At the end of each financial year, all taxpayers are required to lodge an annual reconciliation following the end of the financial year to which the annual reconciliation return relates.

The 2019-20 annual reconciliation must be lodged between from Monday, 13 July 2020 to Friday, 14 August 2020.

The annual reconciliation should include details of taxable wages and the various components that make up those wages. Details of any interstate wages are also required for both the taxpayer and any other group members to determine the correct deduction entitlement. The annual reconciliation may result in either further tax being payable or a refund.

The annual reconciliation checklist can be used to prepare the information you need for your annual reconciliation. The annual reconciliation must be submitted electronically via RevenueSA Online at www.revenuesaonline.sa.gov.au.

After entering the South Australian wage components for the 2019-20 annual reconciliation, you will need to provide your organisation's total South Australian wages split into 2 periods:

- 1 July 2019 to 29 February 2020 (period 1)

- 1 March 2020 to 30 June 2020 (period 2)

Wages paid during period 2 may be eligible for a COVID-19 payroll tax relief waiver or deferral.

Eligibility for a waiver or deferral will be based on the Australia Wide (annualised grouped) wages declared in the 2018-19 annual reconciliation lodged by your organisation. Specifically:

- If your organisation’s Australia wide (annualised grouped) wages are up to $4 million, your organisation will be eligible for a waiver of Payroll Tax.

- If your organisation’s Australia wide (annualised grouped) wages are above $4 million, your organisation can request a deferral of Payroll Tax during the annual reconciliation if you have been adversely impacted by COVID-19.

If your organisation has been receiving JobKeeper payments, these will need to be declared as part of the annual reconciliation for reporting purposes only. JobKeeper payments are exempt from Payroll Tax and will not affect your liability.

See the payroll tax COVID-19 relief page for further information.

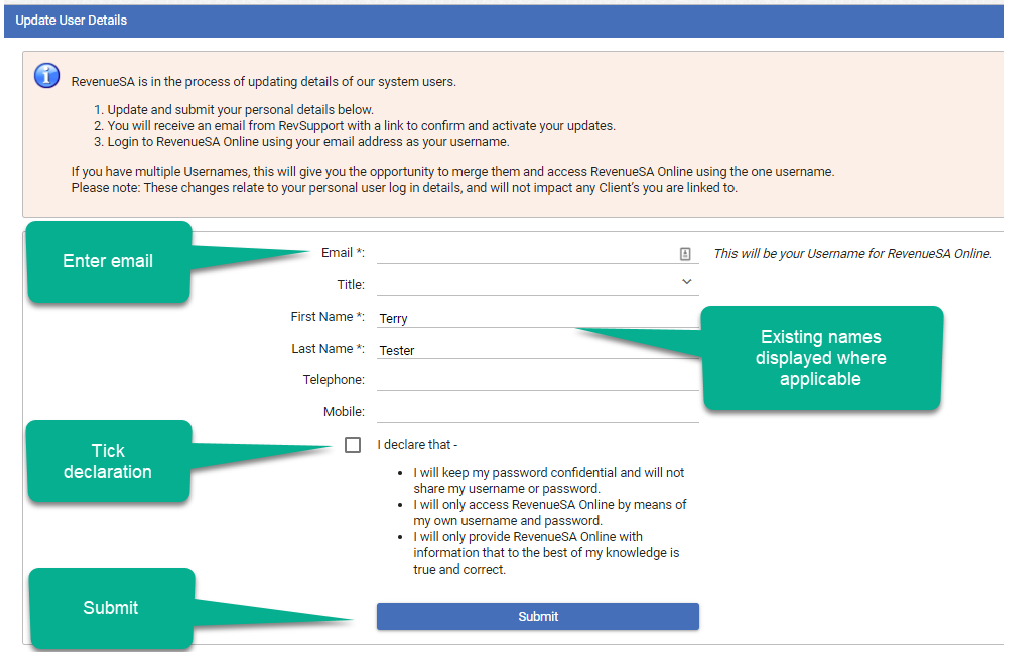

When accessing RevenueSA Online to complete the annual reconciliation, you may be asked to convert your username to an email address.

If a user does not have a username that is an email address, the following screen will appear when you have successfully logged in:

An email will be sent to the nominated email address. You will need to follow the instructions in the email to confirm the changes and then login to RevenueSA Online using your new username.

If your organisation ceased employing in South Australia during 2019-20 and will not be continuing to trade or pay wages in South Australia in 2020-21 onwards, you will be required to submit the final return in the annual reconciliation.

When prompted select YES to the question ‘Did you cease paying wages in South Australia during 2019-20?’

You will be asked if you want to cancel registration for your organisation and you will be required to enter a date of cancellation (the date your organisation ceased to trade or pay wages in South Australia) and a reason for the cancellation (from a drop down list).

The maximum payroll tax deduction entitlement is $600,000. However this may vary based on group status and Australia wide wages.

RevenueSA Online will calculate the applicable payroll tax deduction.

Employers sometimes make lump sum payments. This can include superannuation top ups, fringe benefits and bonuses.

As a result of COVID-19 payroll tax relief being provided to eligible employers, if these payments relate to the full financial year you will need to split them across the 2 periods.

For example, an employer pays an employee a $5,000 bonus in recognition of their work through the financial year. The payment is made in June. The payment relates to the whole financial year, therefore the payment would be declared as follows:

Period 1: 1 July 2019 to 29 February 2020

$5,000 x 244 (number of days from 1 July to 29 Feb) / 366 (number of days in the year) = $3,333

Period 2: 1 March 2020 to 30 June 2020

$5,000 x 122 (number of days from 1 March to 30 June) / 366 (number of days in the year) = $1,667

Total declared = $3,333 (Period 1) + $1,667 (Period 2) = $5,000

If you estimate that your organisation's Australia wide wages for 2020-21 will be $1.5 million or less you will be prompted towards the end of the annual reconciliation (at the wage estimates screen) to cancel the registration. You have the option to cancel the registration or remain registered:

- To cancel select cancel registration.

- To remain registered select continue with registration.

It’s your choice whether to remain registered or cancel. If your organisation's wages are close to the threshold (currently $1.5 million), or they fluctuate year to year, you may prefer to retain the registration in case your organisation exceeds the threshold in 2020-21.

If you choose to remain registered and you would like to change the return cycle for your organisation to annual or monthly please email your request to payrolltax@sa.gov.au.

The July 2020 monthly return will be open on RevenueSA Online from 22 July 2020 and must be lodged by 14 August 2020. We recommend you complete the 2019-20 annual reconciliation before the July return to ensure the estimated rate and deduction entitlement is calculated for the 2020-21 monthly returns.

Reminder: Eligible employers who have applied for the COVID-19 payroll tax waiver/deferral must continue to lodge their monthly payroll tax returns to capture wages for the month, even if no payroll tax payment is required to be made.

Lodging annual reconciliations where the organisation is part of a group

It is important for the DGE to lodge the annual reconciliation first before other group members as this will determine what COVID-19 payroll tax relief the group members may be eligible for, a waiver or deferral.

Payment options for organisations that have deferred their payroll tax liability

Payment options may be available if your organisation is unable to meet their deferred payroll tax due to COVID-19. Further information will be available in due course. If you have concerns about paying your payroll tax liability, please contact RevenueSA at payrolltax@sa.gov.au, or on (08) 8226 3750 (select option 5) to discuss options available.

Contact Us

When contacting us please provide your South Australian Taxpayer Number (if known), ABN, and organisation name.

| payrolltax@sa.gov.au | |

| phone | (08) 8226 3750, select option 5 |

| fax | (08) 8226 3805 |

| post | GPO Box 2418, Adelaide, SA 5001 |

You can reach us during business hours: 8:30am - 5:00pm (South Australian time), Monday to Friday (excluding public holidays).

Do you want to provide feedback or lodge a complaint?

You can do so via our feedback and complaints page.