Nexus provisions

Status: Replaced on 12 May 2011 by Revenue Ruling PTA039 - view current version

Legislation: Payroll Tax Act 2009

Date Issued: 28 June 2010

Information Circulars do not have the force of law.

Background

The payroll tax nexus provisions determine in which Australian state or territory (jurisdiction) payroll tax is to be paid in respect of payments made to workers operating in more than one jurisdiction in a month.

In June 2009, all jurisdictions agreed to introduce amendments to the payroll tax nexus provisions, which would apply retrospectively from 1 July 2009. All jurisdictions have passed the legislation to implement the new rules.

These changes only affect wages for workers providing their services in more than one jurisdiction in a month or partly in more than one jurisdiction and partly overseas in a month. Where a worker provides their services wholly in one jurisdiction, as is the case for the majority of workers, payroll tax will continue to be paid to the jurisdiction where those services are performed.

This Information Circular explains the new nexus rules and also clarifies the circumstances when wages must be declared in South Australia for payroll tax purposes including wages paid for services performed in another country (or countries).

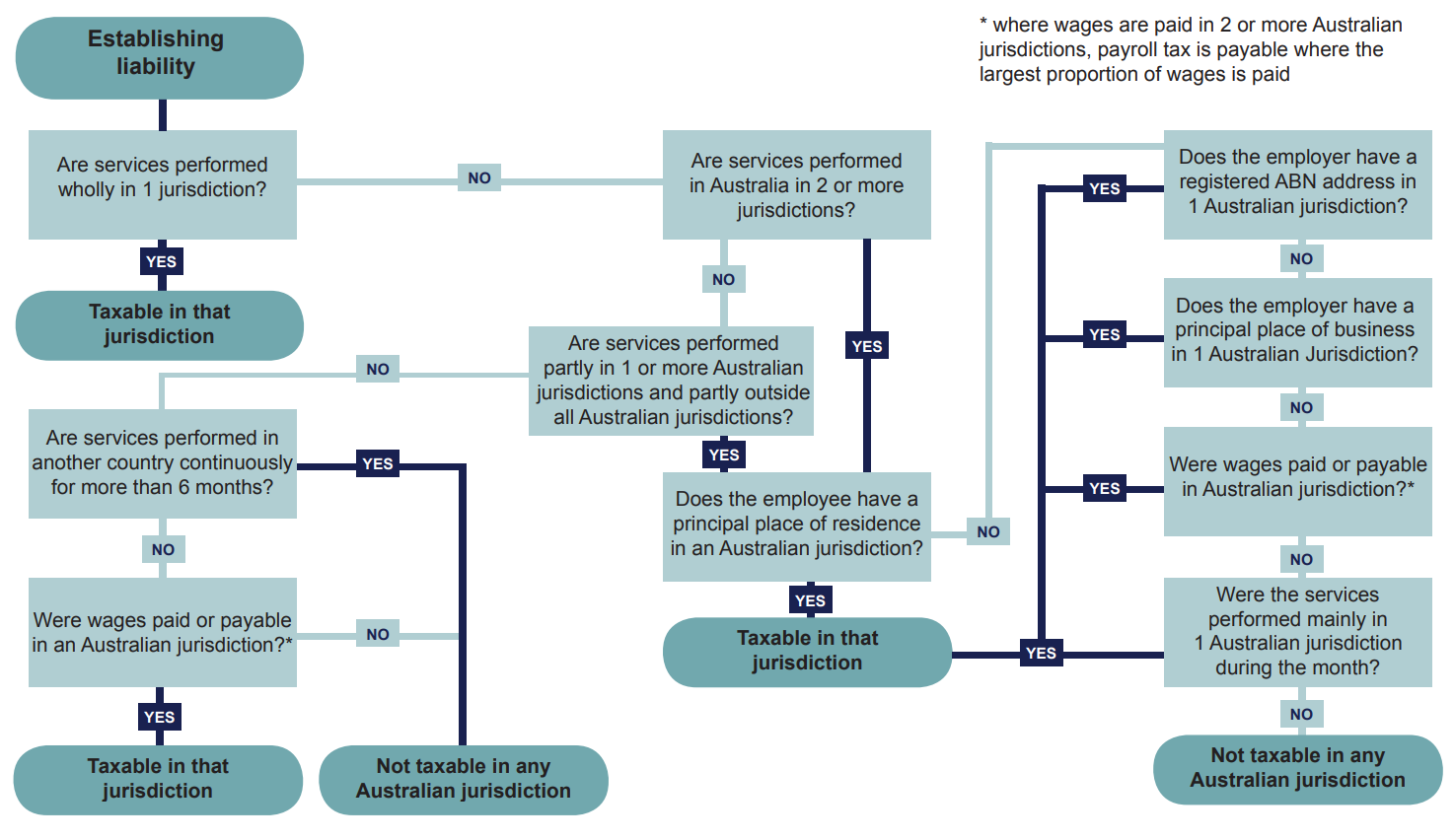

This Information Circular must be read in conjunction with the attached Flowchart which explains how the various scenarios will be treated and shows the circumstances in which wages are taxable in South Australia.

For the purpose of this Information Circular, overseas means outside all Australian jurisdictions.

It is important to note, that the liability for South Australian payroll tax must be considered separately for each calendar month.

Introduction

Payroll tax is payable when an employer’s total Australian wages exceed the payroll tax-free threshold (deduction amount). Australian wages comprise South Australian wages and wages paid in all other jurisdictions. South Australian wages are the wages subject to payroll tax under the Payroll Tax Act 2009 (the “Act”). Interstate wages are those wages subject to payroll tax in the other jurisdictions under their equivalent payroll tax legislation.

To determine whether the wages paid or payable in respect of each monthly return period are subject to payroll tax in South Australia, section 11 of the Act requires an employer to determine the place where the employee has wholly performed services in a calendar month. Where an employee has not wholly performed services in South Australia, the following factors also need to be considered:

- the place where the services are performed;

- the employee’s principal place of residence;

- the employer’s registered ABN address/principal place of business; or

- the place where the wages are paid to the employee

Determining where wages are taxable - section 11

Sections 11, 11A, 11B and 11C of the Act assist employers in determining where wages are liable to payroll tax.

Where services are performed wholly in one jurisdiction

If services are performed wholly in one jurisdiction in the relevant month, payroll tax is payable in that jurisdiction.

This looks at the place where services are performed by the employee in the month that the wages are paid or payable even if that place is not where the employee usually performs services. For example, wages paid to an employee in June 2010, who ordinarily performs services in South Australia, but in June 2010 performed services wholly in Victoria to complete a temporary project would be taxable in Victoria.

Where services are performed in more than one Australian jurisdiction and/or partly overseas

If services are performed in a calendar month in more than one jurisdiction and not overseas or in one or more jurisdictions and overseas, the new provisions provide a tiered test for determining payroll tax liability.

Test 1

Employee's principal place of residence

Section 11A

Payroll tax is payable in the jurisdiction in which the employee’s principal place of residence (PPR) is located.

If an employee has more than one PPR in the relevant month, the employee’s PPR on the last day of that particular month is the one taken to be the PPR.

In the case of a corporate employee that is deemed to be an employee under the Act (for example, an incorporated worker that is deemed to be an employee under the contractor provisions or under the employment agency provisions) the PPR of the corporate employee is the ABN address or where there is no ABN the principal place of business of the deemed corporate employee.

Test 2

Employer's ABN address or principal place of business

Section 11B

If an employee does not have a PPR in an Australian jurisdiction during the relevant month, payroll tax is payable in the jurisdiction where the employer has their registered ABN address.

If the employer does not have a registered ABN address, or has two or more ABN addresses in different jurisdictions, payroll tax is payable in the jurisdiction where the employer has their principal place of business (PPB).

If the employer has more than one PPB in a relevant month (for example, when an employer changes their PPB address part way through a relevant month) the PPB is the address on the last day of that particular month.

Test 3

Where wages are paid or payable

Section 11(1)(b)(iii) and Section 11(C)(5)

If the employee does not have a PPR in an Australian jurisdiction and the employer does not have an ABN address or a PPB in an Australian jurisdiction, payroll tax is payable in the jurisdiction where the wages are paid or payable.

If wages are paid or payable in a number of jurisdictions, payroll tax is paid in the jurisdiction where the largest proportion of wages is paid.

| Example | Mrs Smith provides services to her employer ABC Pty Ltd in October in more than one jurisdiction. Mrs Smith is remunerated for her services in October. Mrs Smith does not have a PPR in an Australian jurisdiction and ABC Pty Ltd does not have an ABN address or its PPB in an Australian jurisdiction. She receives $200 in New South Wales, $300 in Victoria and $1000 in South Australia. The payments are aggregated and tax is payable on the total amount of $1,500 in South Australia because that is where the largest proportion of wages was paid. |

Test 4

Services performed mainly in South Australia

Section 11(b)(iv)

If both the employee and the employer are not based in an Australian jurisdiction and wages are not paid in Australia, payroll tax is paid in South Australia if the services were mainly (that is, actual time worked is more than 50%) performed in South Australia during the month.

| Example | An overseas holding company sends its employee John Doe to work at its South Australian subsidiary for 16 days of a month. The worker stays in a hotel during this time and John’s wages continue to be paid into his bank account in London. As John remains the employee of the overseas holding company but mainly performed services in South Australia for the month, all his wages for that month are liable to payroll tax in South Australia. |

Overseas employment

Employees working in another country - assignment for less than 6 months

Wages paid or payable in South Australia to an expatriate employee who is working in another country, or countries, are taxable where the assignment in another country, or countries, is no more than six continuous months. If only part of the wages earned by an expatriate employee working in another country or countries is paid in South Australia, such wages must be declared for payroll tax. If the wages earned by the expatriate employee are paid in more than one Australian jurisdiction, payroll tax is payable on the full amount of wages paid in the Australian jurisdictions, in the jurisdiction where the largest proportion of wages is paid.

Employees working in another country – assignment more than 6 months

Wages are exempt if the employee has worked in another country for a continuous period of more than 6 months (that is, the exemption from payroll tax applies for the whole assignment, including the first 6 months). The 6 month period does not have to be within the one financial year but must be a continuous period. Where an employee, working in another country, returns to Australia in the following circumstances, it will not be considered to be a break in continuity:

- for a holiday; or

- to perform work exclusively related to the overseas assignment for a period of less than one month; and in either case

- the employee immediately returns to that country to perform further work on the assignment.

If an employee returns to Australia in any other circumstances, the 6 month period will recommence from the date that the employee recommences work in the overseas country.

Services performed offshore

Any wages that relate to services performed offshore and beyond the limits of any Australian jurisdiction, but not in another country, are taxable if they are paid or payable in South Australia irrespective of the duration of the assignment. As such the exemption that applies to wages paid or payable in South Australia in relation to work performed in another country is not applicable.

Where an employee is working outside any jurisdiction, but not in another country, the wages are taxable in the jurisdiction in which wages are paid. Employees working on an oil rig would not be considered as working in another country unless the oil rig is physically located in another country.

Wages paid in a foreign currency

When calculating the value of the payment, RevenueSA will accept an exchange rate conversion, based upon the Reserve Bank of Australia’s daily rate published, for the day of payment. If this creates difficulties, the employer may use, as an alternative, the yearly average rate for the financial year, as published by the Australian Taxation Office. The previous year’s figure may be applied for the purpose of making monthly returns, provided that the current year’s rate is used to make an appropriate adjustment in the Annual Reconciliation return.

Further deeming provisions under section 11

Section 11 also details a number of other factors that employers may need to take into account (in conjunction with the tests previously outlined) above in determining when and where their payroll tax liability arises.

Tax is payable in the month in which wages were paid - section 11(3)

Where wages relate to services performed by an employee over several months (for example, an annual bonus), payroll tax is payable in the jurisdiction where the services were performed in the month the wages are paid or payable.

Example

In June 2010 Joe is paid $3,000 wages for services performed in that month and also a $2,000 bonus for services performed during the financial year ending June 2010. Even though the bonus payment relates to services performed for the whole financial year only the services performed in June 2010 will be used in determining whether services were provided wholly in a jurisdiction or in more than one jurisdiction.

If Joe performed services wholly in South Australia in June 2010 then payroll tax on the $5,000 wages will be payable in South Australia. If Joe provided services in more than one jurisdiction in June 2010, payroll tax would be payable in the jurisdiction where Joe had his PPR in June 2010.

If wages are paid in a different month from when they were payable - section 11(7)

If wages are paid in a different month from the month they are payable, liability arises in the earlier of the two months. For example, wages are paid in August 2010, but under the contract with the employee those wages should have been paid in May 2010 in South Australia. As May is the earlier month, the payments are taxable for May in South Australia based on where the services were performed.

If there are 2 or more payments in one month

There may be instances where an employee receives two payments of wages from the same employer in one month. The payments may relate to services being provided wholly in one jurisdiction or in two or more jurisdictions.

Example

Mrs Smith receives wages of $1,000 on 14 November for services performed in South Australia. She receives another $2,000 on 28 November from the same employer for services performed in New South Wales. The two amounts are to be aggregated together and treated as if paid for all services performed by the employee in that month (that is, in South Australia and New South Wales). Therefore, payroll tax is payable in the jurisdiction where Mrs Smith has her PPR.

Where services are not performed in any jurisdiction in the month in which wages are paid - Section 11(5)

There may be instances where services are not performed in a particular month in which the wages are paid. In such circumstances, the liability for payroll tax is determined by ascertaining where services were provided for that employer during the most recent month.

Example

Mrs Smith is paid in the month of December but has not provided services to the employer in that month. The last month Mrs Smith provided services to that employer was October and those services were provided wholly in South Australia. As such, payroll tax is payable in South Australia for the wages paid to Mrs Smith in December. However, if Mrs Smith provided services in more than one jurisdiction in the month of October then the payroll tax liability for the wages paid in December will be determined by her PPR.

If no services were provided to the employer, payroll tax would be payable in the jurisdiction where it could reasonably be expected that the employee would provide services.

Example

If Mrs Smith accepts an offer of employment in August to commence work in South Australia in November and receives a payment of wages in August, services are deemed to have been performed in South Australia in August.

For further guidance, please refer to the flowchart

Flowchart for determining payroll tax liability

Shares and options

Payroll tax liability for the grant of a share or option are also governed by the new nexus rules contained in Section 11 of the Act and explained in this Information Circular.

However, certain circumstances relating to shares and options attract different nexus rules. These are outlined below (please note the flowchart does not apply in the circumstances below).

Section 26 of the Act identifies the place where wages are payable when a share or option is granted. Section 26 applies in the following situations:

- the employee performs services in more than one Australian jurisdiction and/or partly overseas, and:

- the employee does not have a PPR in an Australian jurisdiction; and

- the employer does not have an ABN address or a PPB in an Australian jurisdiction; or

- the employee performs services wholly outside all Australian jurisdictions for less than 6 months but is paid in an Australian jurisdiction.

In these situations where the grant of a share or an option constitutes wages, the shares or options are taken to be paid or payable in the jurisdiction where the share is a share in a local company.

View this Information Circular as a PDF (PDF 263KB)