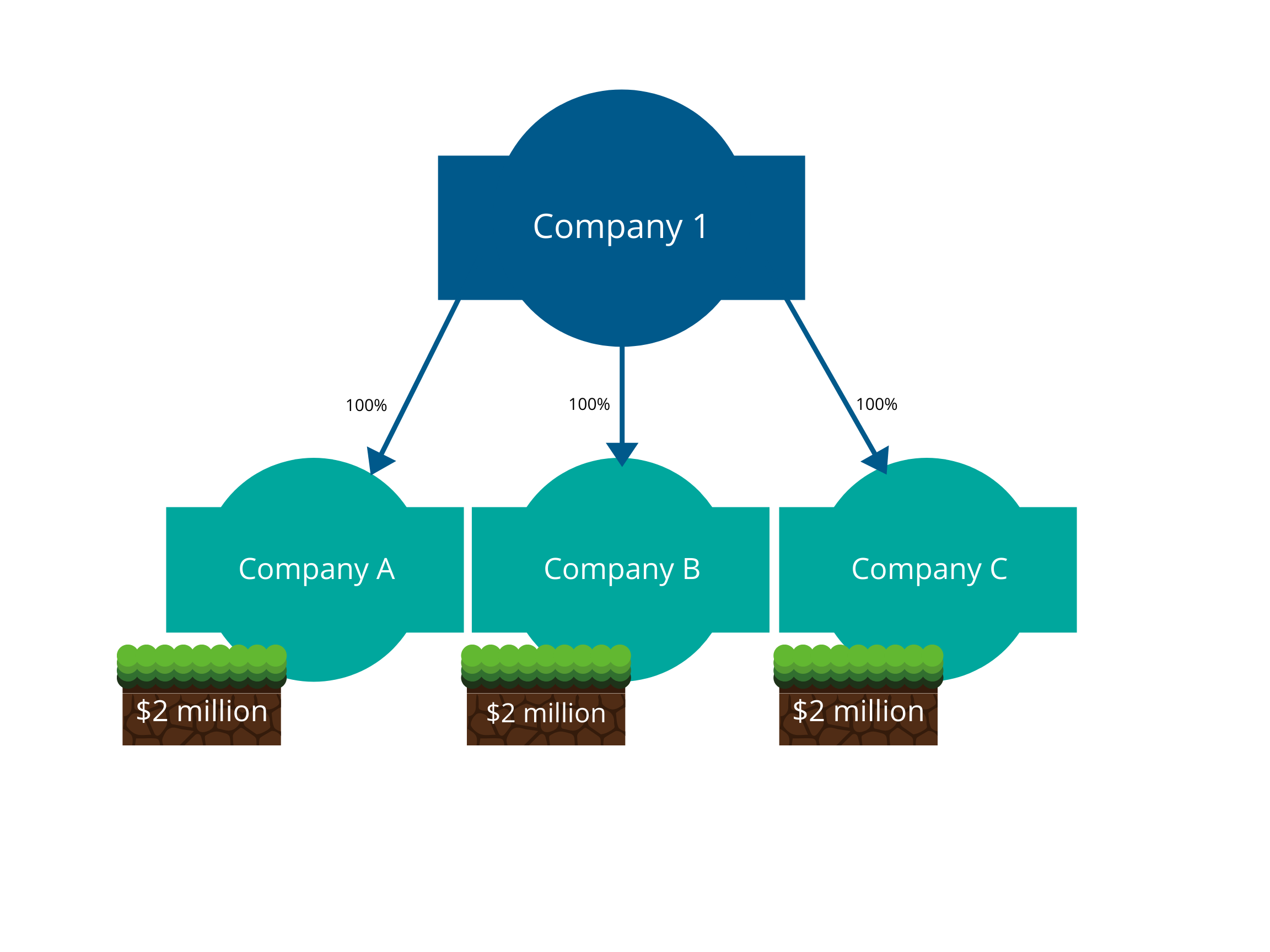

Example 13

Company 1 is a property developer. Company 1 owns 100% of the shares of three other subsidiary companies. These three companies each own a single parcel of land with a site value of $2 million each.

The land held by one of these companies, land C, is intended for a residential development with more than 10 allotments. Land B and A are not intended for residential development.

Company 1 and its subsidiary companies will be treated as related corporations and all would in the first instance be grouped for land tax purposes.

However, land C is being held for an eligible residential development. Company C therefore makes an application to be exempted from related corporation grouping, which is approved.

Company 1 will be grouped with Companies A and B and will be jointly assessed on the $4 million aggregated site value of land A and B.

Company C will only be assessed on the $2 million site value of land C.

Further information

Online versions of state legislation are available at the South Australian legislation website at legislation.sa.gov.au.

See the related corporations page for more information.

Versions history

| Version | Date issued | Changes made |

|---|---|---|

| 1 | 9 July 2021 | first release |

| 2 | 1 September 2022 | Updated to add text missing from example 12 |

View PDF of 2020-21 Guide to Legislation: Land Tax - Related Corporations (PDF 442KB)

Previous Guides to Legislation

Contact Us

When contacting us please provide your ownership number and assessment number. You can find these numbers on your Land Tax Assessment (previously known as a Notice of Land Tax Assessment).

| online | complete a land tax assessment query form |

|---|---|

| landtax@sa.gov.au | |

| phone | (08) 8226 3750, select option 2 |

| fax | (08) 8207 2100 |

| post | GPO Box 1647, Adelaide, SA 5001 |

You can reach us during business hours: 8:30am - 5:00pm (South Australian time), Monday to Friday (excluding public holidays).

Do you want to provide feedback or lodge a complaint?

You can do so via our feedback and complaints page.