2015-16 State budget land tax amendments

Status: Current

Legislation: Land Tax Act 1936

Date Issued: 18 June 2015

Information Circulars do not have the force of law.

As part of the 2015-16 State Budget, the Government announced several proposed amendments to the Land Tax Act 1936 (the “Act”).

The legislative amendments to implement the land tax measures announced are contained in the Statutes Amendment and Repeal (Budget 2015) Bill 2015 (the “Bill”), which was introduced into Parliament today. The operation of these legislative measures are subject to the Bill coming into force as an Act.

With respect to each announced measure, the following guidance is provided for taxpayer information:

Insertion of an exemption for Special Disability Trusts

Trusts Land held in a Special Disability Trust set up under Section 1209L of the Social Securities Act 1991 (Cwlth) or Section 52ZZZW of the Veterans’ Entitlement Act 1986 (Cwlth) which constitutes the principal place of residence (PPR) of the primary beneficiary of that trust will be wholly exempt from land tax (on application) as and from midnight, 30 June 2015.

For further information on this exemption, please refer to Information Circular 79.

Amendments to the operation of section 5A of the Act

As part of the 2001-02 State Budget, Section 5A was inserted into the Act to deliver land tax relief where taxpayers move home or construct a new home which gives rise to a land tax liability on an intended PPR.

Relief is currently provided under Section 5A of the Act where no rental income is received from either property during the period that the homes are owned concurrently and the former residence is sold prior to the end of the financial year in which the exemption for the new residence is sought.

As a result of an anomaly in the operation of the provisions, the waiver/refund is not currently available where a person moves into a new property just prior to 30 June but has not yet sold their old property which was their previous PPR. If the property owner moved into the new property after 30 June, they would qualify for the refund so long as they sold their old home before 30 June of the following year. The issue is one of timing.

The proposed amendment in the Bill is required to accommodate cases where taxpayers are in the process of selling a home and as a result own two properties at 30 June. In these circumstances, the new property is the taxpayer’s current PPR (and eligible for exemption) and the other property is the prior PPR (liable to land tax). The amendment ensures the waiver/refund is applied equitably.

It should be noted that the existing criteria that the old home be sold prior to the commencement of the following financial year and no rental income be received for either property whilst owned concurrently will be maintained.

Additionally, Section 5A(4)(c) of the Act currently requires that a taxpayer lodge a waiver/refund request with RevenueSA by 30 September following the end of the financial year in respect of which the waiver/ refund is sought. The Commissioner of State Taxation (the “Commissioner”) has no discretion to allow the late lodgement of a waiver/refund request under Section 5A of the Act once the deadline has passed.

The deadline contained in Section 5A(4)(c) of the Act can be onerous given some taxpayers are unaware of their entitlement for a waiver/refund. The Bill therefore contains an amendment to extend that deadline to five years from the issue of the assessment to which the application relates.

The proposed amendments to Section 5A of the Act will come into operation at midnight, 30 June 2015, but will apply to applications made in respect of the 2014-15 financial year and subsequent years.

Amendments to the operation of section 13A of the Act (Trust Structures)

The use of trust structures by taxpayers to benefit from the exception to the aggregation principle contained in Section 13(3)(b) of the Act in circumstances where it was not intended for this beneficial trust provision to apply has recently become more prevalent. These practices involve exploiting the deficiencies in Section 13A of the Act when read in conjunction with Section 13(3)(b) of the Act. As Section 13A of the Act was introduced as a specific antiavoidance measure, the exploitation of the same required rectification.

Effective for the 2015-16 financial year, the Bill will provide the Commissioner with the power to disregard minor interests which are created by trust relationships. Specifically, the Commissioner may disregard:

- A minor interest in land held by a trustee of a trust irrespective of whether the trustee holds a more significant legal interest in the same land in another capacity; and

- Minor interests in land held by beneficiaries or potential beneficiaries, such interests being deemed to be an actual interest in the land for the purposes of the Act.

In short, the amendments allow the Commissioner to disregard interests that are minor due to the capacity (legal or beneficial) in which the relevant entity/person holds the interest. The existing threshold tests for interests of 5% or less and for interests of more than 5% but less than 50% apply equally to trust held interests.

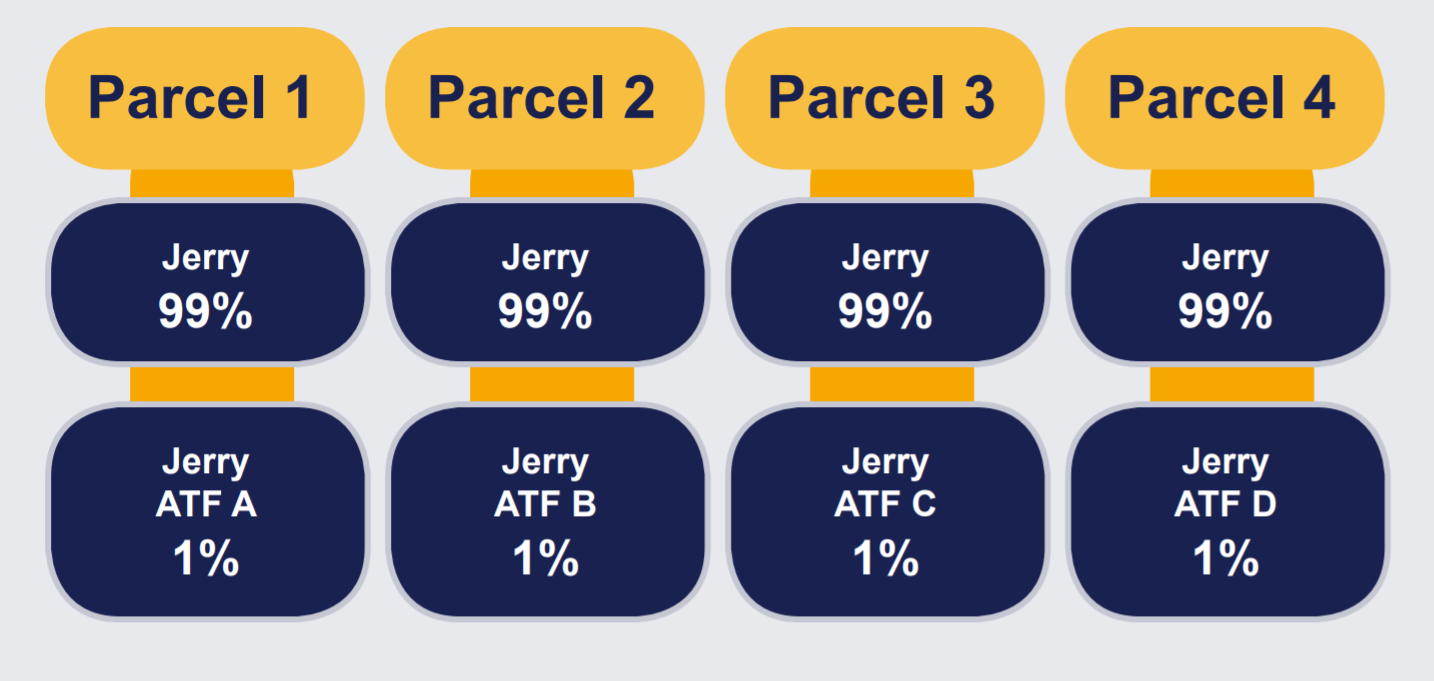

The following example illustrates how the intended provisions can operate:

Example

As can be seen, Jerry is the 100% legal owner of all four parcels. However, by executing four (slightly varied) declarations of trust, Jerry could declare a 1% interest in each and every parcel and hold those interests on trusts for varying beneficiaries (classed ‘A’ through to ‘D’). The trusts created are over minor interests in land.

Applying the proposed amendments, section 13A(2) of the Act would automatically apply to disregard the 1% beneficial interests of classes A through to D. Arguably, after this step, Jerry would hold each Parcel 100% in his individual capacity for the purposes of the Act such that all four parcels would be subject to aggregation. However, the automatic application of section 13A(2) of the Act to interests of 5% or less would also see Jerry’s 1% legal interests in the Parcels disregarded, leaving Jerry in his individual capacity as the undisputed sole owner under the Act.

These amendments to Section 13A of the Act will apply to minor interests irrespective of when they were created, but only affect assessments for the 2015-16 and subsequent financial years.

Amendments to the retrospective operation of section 13A of the Act

Due to 2 recent decisions of the Supreme Court, some taxpayers have questioned whether an opinion formed by the Commissioner under Section 13A(3) of the Act to disregard a minor interest can operate with respect to prior financial years.

The Bill puts it beyond doubt that Section 13A of the Act has retrospective effect such that the Commissioner’s opinion formed under Section 13A(3) applies to all financial years from the time the interest in land the subject of the opinion was created (see proposed Section 13A(3a) in the Bill). Proposed Section 13A(3a) also ensures that the retrospective effect of Section 13A(5) is not impeded by the prior exempt status of the land in question.

As Section 13A of the Act was originally introduced with effect as and from 30 June 2008 for the 2008-09 financial year, the amendment cannot operate to affect an assessment of land tax for a financial year preceding 2008-09.

This was always the intent upon the introduction of Section 13A as land tax assessments are issued in September and October and the Commissioner practically must make his decision after 30 June. The amendments are clarifying the position as it was always intended to operate.

Amendments to the operation of section 19 of the Act

Current legislation prevents the imposition of penalty tax and interest under the Taxation Administration Act 1996 (the “TAA”) in circumstances where a taxpayer is liable to land tax but has not been served with a notice of assessment pursuant to Section 19 of the Act. The anomaly exists from inconsistencies between the notion of the liability for land tax arising at the commencement of a financial year (Section 4(2) of the Act) and the liability to pay arising 30 days after service of a notice of assessment (Section 19 of the Act).

A taxpayer is only liable to penalty tax and interest where a tax default has occurred, but the notion of a tax default under Section 3 of the TAA focuses on a failure to pay in accordance with the tax law in question. It is arguable that a taxpayer who has not been issued a notice of assessment has thus not failed to pay in accordance with the Act, even though a tax liability arises prior to the service of such a notice. Therefore, whilst a person who has provided false or misleading information, or failed to provide information that should have been provided, may be liable to prosecution, such a person may potentially avoid liability to penalty tax and interest in some cases as a result of them providing false or misleading information, or failing to provide information that should have been provided. This anomaly will occur mostly in situations where a taxpayer has obtained an exemption by providing false or misleading information, or where the taxpayer’s circumstances have changed and they have failed to notify the Commissioner.

View this Information Circular as a PDF (PDF 274KB)